GI Bill Housing Allowance: How the MHA Is Calculated

How the Post-9/11 GI Bill housing allowance (MHA) is calculated for 2026 - the E-5-with-dependents BAH base, eligibility tier, rate of pursuit, and the online and active-duty rules that cut it in half.

The GI Bill housing allowance is the part of your Post-9/11 GI Bill that pays your rent, and it is also the part that surprises people most. Two veterans sitting in the same lecture hall can receive monthly checks that differ by more than a thousand dollars, and neither one did anything wrong. The amount is not a flat benefit. It is built from your school's location, how much of your benefit you earned through active service, how many credits you are taking, and whether any of your classes meet in person. Get one of those wrong and the number you budgeted around can be off by half.

This guide explains exactly how the Monthly Housing Allowance, the MHA, is calculated, in plain English, with the fixed rates for the current award year that runs August 1, 2025 through July 31, 2026. We will walk through every input the VA uses, the rules that quietly cut the payment in half, and the timing gotchas that leave students short during breaks. The dollar amounts shift with your school's ZIP code and your exact enrollment, so rather than guess, run your own situation through the GI Bill calculator as you read. It models the housing allowance, tuition, and books stipend together using your inputs.

What the GI Bill Housing Allowance Actually Is

The MHA is the housing portion of the Post-9/11 GI Bill, formally Chapter 33. The benefit has three separate pieces, and the housing allowance is only one of them:

- Tuition and fees paid directly to your school, up to the public in-state cap for public schools or an annual national cap for private and foreign schools.

- A monthly housing allowance (MHA) paid to you, the student, to cover living costs while you are enrolled.

- An annual books and supplies stipend, paid at the start of each term.

The housing allowance is the piece you actually live on, and it is the one with the most moving parts. It is paid to you monthly, in arrears, meaning you are paid for a month after you have completed it. It is not taxable income, so you will not get a 1099 for it and you do not report it on your return. And critically, it is tied to the school, not to where you live. A student attending a campus in an expensive metro area receives a higher allowance than one attending in a low-cost town, even if both students rent identical apartments in the same neighborhood.

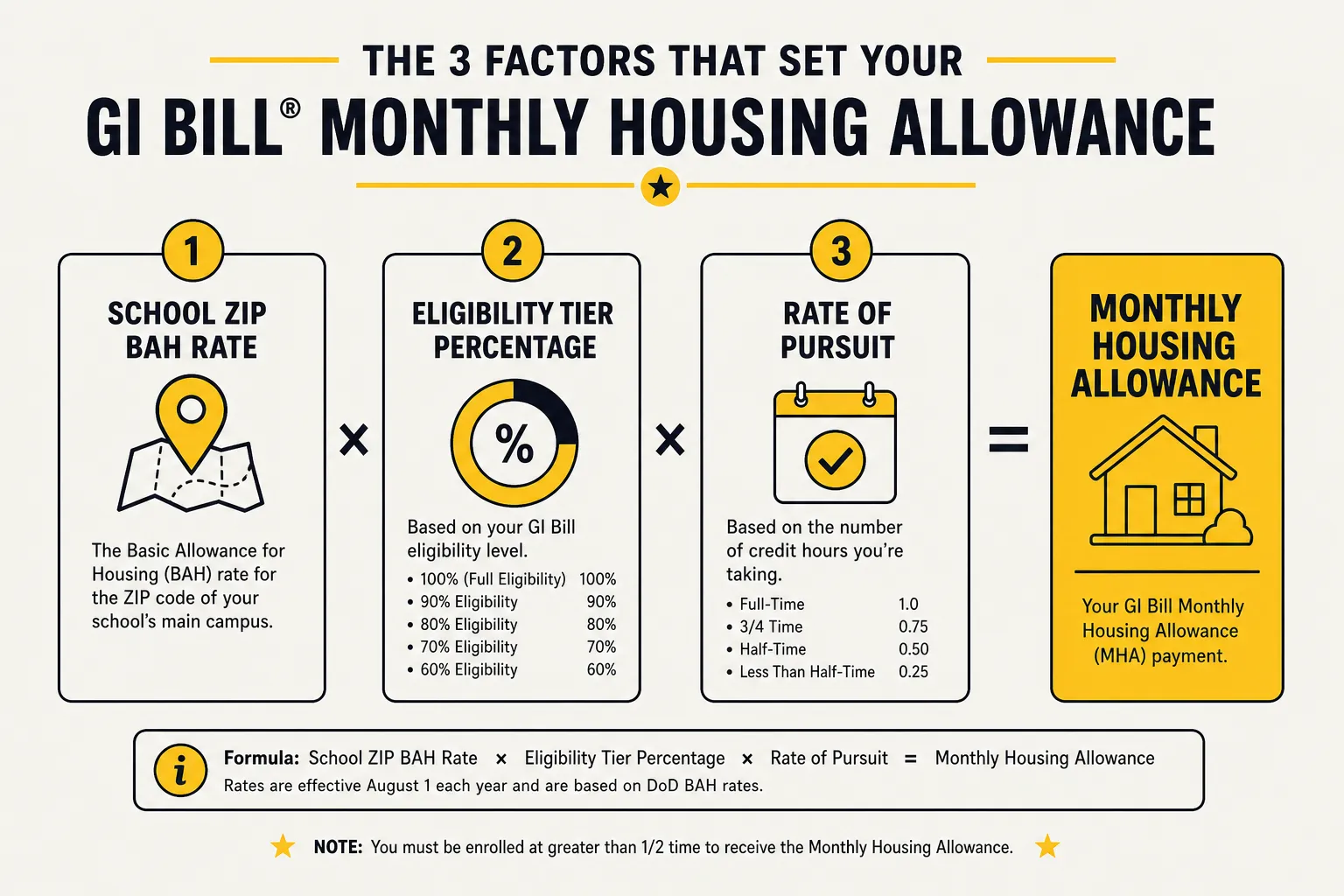

The Three Factors That Set Your MHA

Every MHA calculation comes down to three multiplied factors: the base rate, your eligibility tier, and your rate of pursuit. Understand these three and you can predict your check within a few dollars.

Factor 1: The base rate is an E-5-with-dependents BAH

The starting point for the MHA is the military Basic Allowance for Housing, specifically the BAH rate for an E-5 with dependents at your school's ZIP code. This is the single most misunderstood part of the benefit. Your own rank does not matter. Whether you actually have dependents does not matter. The VA uses the E-5-with-dependents rate for everyone as a standard yardstick, then localizes it to wherever your school sits.

That is why location drives the number so hard. The E-5-with-dependents BAH in a high-cost coastal city can run more than double the rate in a rural college town. Two students with identical service records and identical course loads will receive very different checks purely because of where their campuses are. If you are weighing schools, this is a real and often overlooked financial variable. You can look up the underlying military rate for any ZIP in the BAH calculator to see how much your school's location is worth before the GI Bill adjustments are applied.

One nuance: the relevant ZIP is the campus where you physically attend the majority of your classes, not the school's headquarters or billing address. For a large university system with multiple campuses, that distinction can move your allowance.

Factor 2: Your eligibility tier scales the whole benefit

You do not automatically receive 100 percent of the Post-9/11 GI Bill. Your percentage is set by how long you served on qualifying active duty after September 10, 2001, and that same percentage scales your housing allowance, your tuition coverage, and your books stipend all together. The 2026 tiers are:

| Qualifying active-duty service | Benefit percentage |

|---|---|

| At least 36 months (1,095+ days) | 100% |

| 30 to 35 months (910 to 1,094 days) | 90% |

| 24 to 29 months (730 to 909 days) | 80% |

| 18 to 23 months (545 to 729 days) | 70% |

| 6 to 17 months (180 to 544 days) | 60% |

| 90 days to 5 months (90 to 179 days) | 50% |

You also reach the full 100 percent tier, regardless of time served, if you received a Purple Heart on or after September 11, 2001, or if you were discharged for a service-connected disability after at least 30 continuous days of active duty.

A practical example: if your school's E-5-with-dependents BAH rate is the base, and you are at the 80 percent tier, your full-time MHA before any other adjustment is 80 percent of that base. The tier is a straight multiplier on everything. If you are not certain which tier you fall into, your Certificate of Eligibility from the VA states your percentage near the top, and you can model different tiers in the GI Bill calculator to see the dollar impact.

Factor 3: Rate of pursuit scales it again

The third factor is how much school you are actually taking, called your rate of pursuit. You must be enrolled at more than 50 percent of full-time to receive any housing allowance at all. A student at exactly half-time or below gets zero MHA, even though tuition is still covered.

Above that threshold, your rate of pursuit is rounded and applied as a percentage. If full-time is 12 credits and you take 9, your rate of pursuit is 75 percent, and your housing allowance is paid at 75 percent of the tier-adjusted rate. The VA rounds the rate of pursuit to the nearest 10 percent for the payment, so the practical buckets are 60, 70, 80, 90, or 100 percent for anything above the half-time line.

So the full stack looks like this for an in-person student:

School-ZIP E-5-with-dependents BAH x your tier percentage x your rate of pursuit = your monthly housing allowance

That is the entire formula for a traditional on-campus student. The complications that follow are special rules that override or replace one of these three pieces.

The Two Rules That Cut Your MHA in Half

Two situations replace the local BAH base with a much lower national figure. Both routinely catch students off guard because the rest of the formula looks identical, but the starting number is slashed.

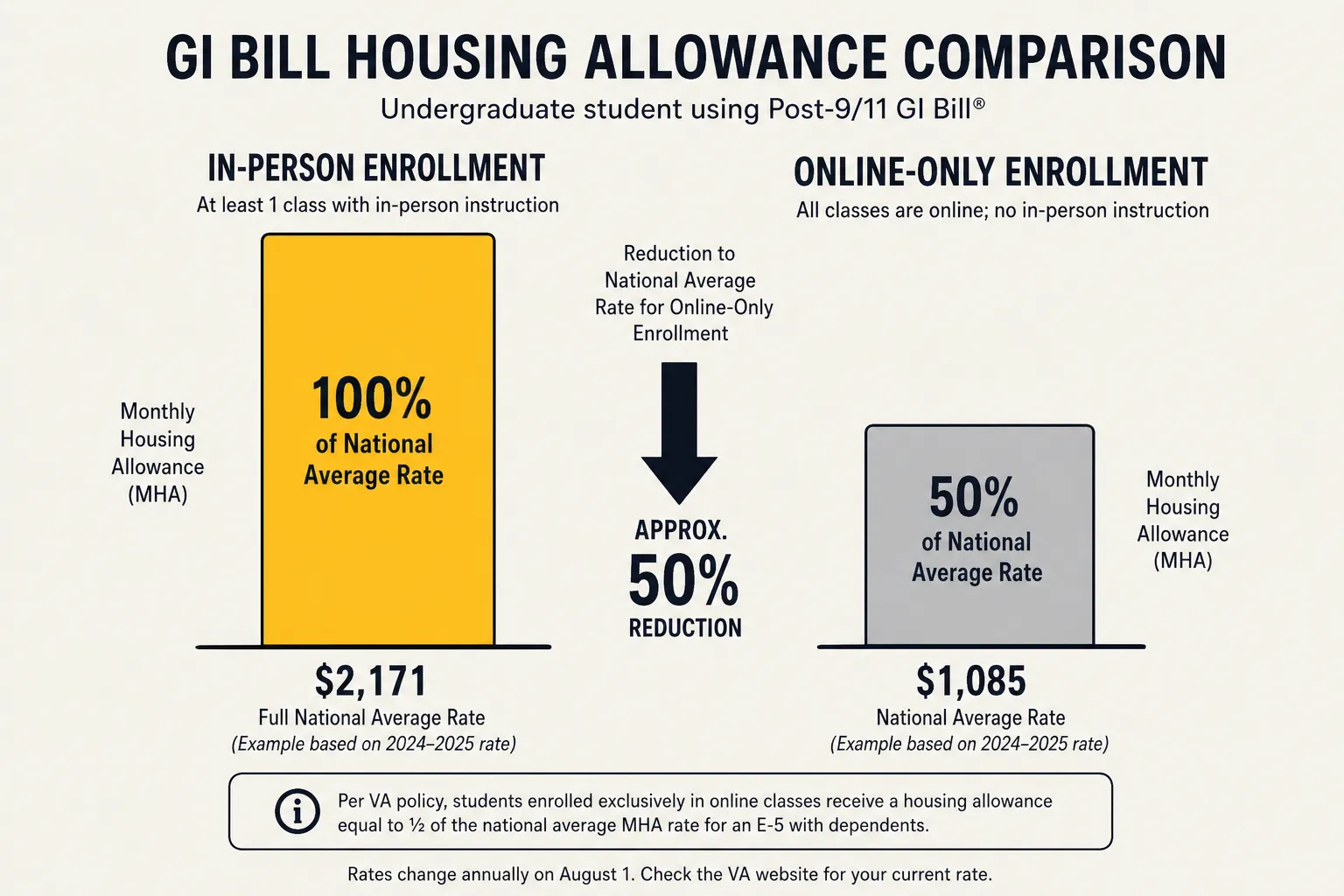

Online-only enrollment

If every one of your courses is taken online, you do not receive the local BAH rate for your school's ZIP. Instead you receive a flat national rate set at one-half of the national average E-5-with-dependents BAH. For the current award year, running August 1, 2025 through July 31, 2026, that online MHA is up to $1,169 per month at the 100 percent tier and full-time pursuit, and it does not vary by location at all. An online student in Manhattan and one in rural Kansas receive the same figure. Effective August 1, 2026, the VA has set the online rate higher, to up to $1,261 per month, so check which award year your term falls in.

This is roughly half of what an in-person student at a typical campus receives, and for students at high-cost campuses it can be a third or less. The fix is straightforward and worth knowing: taking even one class that meets in person, on a real campus, qualifies you for the full local resident MHA instead of the online rate. A single in-person credit can be worth several hundred dollars a month. If you are enrolling in a mostly online program, look hard at whether one on-campus course is available, because the housing math can swamp the inconvenience.

Active-duty students

If you are still on active duty while using the Post-9/11 GI Bill, you do not receive the MHA at the local rate either. Active-duty members, and spouses using transferred benefits while the sponsor is still on active duty, receive no separate housing allowance because the service member is already drawing BAH or living in government quarters. The reasoning is that the government will not pay you twice for the same housing.

This matters most for transfer-of-benefit planning. A spouse who starts school while the sponsor is still serving will not get the housing check, but the same spouse using the benefit after the sponsor separates would. The tuition and books portions are still paid in both cases; it is only the housing piece that is suppressed while on active duty.

Foreign Schools and the National-Average Rate

Students attending a school located outside the United States are another special case. There is no local BAH table for a campus in London or Tokyo, so the VA pays a fixed national-average rate instead. For the current award year, August 1, 2025 through July 31, 2026, the foreign-school MHA is up to $2,338 per month at the 100 percent tier and full-time pursuit. As with every other figure, your tier percentage and rate of pursuit then scale it down from there. Effective August 1, 2026, the foreign rate rises to up to $2,522 per month, so confirm the rate for the period your term falls in.

That foreign rate is, not by accident, exactly double the online rate. The online figure is half the national average and the foreign figure is the full national average for an E-5 with dependents. Knowing that relationship is a useful sanity check when you are estimating any of these numbers.

How Training-Time Progression Affects Some Programs

For traditional college degree programs, your MHA holds steady as long as your enrollment holds steady. But for some structured programs, the housing allowance steps down over time on a fixed schedule. This applies to on-the-job training and apprenticeship programs, where the payment is designed to taper as your own wages from the employer rise. The schedule pays a percentage of the applicable MHA:

| Months in the program | Percentage of MHA paid |

|---|---|

| Months 1 to 6 | 100% |

| Months 7 to 12 | 80% |

| Months 13 to 18 | 60% |

| Months 19 to 24 | 40% |

| Beyond 24 months | 20% |

If you are in a standard classroom degree program, ignore this table; it does not apply to you. It is included because apprenticeship and OJT students are frequently confused when their check shrinks on schedule, assuming it is an error when it is the rule working as designed.

The Timing Traps Nobody Warns You About

The formula is only half the story. The other half is when the money actually arrives, and the gaps are where student budgets break.

You are paid in arrears

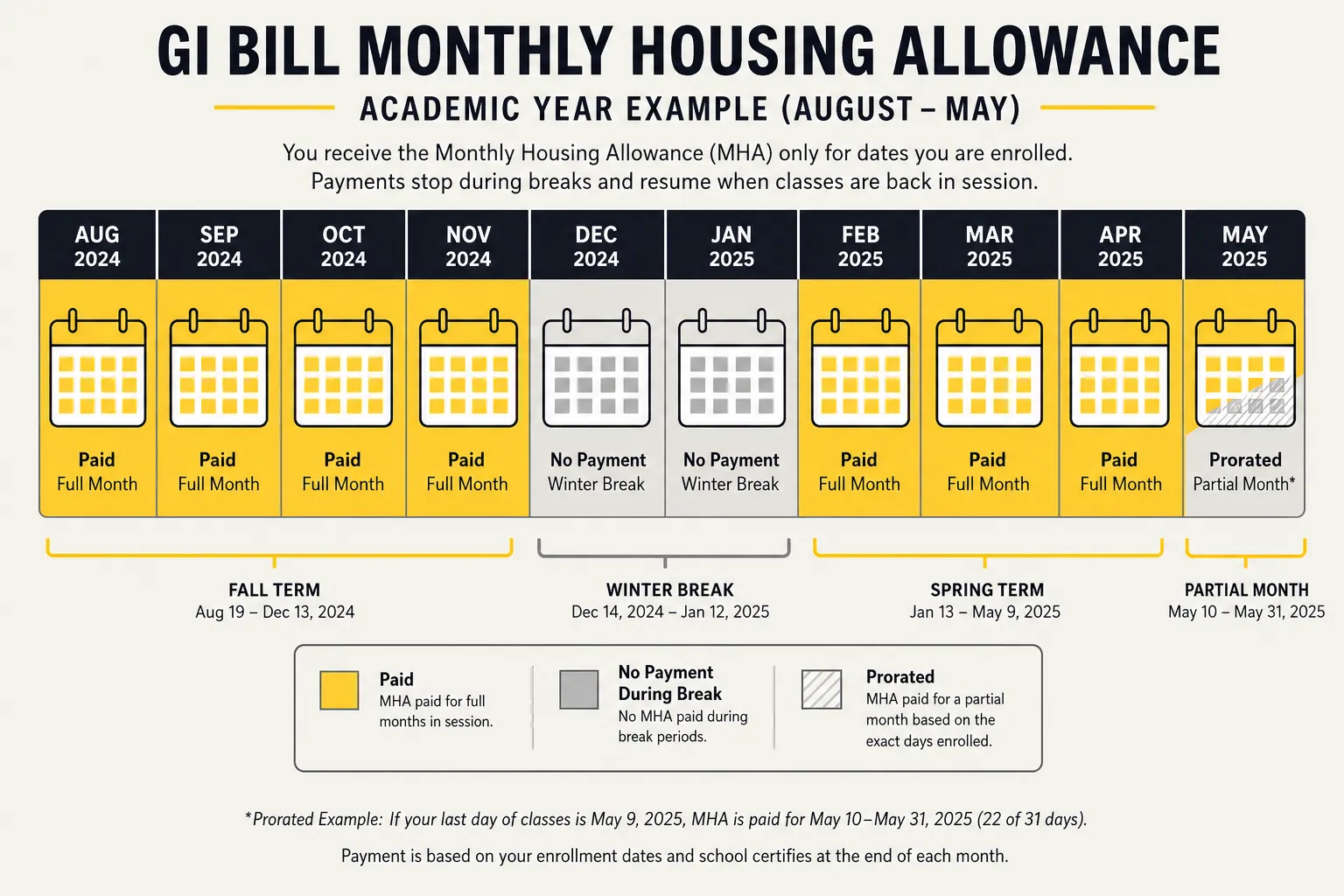

The MHA pays for a month after you finish it. Your August enrollment generates a payment that lands in early September. This means your first housing check of any term arrives roughly a month after classes start, and if you are counting on it to make a deposit or a first rent payment, you will come up short. Plan for a one-month float at the start of every program, not just your first.

Breaks between terms are unpaid

You are only paid for the days you are actively enrolled. During the break between the end of one term and the start of the next, the housing allowance stops. A long winter break or a summer with no enrollment means no housing check for those weeks, and the months on either side are prorated for the partial enrollment. Students who budget as if the MHA is a steady year-round salary get caught every December and every summer. Treat it as paid only while school is in session.

Partial months are prorated

Because the allowance is tied to days of enrollment, the first and last months of a term are almost never full payments. If your term starts on the 15th, that month's housing check covers only the second half of the month. The same applies to the month a term ends. This is normal and not an error, but it means your real monthly cash flow is lumpier than the headline full-time rate suggests.

Your entitlement is finite

The Post-9/11 GI Bill provides 36 months of full-time entitlement, and the months you draw the housing allowance burn that entitlement down. Every month of full-time MHA is a month of benefit used. Reducing your course load below full-time stretches your entitlement across more calendar time but pays a smaller monthly check while doing it. There is a real planning decision here between drawing a bigger check faster and stretching a smaller check longer, and it is worth modeling deliberately rather than defaulting into it.

Stacking the Yellow Ribbon Program on Top

The housing allowance is fixed by the rules above, but the tuition side of the benefit has a separate lever worth knowing because it affects whether a school is affordable at all. The Post-9/11 GI Bill caps tuition for private and foreign schools at a national annual maximum, and at public schools it covers the full in-state rate. When a school costs more than the cap, the Yellow Ribbon Program can close the gap: the school voluntarily waives a portion of the overage and the VA matches that waiver dollar for dollar.

Yellow Ribbon does not change your housing allowance. But it determines whether an expensive private or out-of-state school is reachable without out-of-pocket tuition, which in turn affects which campus ZIP sets your MHA. The two interact through your school choice even though they are separate benefits. Only students at the 100 percent eligibility tier qualify for Yellow Ribbon, which is one more reason your service-based tier percentage matters across the whole benefit.

Putting It All Together With a Calculator

The reason a calculator beats a rule of thumb here is that four independent variables multiply together, and getting any one wrong throws off the whole estimate. Here is the order of operations to estimate your own GI Bill housing allowance:

- Find your school's E-5-with-dependents BAH rate by its ZIP code. This is your base. For an online-only program, replace it with the national online rate instead. For a foreign school, use the national-average foreign rate.

- Multiply by your eligibility tier percentage from your Certificate of Eligibility.

- Multiply by your rate of pursuit, but only if you are above 50 percent of full-time. At or below half-time, your housing allowance is zero.

- Remember it pays in arrears, prorates partial months, and stops during breaks.

Because the localized BAH base changes constantly and varies by every ZIP, the cleanest way to get a real number is to enter your school and your tier into the GI Bill calculator, which pulls the current rates and applies the tier and pursuit adjustments for you. For a fuller picture of how the housing allowance fits alongside the tuition cap and books stipend, see the Post-9/11 GI Bill housing and tuition guide.

Common Mistakes to Avoid

- Assuming your own rank sets the rate. It does not. The base is always the E-5-with-dependents BAH, regardless of whether you served as an E-3 or an O-4.

- Going fully online without checking the math. Online-only enrollment pays the national online rate, not your local rate, often roughly half. One in-person class can restore the full local MHA.

- Budgeting through the breaks. The housing allowance stops between terms and prorates partial months. It is not a year-round salary.

- Forgetting the arrears lag. Your first check of a term lands about a month after classes begin. Plan for the float.

- Dropping below 51 percent of full-time. Anything at or under half-time pays no housing allowance at all, even though your tuition is still covered.

Frequently Asked Questions

How is the GI Bill housing allowance calculated?

It is the E-5-with-dependents Basic Allowance for Housing rate for your school's ZIP code, multiplied by your eligibility tier percentage, multiplied by your rate of pursuit. You must be enrolled at more than 50 percent of full-time to receive any housing allowance, and online-only or active-duty students receive a reduced or zero rate. Plug your school and tier into the GI Bill calculator for your own figure.

How much is the GI Bill housing allowance per month in 2026?

There is no single number because it is tied to your school's location. The local rate equals the E-5-with-dependents BAH at the campus ZIP, scaled by your tier and course load. The fixed exceptions for the award year running August 1, 2025 through July 31, 2026 are the online-only rate of up to $1,169 per month and the foreign-school rate of up to $2,338 per month, both at the 100 percent tier and full-time enrollment. Effective August 1, 2026, those rates rise to up to $1,261 for online and up to $2,522 for foreign schools, so confirm which award year your term falls in or check the live GI Bill calculator.

Why is my GI Bill housing allowance so low?

The most common reasons are online-only enrollment, which replaces your local rate with the lower national online figure, being on active duty, which suppresses the housing portion entirely, a lower eligibility tier from fewer than 36 months of qualifying service, or a course load that is above half-time but below full-time, which prorates the payment. A partial first or last month also produces a smaller check that is not an error.

Do I get the housing allowance if I take classes online?

Yes, but at a reduced rate. Online-only students receive a flat national rate, up to $1,169 per month for terms through July 31, 2026, rising to up to $1,261 per month for terms on or after August 1, 2026, at the full tier, rather than their school's local rate. Taking even one course that meets in person on campus qualifies you for the full local resident rate instead, which is often substantially higher.

Does the GI Bill pay housing allowance during summer or winter break?

No. The MHA is paid only for days you are actively enrolled. During breaks between terms there is no housing payment, and the months bordering a break are prorated for the partial enrollment. Budget for the housing allowance as in-session income only, not a steady monthly salary.

Is the GI Bill housing allowance taxable?

No. The Monthly Housing Allowance is a non-taxable benefit. You will not receive a tax form for it and you do not report it as income on your federal return.

Bottom Line

The GI Bill housing allowance is not a flat benefit, it is a calculation, and the inputs are your school's location, your service-based tier, and your course load, with hard overrides for online and active-duty students. The single biggest swing factors are choosing an in-person over an online program and the ZIP code of the campus you pick, either of which can change your monthly check by hundreds or even a thousand dollars. Before you commit to a school or sign a lease, confirm your tier on your Certificate of Eligibility and run your real school and enrollment through the GI Bill calculator. For how the housing piece sits next to tuition and books, and for how the underlying BAH rate is built from your duty ZIP and dependent status, see the BAH with vs without dependents guide.