BRS vs High-3: A Military Retirement Calculator Comparison

Military retirement calculator comparison of BRS vs High-3 for 2026 - the 2% vs 2.5% multiplier, TSP matching, continuation pay, and which plan pays more.

A military retirement calculator can tell you whether the Blended Retirement System or the legacy High-3 plan pays you more, but the honest answer depends on one thing more than any other: how long you stay in uniform. The two systems are built on opposite bets. High-3 rewards the people who reach 20 years with a richer pension and gives nothing to everyone who leaves early. BRS trims that pension a little but hands a real, portable retirement account to every service member from day one, even the roughly 80 percent who separate before they ever qualify for a pension. For most people in BRS military service today, those funded retirement benefits are the part that actually matters.

This guide walks through exactly how each plan is calculated, who is allowed to be in which one in 2026, and the trade-offs that decide which one comes out ahead for your specific career. The dollar figures swing a lot with your final paygrade, your years of service, and the returns your Thrift Savings Plan earns, so rather than quote example numbers that go stale, plug your own situation into the military retirement calculator as you read. It models both plans side by side using your inputs.

The Short Version

There is no universal winner. The plan that pays more is the one that matches your career length and your saving habits.

- If you are confident you will serve a full 20 or more years and you do not contribute much to TSP, the legacy High-3 plan usually produces a larger lifetime payout because of its higher pension multiplier.

- If there is real uncertainty about reaching 20 years, or you contribute steadily to TSP and let it grow, BRS often wins because the matched account follows you out the door whether you stay 4 years or 24.

The catch in 2026 is that for almost everyone serving today the choice is already made. Which plan you are in was locked years ago by when you entered service. The comparison still matters, because it shapes how hard you should be saving and whether the pension you are counting on is as large as you think.

Who Is in Which Plan in 2026

You do not get to pick your retirement system today. It was set by your entry date, and the one-time switch window closed years ago.

Automatically in BRS

Anyone who first entered a uniformed service on or after January 1, 2018 is automatically covered by the Blended Retirement System. If your Date of Initial Entry to Military Service falls on or after that date, BRS is your plan and there was never an alternative. That now covers every junior enlisted member and junior officer with eight years of service or less.

Grandfathered under legacy High-3

Every member who was serving on or before December 31, 2017 was grandfathered into the legacy High-3 (also called High-36) plan. No one serving before that date was ever moved into BRS against their will.

The opt-in window is closed

Members who were already serving but had relatively little time in (fewer than 12 years of active service, or fewer than 4,320 retirement points for Guard and Reserve) got a one-time chance to opt into BRS. That window ran the full 2018 calendar year and ended December 31, 2018. It has not reopened, and there is no expectation that it will. If you were eligible and did not opt in, you are still under High-3 today.

The practical takeaway: in 2026 this is mostly a planning question, not a decision you can still make. Confirm which plan you are in by checking your DIEMS date and your branch's personnel record. The rest of this guide explains what that plan actually does for you.

How the Legacy High-3 Plan Works

High-3 is a traditional defined-benefit pension, and it is straightforward.

The pension formula

You earn a monthly pension only if you serve at least 20 years. The formula is:

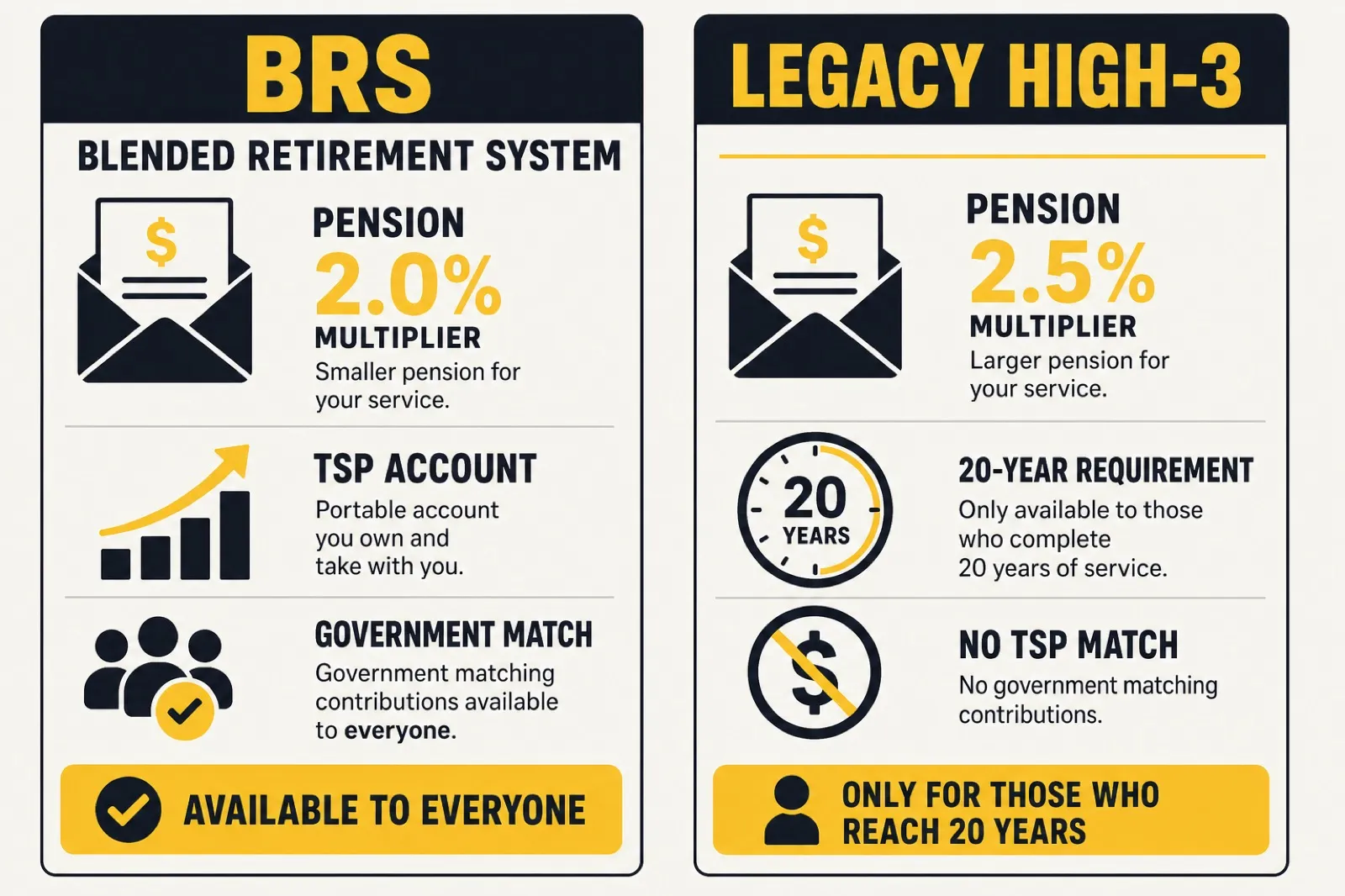

Years of service x 2.5% x average of your highest 36 months of basic pay

The "high 3" name comes from that highest-36-months average, which for most careers is the basic pay over your final three years. At 20 years of service the multiplier works out to 50 percent of that average (20 x 2.5%). Stay 30 years and you reach 75 percent (30 x 2.5%). The pension is paid for life starting the month you retire, and it gets an annual cost-of-living adjustment tied to inflation.

One detail trips people up: the average is built from basic pay only. It does not include Basic Allowance for Housing, Basic Allowance for Subsistence, special pays, or bonuses. So the high-3 figure that feeds the formula is almost always lower than your total take-home pay in those final years. A promotion in your last three years raises the average, but only the basic-pay portion of it counts. When you model your pension in the retirement calculator, the basic pay you enter is what drives the result, not your gross compensation.

There is also a partial-year nuance worth knowing. Months of service count too, not just whole years, so 20 years and 6 months produces a slightly higher multiplier than a flat 20 years. A High-3 calculator handles the fractional math for you, but it is one more reason the exact figure is hard to eyeball. For a step-by-step run through the legacy pension math, see the High-3 retirement walkthrough.

What High-3 does not include

High-3 comes with no government money in your Thrift Savings Plan. You can and should still contribute to TSP under High-3, but every dollar in that account is yours alone with no automatic or matching contributions from the service. And the hard edge of the plan is this: serve 19 years and 11 months, then separate, and the pension is zero. There is no partial pension. This all-or-nothing design is the single biggest reason BRS was created.

How the Blended Retirement System Works

BRS is "blended" because it pairs a smaller traditional pension with a funded retirement account, plus a mid-career bonus.

A smaller pension multiplier

BRS uses the same structure as High-3 but with a lower multiplier:

Years of service x 2.0% x average of your highest 36 months of basic pay

At 20 years that is 40 percent of your high-3 average instead of 50 percent. That 20 percent haircut on the pension (2.0% versus 2.5%) is the price you pay for everything else BRS adds. Like High-3, the BRS pension still requires 20 years to vest and still receives an annual cost-of-living adjustment.

Automatic and matching TSP contributions

This is the heart of BRS and the part that benefits the majority of members who never reach 20 years. The service puts money into your Thrift Savings Plan:

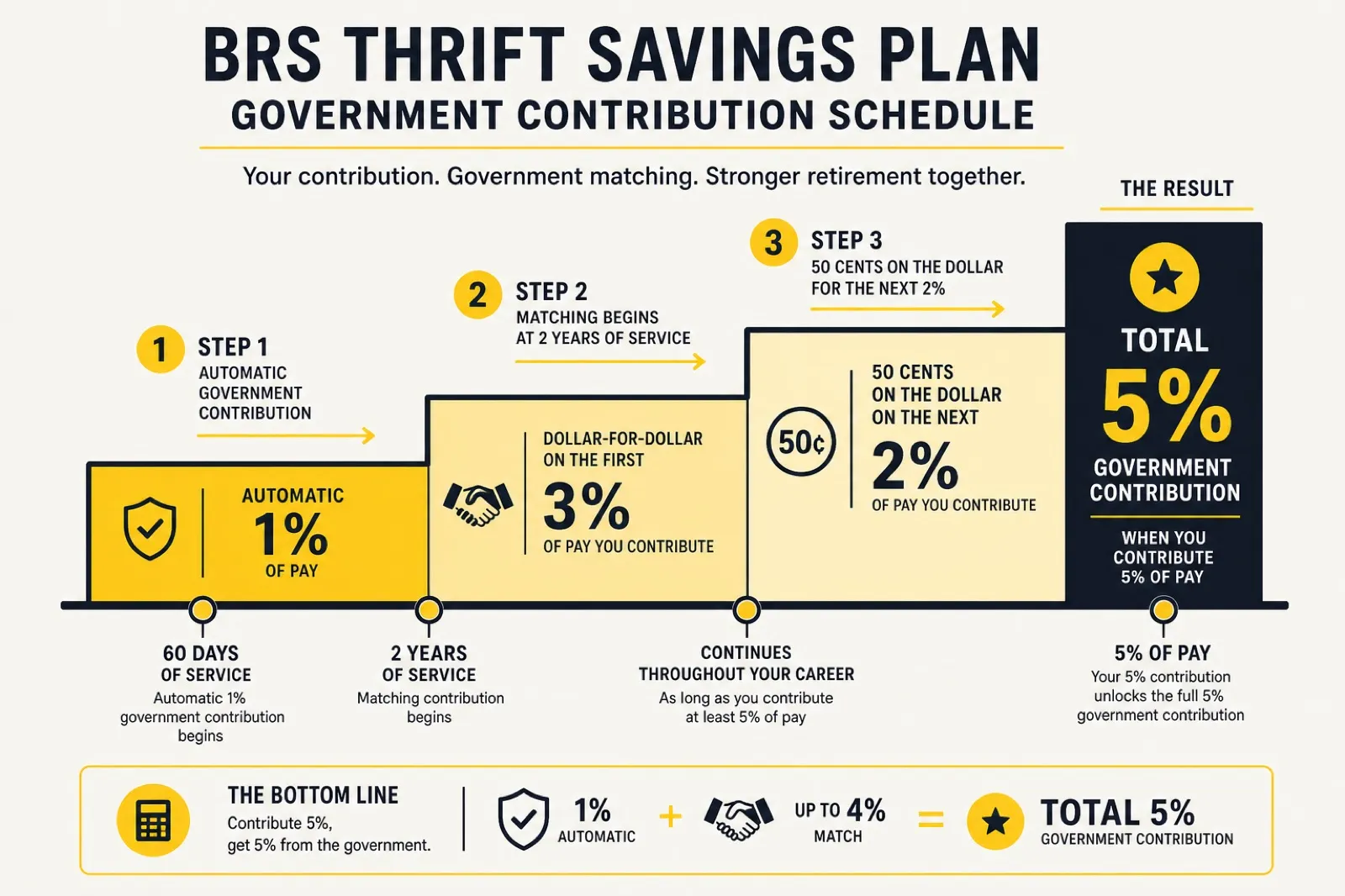

- A Service Automatic Contribution of 1% of your basic pay every pay period, whether or not you contribute anything yourself. It begins after you have served 60 days.

- Service Matching Contributions on top of that. The service matches your first 3% dollar for dollar, then matches the next 2% at 50 cents on the dollar. There is one timing catch that trips up junior members: if you first entered service on or after January 1, 2018, matching does not begin until you complete two years of service (specifically two years and one day). Before that point you receive only the automatic 1%, even if you are already contributing 5% of your own pay. No matching dollars are deposited at all until you cross that two-year mark. (Members who opted into BRS from the legacy system in 2018 received matching right away; the two-year wait applies to new accessions from 2018 onward.)

Put in 5% of your own basic pay and the math looks like this:

| Your contribution | Service automatic | Service match | Total into TSP |

|---|---|---|---|

| 5% | 1% | 4% | 10% of basic pay |

So contributing 5% yourself turns into 10% going into the account, once you are past the two-year mark where matching kicks in. In your first two years you still want to be contributing 5%, but the deposit is only your own 5% plus the automatic 1% until matching starts. Contributing less than 5% after that leaves free matching money on the table, which is the most common and most costly mistake BRS members make. You can run your own contribution rate through the TSP calculator to see the long-run difference a few percentage points makes.

Vesting: what you keep if you leave

Two different rules apply here, and it is easy to confuse "when does the money show up" with "when is it mine to keep":

- The matching contributions carry no separate vesting wait. For new accessions from January 1, 2018 onward, matching does not even begin until you complete two years of service, but every matching dollar is fully vested the moment it is deposited. There is no scenario where you have matching money sitting in your account that you could forfeit.

- The automatic 1% contributions begin after 60 days but do not vest until you complete two years of service. Leave before two years and you forfeit just that automatic portion. Your own contributions are always yours.

So for a member who separates inside the first two years, the picture is simple: you keep your own contributions, you lose the unvested automatic 1%, and there were never any matching dollars to take in the first place because matching had not started yet. Reach two years and the automatic 1% vests and matching begins, so from that point on the entire government contribution leaves service with you. That portability is the structural advantage High-3 simply does not have.

Continuation pay at mid-career

BRS adds a retention bonus called continuation pay. You become eligible somewhere between completing 8 and 12 years of service, and you must take it before you hit 12 years. In exchange you commit to an additional service obligation, typically four more years.

The amount is a multiplier of your monthly basic pay. The law sets a floor of 2.5 months of basic pay for active-duty members and 0.5 months for drilling Guard and Reserve members, but each service can and does pay more than the minimum depending on the specialty and the year. Because these multipliers are set annually by each branch, do not assume the floor. Check your service's current continuation pay rates for your year group.

The lump-sum option at retirement

If you stay to 20 years under BRS, at retirement you can take part of your future pension as a discounted lump sum. You may choose either 25 percent or 50 percent of the present value of your retired pay, paid up front, in exchange for a reduced monthly check until you reach full Social Security retirement age (age 67 for most people), at which point your monthly pay returns to the full amount.

This sounds attractive and it usually is not. The "discounted present value" means the government applies a discount rate that often makes the lump sum a worse deal than just taking the full monthly pension. Treat the lump-sum option with caution and model it carefully before electing it.

BRS vs High-3 Side by Side

| Feature | Legacy High-3 | BRS |

|---|---|---|

| Pension multiplier | 2.5% per year | 2.0% per year |

| Pension at 20 years | 50% of high-3 pay | 40% of high-3 pay |

| Years to vest pension | 20 | 20 |

| TSP automatic contribution | None | 1% of basic pay |

| TSP matching | None | Up to 4% (5% total gov) |

| Continuation pay | None | Yes, mid-career bonus |

| Lump-sum option at retirement | No | 25% or 50% election |

| Value if you separate before 20 years | $0 pension | Vested TSP travels with you |

Which One Actually Pays More: Using a Military Retirement Calculator

Now the real question. Run the numbers through a military retirement calculator for your own paygrade and years, but here is how to think about the result before you do. A good military pension calculator models both plans against the current military retirement pay chart so you compare real dollars, not rules of thumb.

The break-even depends on TSP returns and career length

The whole comparison comes down to whether the extra TSP money under BRS, compounded over a career and beyond, makes up for the 20 percent smaller pension. The answer hinges on two variables: how long you serve and what return your TSP investments earn over time.

It helps to picture the two plans as different shapes. High-3 is a step function with one giant step at year 20: nothing, nothing, nothing, then suddenly a lifetime pension. BRS is a ramp that starts paying into your account from day one and rises smoothly the whole way. The step function pays more at the very top if you make it there. The ramp pays something to everyone along the path. Which shape pays you more depends entirely on where your own career lands on that line.

- The longer you serve past 20 years, the more the High-3 pension's higher multiplier pulls ahead, because that gap compounds across more years of service and more years of retirement.

- The higher your TSP return and the more you contribute, the more BRS catches up and often surpasses High-3, because the funded account keeps growing for decades.

Scenarios where BRS clearly wins

- You separate before 20 years. This is the big one. Most service members do not reach 20, and for them BRS pays a vested retirement account while High-3 pays nothing at all. If there is meaningful doubt you will stay to 20, BRS is the safer plan by a wide margin.

- You are a disciplined saver. If you reliably contribute at least 5% to capture the full match and let it ride in a low-cost fund, the compounding can outpace the pension difference even across a full career.

Scenarios where High-3 tends to win

- You are certain you will serve 20-plus years and you do not contribute much to TSP. The higher 2.5% multiplier produces a bigger guaranteed lifetime check, and you are not offsetting it with account growth.

- You value a larger guaranteed, inflation-adjusted income over a portable balance you have to manage yourself.

Why it usually does not matter which "wins"

Because your plan is fixed by your entry date, the more useful framing is what to do inside the plan you already have. If you are in BRS, the single highest-return financial move available to you is contributing at least 5% to TSP every single pay period to capture the full match. Skipping it is leaving guaranteed money behind. If you are under High-3, recognize that you have no employer match cushioning your retirement, so your own TSP and savings discipline carries more weight, and reaching 20 years matters enormously because the pension is all-or-nothing.

Common Mistakes to Avoid

A few errors come up over and over:

- Contributing under 5% in BRS. The match is free money with an immediate, guaranteed return. Anything less than 5% of your own pay forfeits part of it.

- Assuming the lump sum is a bonus. It is a discounted advance on money you already earned, and the discount usually favors the government. Model it before electing.

- Forgetting the 2-year vesting on the 1%. If you might separate very early, know that the automatic 1% is not yours until two years of service. Your matches and your own contributions always are.

- Banking on a pension you may not reach. Under either plan the pension needs 20 years. Plan your finances so a separation at 10 or 15 years does not leave you empty-handed - which under BRS means feeding the TSP, and under High-3 means saving even harder on your own.

Frequently Asked Questions

What is the BRS in the military?

The BRS is the Blended Retirement System, the retirement plan that automatically covers anyone who first entered a uniformed service on or after January 1, 2018. It blends a smaller defined-benefit pension (a 2.0% multiplier instead of High-3's 2.5%) with automatic and matching Thrift Savings Plan contributions and a mid-career continuation pay bonus. Unlike the legacy pension, its TSP retirement benefits travel with you even if you separate before 20 years.

BRS vs High-3: which is better?

Neither is universally better; the right plan depends on how long you serve and how much you save. High-3 usually pays more to members who reach 20-plus years and contribute little to TSP, thanks to its higher 2.5% pension multiplier. BRS usually pays more to everyone who separates early or who reliably contributes at least 5% to capture the full match. Run both through a military retirement calculator with your own numbers to see the gap.

BRS vs current retirement system?

The BRS is the current retirement system for service members today. Everyone who joined on or after January 1, 2018 is on it automatically, so for new and junior members there is no other option. The legacy High-3 plan still exists only for those who were grandfathered in by serving on or before December 31, 2017.

BRS vs legacy retirement?

The legacy retirement system is the High-3 plan, a pure defined-benefit pension with a 2.5% multiplier and no government TSP money. BRS lowers the multiplier to 2.0% but adds the 1% automatic contribution, up to 4% matching, continuation pay, and a lump-sum option at retirement. The core trade-off is a 20 percent smaller pension in exchange for a portable, funded account.

What is the average military pension after 20 years?

There is no single average figure because the pension is driven entirely by your final paygrade and your highest-36-months basic pay. At 20 years, High-3 pays 50 percent of that average (20 x 2.5%) and BRS pays 40 percent (20 x 2.0%). Because basic pay varies widely by rank, the only accurate estimate is your own number plugged into the retirement calculator.

What are the pros and cons of the Blended Retirement System?

The pros: a vested, portable retirement account from early in your career, free matching money worth up to 4% of basic pay, continuation pay at mid-career, and real value even if you never reach 20 years. The cons: a smaller 2.0% pension multiplier, a two-year wait before matching begins for 2018-onward accessions, and a lump-sum option that usually favors the government. For the majority who separate before 20 years, the pros clearly outweigh the cons.

Bottom Line

BRS vs High-3 is less a contest with a single winner than a question of fit. High-3 pays more to the career member who reaches 20-plus years and does not lean on TSP. BRS pays more to nearly everyone else, especially the majority who separate before 20 and the disciplined savers who capture the full match. For 2026 the practical move is to confirm which plan your entry date placed you in, then optimize the military retirement benefits inside it: max the match if you are BRS, guard your road to 20 years if you are High-3, and run your real numbers through the retirement calculator rather than trusting any rule of thumb.

For related planning, see how your Thrift Savings Plan contributions compound over a career and where the TSP match fits into the larger picture of your military pay in the TSP for service members guide.