TSP for Service Members in 2026: BRS Match, Limits, and a TSP Calculator

TSP calculator and 2026 guide for service members: how the Blended Retirement System match works, the $24,500 deferral limit, catch-up, Roth vs traditional.

The Thrift Savings Plan is the closest thing the military has to a 401(k), and a TSP calculator is the fastest way to see what your contributions and match actually grow into. For anyone who joined under the Blended Retirement System it is no longer optional background noise. It is a core part of your retirement, sitting right alongside the pension you may or may not stay in long enough to collect. The frustrating part is that the rules change every January, the dollar limits move, and most of the explanations you find online are written for civilian federal employees who never deal with combat-zone pay or a deployment that doubles their savings room for a few months.

This guide is built for the 2026 plan year and for the uniformed-services side of TSP specifically. We will walk through what the government actually puts into your account under BRS, the exact contribution limits for 2026, how catch-up works as you get older, the Roth versus traditional decision, and the combat-zone rules that can let you stuff far more into the account than the headline number suggests. Wherever a real dollar figure matters to your own paycheck, run it through the TSP calculator so you are looking at your numbers rather than an example. The limits below are accurate for 2026, but your share, your match, and your projected balance depend entirely on your paygrade and how much you elect to contribute.

What the Government Actually Puts In: the BRS Match

If you entered service on or after January 1, 2018, you are automatically under the Blended Retirement System, and the defining feature of BRS is that the government contributes to your TSP. Under the legacy High-3 pension, the plan was yours alone with no match. Under BRS, you get two separate streams of government money, and understanding the difference between them is the single most valuable thing in this guide. If you are still deciding whether BRS or the legacy pension fits your career plan, our BRS vs High-3 guide breaks down the full trade-off.

The automatic 1 percent

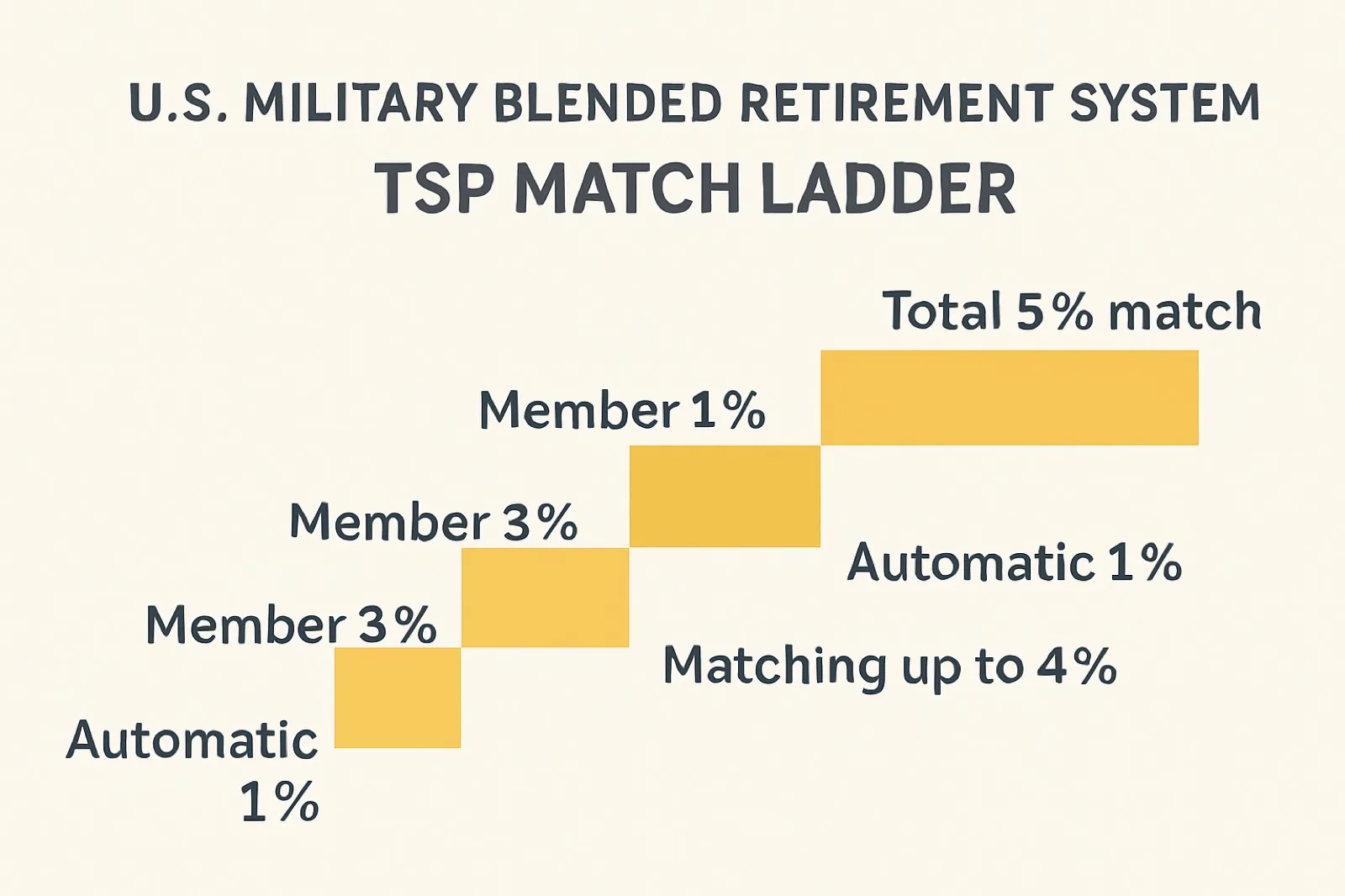

The first stream is the Service Automatic (1%) Contribution. Your branch deposits an amount equal to 1 percent of your basic pay into your TSP every pay period whether or not you contribute a single dollar of your own. For BRS members who joined on or after January 1, 2018, this automatic contribution begins after 60 days of service. It is free money with no action required on your part beyond showing up.

The matching 4 percent

The second stream is the Service Matching Contribution, and this is the one people leave on the table. The match works on a ladder:

| Your contribution | What the service adds | Running match total |

|---|---|---|

| 1% of basic pay | 1% (dollar for dollar) | 1% |

| 2% | 1% | 2% |

| 3% | 1% | 3% |

| 4% | 0.5% (50 cents on the dollar) | 3.5% |

| 5% | 0.5% | 4% |

Put it together and the picture is simple, and it is why TSP matching at 5 percent is the number every service member should memorize. Contribute 5 percent of your own basic pay and the government adds 5 percent on top: the 1 percent automatic plus the full 4 percent match. That is an immediate 100 percent return on your first 5 percent before the markets do anything at all. Contribute less than 5 percent and you are walking away from part of that match every payday, which is the most expensive mistake in military personal finance.

A common point of confusion: new members are auto-enrolled at a 3 percent default contribution, not 5 percent. Three percent is enough to feel like you are "doing TSP," but it leaves a full 1 percent of matching money on the table every pay period. If you do nothing else after reading this, log into your pay system and bump your election to at least 5 percent.

Vesting: which money is really yours

Not all of these dollars belong to you on day one. The concept here is vesting, which is the point at which money in your account becomes permanently yours. Your own contributions and their earnings are always 100 percent yours, immediately, and the Service Matching Contributions vest immediately as well. The one piece with a waiting period is the Service Automatic (1%) Contribution, which requires two years of service before it vests. Separate before that two-year mark and you forfeit the automatic 1 percent, though you keep everything else. If you are weighing an early separation, this is worth checking against your retirement timeline so you know exactly what you would leave behind.

The 2026 Contribution Limits

The IRS resets these numbers every year for inflation, and 2026 brought a meaningful bump. Here are the figures that govern how much you can put into TSP this year.

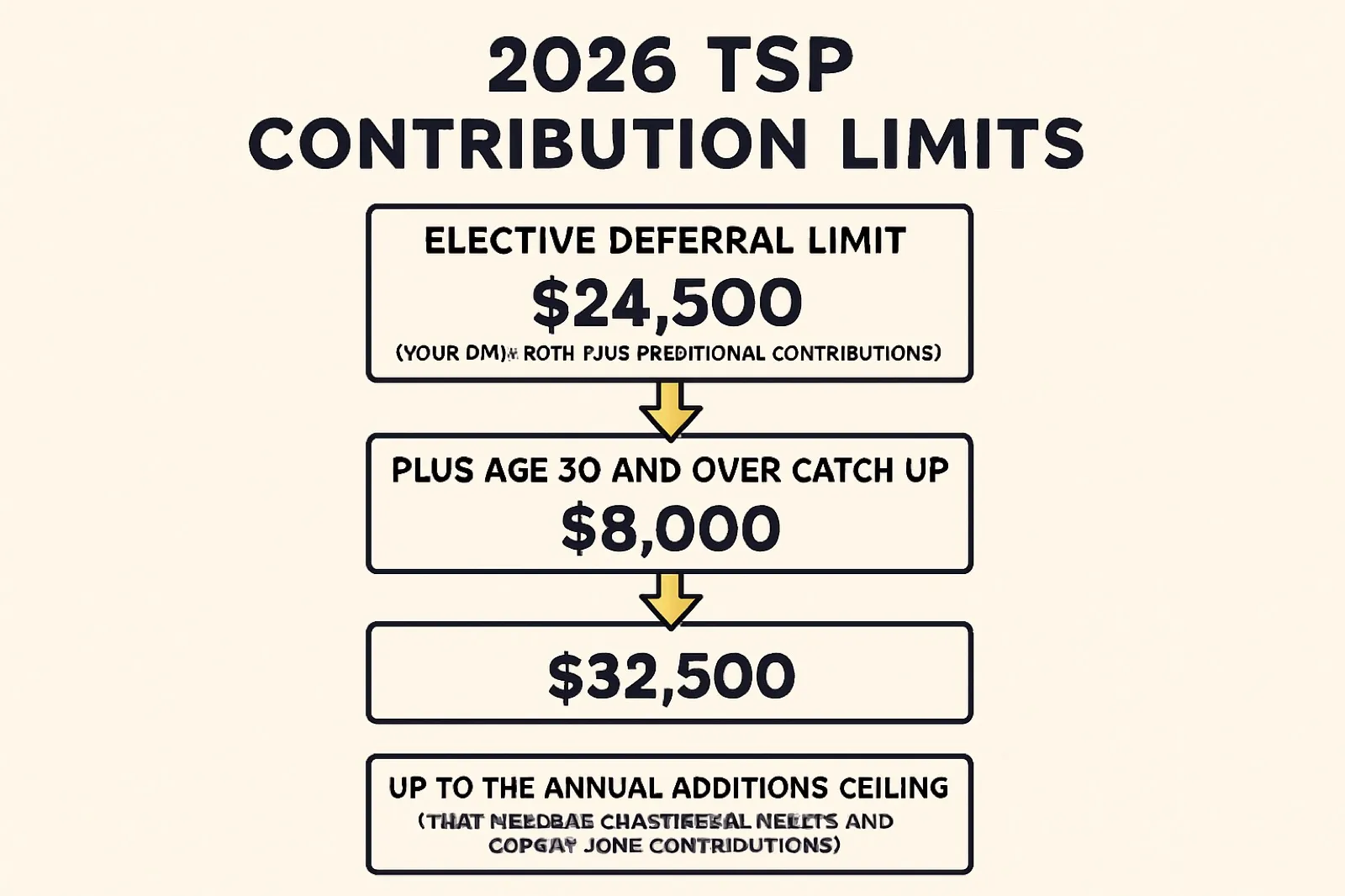

The elective deferral limit: $24,500

The core cap is the elective deferral limit under Internal Revenue Code section 402(g). For 2026 it is $24,500, up from $23,500 in 2025. This is the most-out-of-pocket figure that matters to most people: the total of your own traditional and Roth TSP contributions across the calendar year cannot exceed it. The government match does not count against this limit; only the money that comes out of your paycheck does.

Catch-up contributions if you are 50 or older

If you are age 50 or older at any point during 2026, you can contribute beyond the elective deferral limit. The 2026 catch-up amount is $8,000, which sits on top of the $24,500 base. That brings the total of your own contributions to $32,500 for the year if you are 50 or older.

TSP handles this through what it calls the spillover method. You do not file a separate catch-up election. You simply keep contributing, and once your regular contributions hit the $24,500 ceiling, additional dollars automatically spill over and count toward the catch-up limit. No extra paperwork.

The age 60 to 63 "super catch-up"

SECURE Act 2.0 created an enhanced catch-up for a narrow age band. If you turn age 60, 61, 62, or 63 at any point in 2026, your catch-up limit is $11,250 instead of $8,000. That raises your personal maximum to $35,750 for the year. The moment you turn 64, you drop back to the standard $8,000 catch-up. For most active-duty members this band is irrelevant, but it matters for senior officers and for reservists or guardsmen who are still contributing late in a long career.

A Roth catch-up wrinkle for high earners

One more SECURE 2.0 rule kicked in that affects higher earners. If your prior-year Social Security (FICA) wages were above $150,000, any catch-up contributions you make must go into the Roth side of your TSP once you have maxed the traditional pre-tax amount. Your payroll office handles the mechanics, but it is worth knowing so the change in tax treatment does not surprise you.

Roth or Traditional: How to Think About It in Uniform

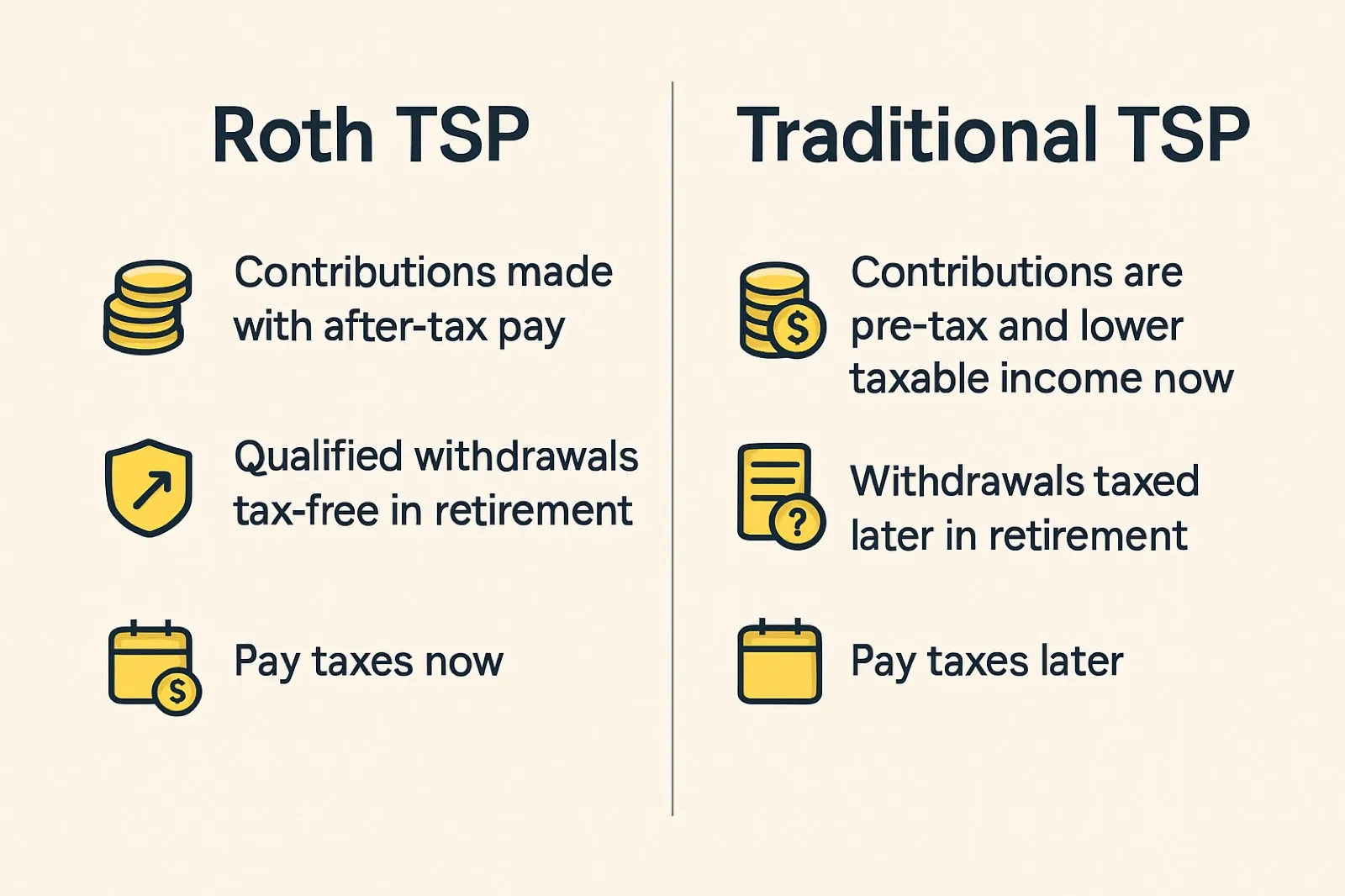

Every dollar you contribute can go into either the traditional (pre-tax) or Roth (after-tax) bucket, and both share the same combined $24,500 limit. The deciding question is whether you would rather take the tax break now or later.

The basic trade

Traditional contributions come out before income tax, lowering your taxable pay today, and you pay ordinary income tax when you withdraw in retirement. Roth contributions are made with money you have already paid tax on, and qualified withdrawals in retirement, including all the growth, come out completely tax-free.

Why Roth often wins for junior members

For most enlisted members and junior officers, Roth is the stronger default, whether you think of it as Army Roth TSP, Navy, Air Force, or any other branch, and the reason is your tax bracket. Early in a career your taxable income is low, your marginal rate is low, and the tax deduction from a traditional contribution is worth relatively little. Lock in that low rate now with Roth, let decades of growth compound, and pull it out tax-free later when your retirement income, and possibly tax rates in general, could be higher. The closer you are to a high-earning, late-career position, the more a traditional contribution's immediate deduction starts to compete.

The combat-zone case for Roth is overwhelming

This is where military TSP diverges hard from the civilian playbook. When you contribute Roth dollars from tax-exempt combat zone tax exclusion pay, you get a result a civilian can never get: money that was never taxed going in, and never taxed coming out. If you are deployed to a designated combat zone, prioritizing Roth contributions is close to a no-brainer. We dig into the mechanics below, and you can sanity-check how much of your deployment pay qualifies with the combat pay calculator. For the full picture on which zones qualify and how the exclusion works, see our combat pay and tax-free zones guide.

Deployment and the Combat-Zone Rules

A deployment to a designated combat zone changes the math in two big ways, and both work in your favor.

Tax-exempt contributions and a higher ceiling

Pay earned in a combat zone is generally excluded from federal income tax, and you can contribute that tax-exempt pay to your TSP. There is a separate, larger ceiling that comes into play here. Alongside the $24,500 elective deferral limit there is the annual additions limit under section 415(c), which for 2026 is $72,000. This ceiling counts everything that lands in your account in the year: your contributions, your service's automatic 1 percent, the matching, and tax-exempt combat-zone contributions.

For most years the $24,500 deferral limit is the one you bump into first. But while you are receiving tax-exempt combat-zone pay, your own contributions are measured against the much higher $72,000 annual additions limit instead. That is what lets deployed members pour far more into TSP during those months than they ever could stateside.

A planning note on Roth in a combat zone

There is a subtle interaction worth flagging. Traditional contributions made from tax-exempt pay grow tax-deferred, but only the original tax-exempt principal comes out tax-free later; the earnings are taxed on withdrawal. Roth contributions from that same tax-exempt pay let both the principal and all the earnings come out tax-free, assuming you meet the qualified-withdrawal rules. That is why deployed members who can afford it lean heavily on Roth: it converts a one-time tax break on the principal into a lifetime tax break on the growth too.

Where Your Money Goes: TSP Funds in Brief

Choosing a contribution amount is only half the decision. The other half is where it gets invested. TSP keeps the menu deliberately short, which is a feature rather than a limitation.

The core funds

There are five individual funds. The G Fund holds government securities and never loses principal, which makes it the safe-but-slow option. The F Fund tracks the broad bond market. The C Fund tracks large U.S. companies through an S&P 500 index. The S Fund covers smaller and mid-sized U.S. companies. The I Fund holds international stocks. New money is auto-enrolled into an age-appropriate Lifecycle (L) Fund by default.

Lifecycle funds and the auto-enrollment default

The L Funds are target-date funds. You pick the one closest to the year you expect to start drawing the money, and the fund automatically shifts from mostly stocks when you are young toward more bonds and G Fund as that date approaches. For someone who does not want to manage allocations, leaving your contributions in the age-appropriate L Fund you were auto-enrolled into is a perfectly defensible choice. Your long-run TSP rate of return depends mostly on this stock-versus-bond mix, not on trying to time the market. The expense ratios across all TSP funds are among the lowest you will find anywhere, which over a 20- or 30-year career quietly adds up to real money compared with retail funds that charge ten or twenty times as much.

Run the Numbers: a 2026 Action Plan and TSP Calculator

Here is the short version, in order of priority:

- Contribute at least 5 percent of basic pay. This captures the full government match. Anything less is leaving guaranteed money behind.

- Default to Roth if you are junior or deployed. Lock in your low tax bracket now and prioritize Roth hard when contributing from tax-exempt combat-zone pay.

- Know the 2026 numbers. $24,500 elective deferral limit, $8,000 catch-up at 50+, $11,250 catch-up at 60 to 63, $72,000 annual additions ceiling.

- Use the spillover method. If you are 50 or older, just keep contributing past the base limit; catch-up happens automatically.

- Pick a fund and leave it alone. An L Fund matched to your retirement date is a reasonable set-and-forget choice with rock-bottom fees.

- Mind the two-year vesting cliff on the automatic 1 percent if you might separate early.

The single biggest lever you control is your own contribution rate. To see what a given percentage of your pay actually grows into over a full career, with the match layered in, run your real paygrade and election through the TSP calculator. A military TSP calculator will show you the compounding effect of the match, and the assumed TSP rate of return, in a way that a flat percentage never quite conveys.

Frequently Asked Questions

What are the 2026 TSP contribution limits?

Your own contributions are capped at the $24,500 elective deferral limit for the year, plus $8,000 in catch-up if you are 50 or older ($11,250 if you turn 60 to 63 in 2026). The government match is separate and does not count against that figure. If you are contributing tax-exempt combat-zone pay, you are instead measured against the $72,000 annual additions limit.

What is the BRS TSP match?

Under the Blended Retirement System you get two streams of government money: a Service Automatic Contribution of 1 percent of basic pay regardless of what you put in, plus a Service Matching Contribution on the first 5 percent you contribute. Contribute 5 percent and the service adds 5 percent total (the 1 percent automatic plus a full 4 percent match). Contribute less and you forfeit part of that match every pay period.

Roth TSP vs traditional TSP for military?

Traditional contributions are pre-tax and lower your taxable pay now, with ordinary income tax due on withdrawal. Roth contributions are after-tax, and qualified withdrawals, including growth, come out tax-free. For most junior enlisted and officers in a low bracket, Roth is the stronger default, and it is close to a no-brainer when you are contributing from tax-exempt combat-zone pay.

What are the pros and cons of a TSP annuity?

A TSP life annuity converts part of your balance into a guaranteed payment you cannot outlive, which removes the risk of running out of money. The trade-offs are that the decision is generally irreversible, the money is no longer invested for growth, and depending on the option you choose it may leave little or nothing to heirs. It suits members who value certainty over flexibility.

TSP annuity vs monthly payments?

A TSP annuity is a separate insured product that locks in a fixed payment for life, while TSP installment (monthly) payments draw down your own invested balance and can be started, stopped, or adjusted. Installments keep your money invested and accessible but carry the risk of depleting the account; the annuity trades that flexibility for a guaranteed lifetime income. Many members blend the two.

How does TSP matching work for service members?

Matching applies only to BRS members on the first 5 percent of basic pay you contribute each pay period. The first 3 percent is matched dollar for dollar, and the next 2 percent is matched at 50 cents on the dollar, for a 4 percent match; add the automatic 1 percent and the service contributes 5 percent when you contribute 5 percent. The match is always deposited as traditional money even if your own contributions are Roth, and it is tracked against the $72,000 annual additions limit rather than the $24,500 deferral cap. When you leave the service your balance stays yours to keep in TSP, roll to an IRA, or move elsewhere, subject to the two-year vesting rule on the automatic 1 percent.