National Guard & Reserve Retirement: The Points System Explained

How National Guard and Reserve retirement works in 2026 - earning retirement points, the 360-point year, the 20 good years rule, pay at age 60, and reduced-age retirement.

National Guard and Reserve retirement runs on a different engine than the active-duty pension most people picture. An active-duty member serves 20 years and starts drawing a check the month they retire. A Guard or Reserve member earns retirement points across their career, needs 20 qualifying years to vest, and then usually waits until age 60 to see the first payment. The math, the timing, and the eligibility rules are all distinct, and missing how they fit together is the fastest way to misjudge what your service is actually worth.

This guide explains the points system from the ground up: how you earn points, what counts as a "good year," how points convert into the years-of-service figure that drives your pension, when the money starts, and how mobilizations can pull that start date earlier than 60. Because the final dollar figure depends on your point total, your final paygrade, and the basic pay tables in effect when your pay begins, run your own numbers through the military retirement calculator as you read rather than trusting a single example. The rules below are accurate for 2026; the dollar amounts are yours to plug in.

The Short Version

Guard and Reserve retirement, often called a non-regular retirement, works in three stages:

- Earn points. Every drill, every day of active duty, every annual training, and your yearly membership all add retirement points to your record.

- Bank 20 good years. You need 20 qualifying years, each with at least 50 points, to vest in the pension. Fewer than 20 and there is no pension at all.

- Get paid at 60. Unlike active-duty retirees, you usually do not draw retired pay the moment you stop drilling. Payment starts at age 60, though qualifying active-duty mobilizations can move that date earlier, down to a floor of age 50.

The pension itself uses the same building blocks as the active-duty formula, with one swap: instead of plugging in raw years of service, you divide your lifetime points by 360 to get an equivalent years figure, then apply the standard multiplier. That single substitution is the heart of the whole system.

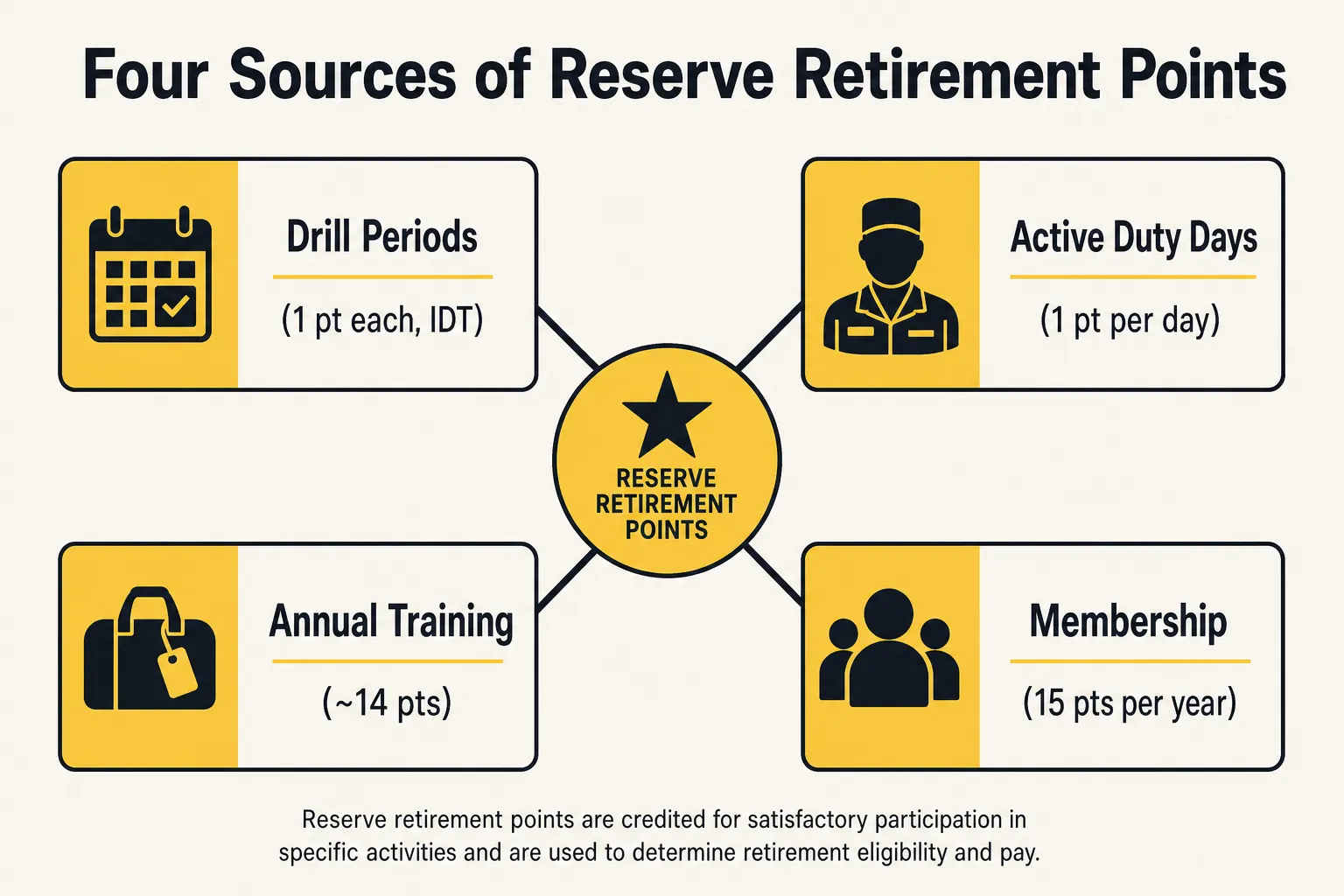

How You Earn Retirement Points

Points are the currency of Guard and Reserve retirement. They come from four sources, and they accumulate for your entire career - every point you ever earn counts toward the final pension, not just the points from your last few years.

Drill periods (inactive duty training)

The classic "one weekend a month" is built from individual drill periods. Each drill period is worth 1 point. A standard drill weekend is four drill periods - two on Saturday, two on Sunday - so a normal weekend earns 4 points. Across a typical training year of 12 weekends, that is 48 points from drills alone. These are inactive duty training (IDT) points, and they are capped (more on that below).

Active duty and active duty for training

Every day on active orders earns 1 point per day. This includes your two-week annual training, any active duty for training, and full mobilizations. A two-week annual training period of 14 days adds 14 points. A 12-month mobilization can add roughly 365 points by itself, which is why a deployment year is so valuable to a Reserve pension.

Membership points

Simply being in a Reserve component earns you 15 membership points per year, awarded for each year of satisfactory service. You get these for belonging, on top of everything you earn from showing up.

How a normal year adds up

Put the routine pieces together for a standard training year and you get a feel for the pace:

| Source | Points |

|---|---|

| 12 drill weekends (48 drills x 1) | 48 |

| 14-day annual training | 14 |

| Membership | 15 |

| Typical year total | about 77 |

That is a representative year, not a rule. Schools, additional duty, and mobilizations all push the total higher. The exact mix is what you should feed into a retirement calculator once you know your real point statement.

The Annual Point Caps

Two ceilings limit how many points a single year can produce, and they work differently.

The inactive-duty cap

Points from inactive sources - drills, membership, correspondence courses, equivalent instruction - are capped per retirement year. For retirement years that include October 30, 2007 and any year after, the cap on inactive points is 130 points. Earlier years carried a lower cap (90 points from 2000 to 2007, and 75 before that), which matters only if you are reconstructing an older record.

The overall annual cap

The total points in any one retirement year cannot exceed 365 points (366 in a leap year). Here is the key nuance: active-duty points are not subject to the 130 inactive cap. So a member who drills all year and also mobilizes can blow past 130 because the extra points come from active service. The 130 ceiling only limits the inactive portion; the active portion fills the rest up to 365 or 366. A heavy mobilization year therefore lands near the full annual maximum.

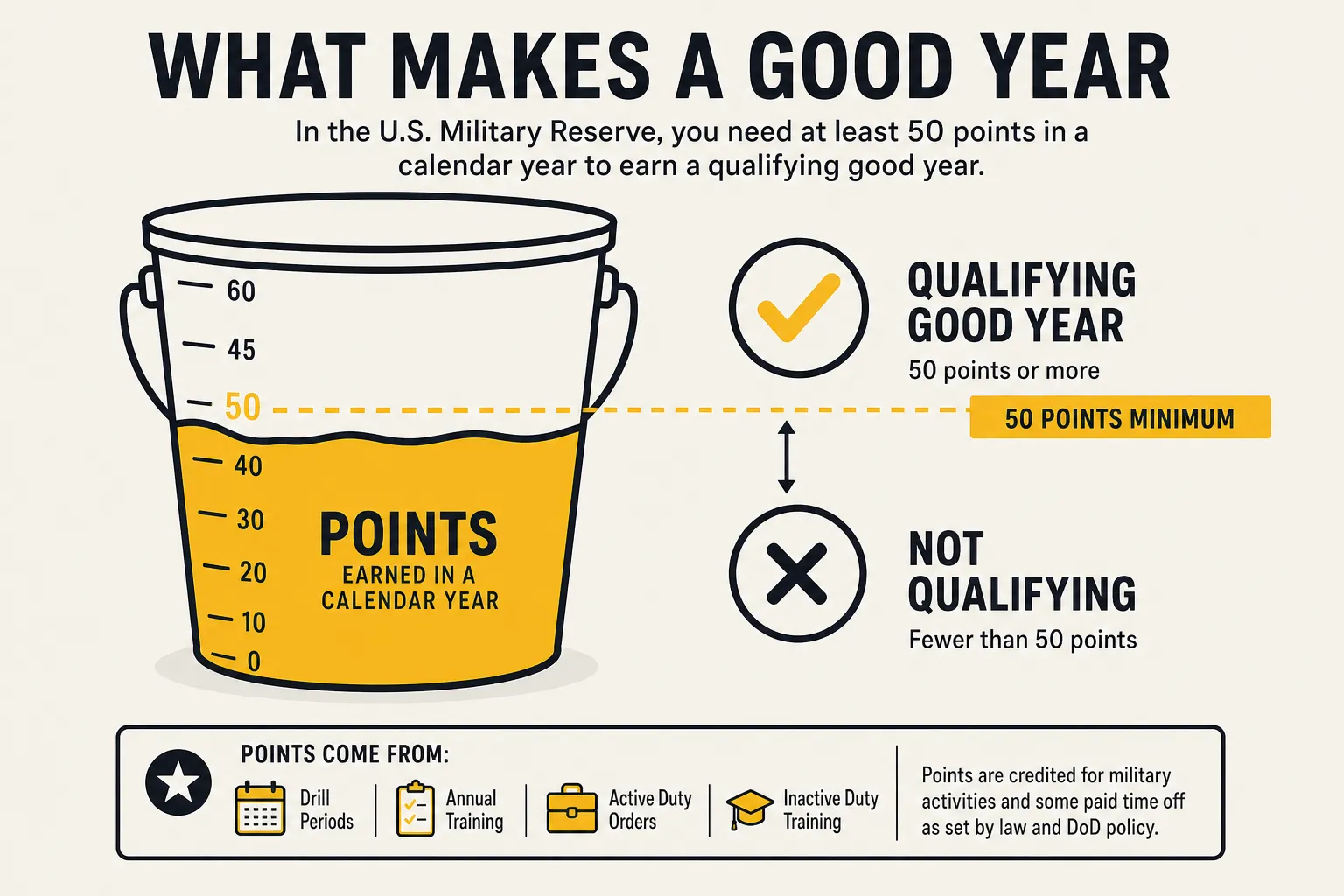

What Counts as a Good Year

This is the rule that decides whether a year of service helps your pension at all, and it trips up more people than any other part of the system.

A qualifying year - the term most people use is a "good year" - is a retirement year in which you earn at least 50 retirement points. Hit 50 or more and the year is a good year that counts toward the 20 you need. Fall short of 50 and the entire year is non-qualifying for the 20-year threshold, even though every point you did earn still counts later in the pension math.

That split is the part to internalize:

- For the 20-year vesting requirement, only good years (50+ points) count. You need 20 of them to be eligible for a pension at all.

- For the pension amount, every point from every year counts, including points from years that fell short of 50. No earned point is ever wasted in the dollar calculation - but a year under 50 points does not advance you toward the 20-good-year finish line.

So a member who strings together 19 good years and one weak year with 40 points has a problem: that weak year does not count toward the 20, even though the 40 points will still feed the pension formula if they eventually vest. Watching your point total each year to make sure you clear 50 is the single most important habit in protecting a Guard or Reserve retirement.

Converting Points to Years: The 360 Rule

Here is where the points system connects to the familiar pension formula. The active-duty pension multiplies years of service by a percentage. Guard and Reserve members do not have a clean years-of-service number because their service is part-time, so the law converts points into an equivalent years figure:

Equivalent years of service = total lifetime points / 360

Note the number is 360, not 365. The convention treats 360 points as one year of creditable service for the pension multiplier. This is deliberate and it works in your favor compared to a 365 divisor - it takes fewer points to reach each equivalent year.

Once you have that equivalent years figure, the rest of the formula is identical to the active-duty pension:

Equivalent years x multiplier x high-36 base pay = monthly retired pay

The multiplier is the same one your retirement system uses. Under the legacy High-3 plan it is 2.5% per equivalent year. Under the Blended Retirement System, it is 2.0% per equivalent year. Which one applies to you depends on when you entered service, the same way it does for active-duty members.

A worked illustration

Suppose a Reservist retires with 3,600 total points under the legacy High-3 plan. Convert the points:

- 3,600 / 360 = 10 equivalent years

- 10 x 2.5% = 25% multiplier

That member's pension is 25% of their high-36 base pay. The same point total under BRS would be 10 x 2.0% = 20%. The dollar value then depends entirely on which high-36 base pay applies, which we cover next. Because both your point total and your paygrade are personal, the only accurate figure is the one the military retirement calculator produces from your inputs.

Which Base Pay the Formula Uses

A common misconception is that the pension uses the basic pay you earned while drilling. It does not. The retired pay base is the high-36 average - the average of your highest 36 months of basic pay - just like the active-duty High-3 plan.

For a Guard or Reserve retiree, that average is built from the basic pay tables in effect for the 36 months immediately preceding the date your retired pay actually begins, for the rank and years of service you would hold. Because most members do not start drawing pay until age 60, the high-36 average typically reflects the pay tables in effect around the time you turn 60, not the (lower) tables from when you stopped drilling years earlier. That timing quietly increases the pension, since basic pay tables rise over time with annual military pay raises.

As with every version of this formula, only basic pay feeds the average. Drill pay differentials, Basic Allowance for Housing, special pays, and bonuses are not part of it. When you enter a figure in the retirement calculator, it should be the basic pay for your retirement paygrade, not your total compensation while serving.

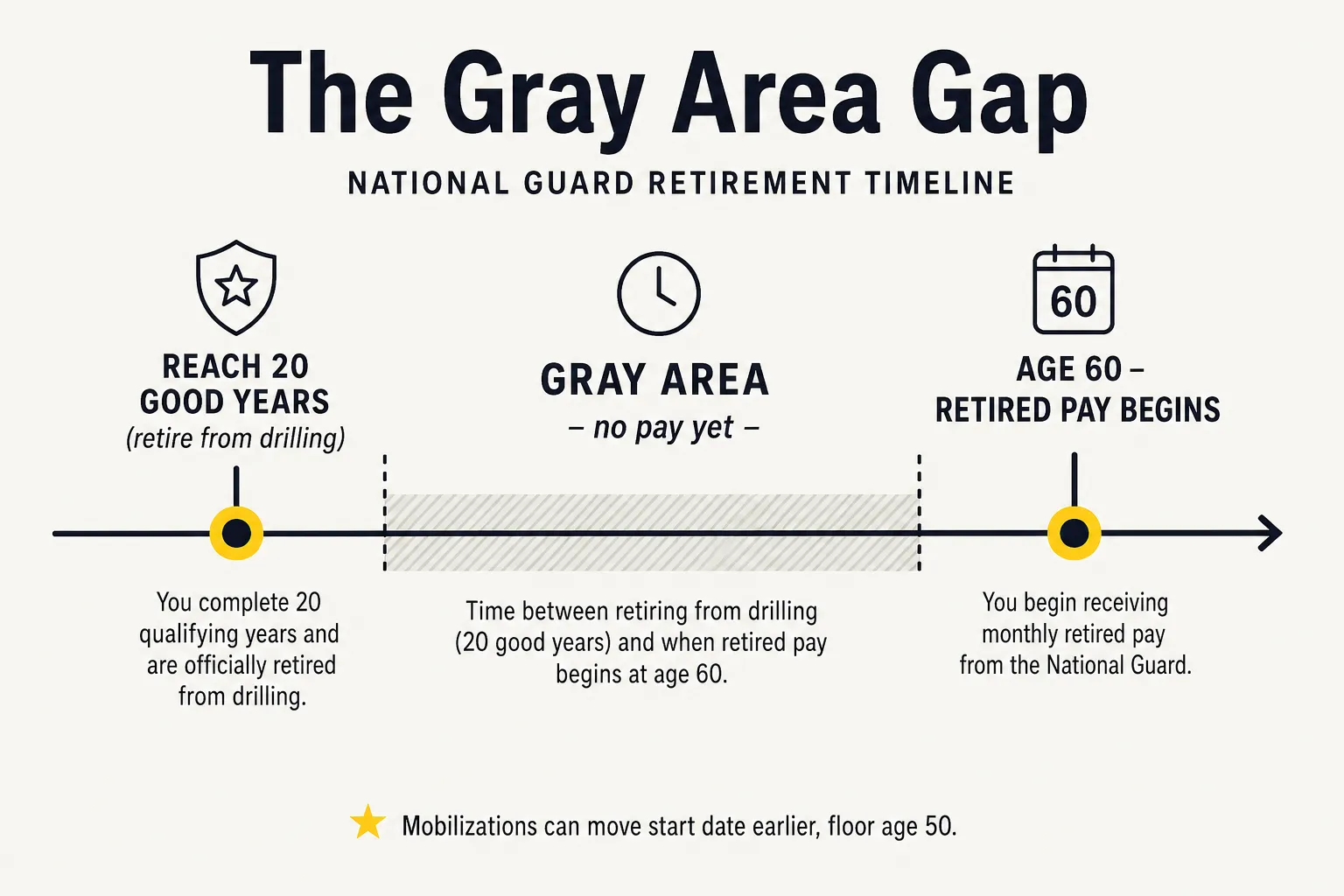

When the Money Starts: Age 60 and the Gray Area

This is the biggest structural difference from active-duty retirement, and it deserves its own section.

An active-duty retiree starts collecting the month they retire, often in their early 40s. A Guard or Reserve member who completes 20 good years and stops drilling enters what the community calls the gray area - they are a retiree who has vested in the pension but is not yet receiving it. Retired pay does not begin until age 60.

During that gray area the member keeps certain benefits, like access to a retirement ID and TRICARE Retired Reserve eligibility for purchase, but no monthly pension check arrives. For someone who finishes their 20 years at age 45, that is a 15-year wait before the first payment. Planning around that gap is essential, because the pension you earned is real but it is not income yet.

Reduced-age retirement for mobilizations

The age-60 rule has an important exception built for members who deployed. Under a provision first enacted in the 2008 National Defense Authorization Act, qualifying active-duty service after January 28, 2008 can pull your pay start date earlier than 60.

The mechanics:

- For every 90 cumulative days of qualifying active duty served in support of a contingency operation in a fiscal year, your retired-pay start age drops by 3 months.

- The reduction has a floor: it can never bring the start age below 50.

- A 2015 change lets the 90-day block be served across two consecutive fiscal years (for service beginning after September 30, 2014), rather than requiring all 90 days in a single fiscal year.

So a member with 360 cumulative qualifying days could move their start date a full year earlier - to age 59 - and heavy mobilization over a career can stack those reductions down toward the age-50 floor. The qualifying days must be the right kind of orders, so the specific authority under which you were activated matters. Check your orders and your branch's records to confirm which days count toward reduced-age retirement.

Guard and Reserve Under BRS vs Legacy High-3

The retirement-system split that applies to active duty applies to the Guard and Reserve too, with the points conversion layered on top.

| Feature | Legacy High-3 (Guard/Reserve) | BRS (Guard/Reserve) |

|---|---|---|

| Multiplier per equivalent year | 2.5% | 2.0% |

| Points-to-years divisor | 360 | 360 |

| Good years to vest | 20 | 20 |

| Pay begins | Age 60 (earlier with mobilization credit) | Age 60 (earlier with mobilization credit) |

| TSP automatic + matching | None | 1% automatic + up to 4% match |

| Continuation pay | None | Yes, mid-career bonus |

Two points are worth pulling out for Guard and Reserve members specifically.

First, the two systems use the same 360 divisor and the same 20-good-year requirement. BRS only changes the multiplier (2.0% instead of 2.5%) and adds the funded Thrift Savings Plan benefits. If you joined on or after January 1, 2018 you are automatically under BRS; if you were serving on or before December 31, 2017 you were grandfathered into legacy High-3 unless you opted in during the 2018 window. The detailed comparison of the two systems is in the BRS vs High-3 guide.

Second, BRS matters more for part-time service than people expect. Because most of a Reservist's pay is part-time, the funded TSP contributions and matching under BRS are a meaningful share of the total retirement value, and they vest and travel with you the same way they do for active-duty members. If you are a BRS Reservist, contributing at least 5% of your basic pay to capture the full match is the highest-return move available to you. Run your contribution rate through the TSP calculator to see how a part-time match compounds over a long career.

Common Mistakes to Avoid

A handful of errors come up repeatedly with Guard and Reserve retirements:

- Letting a year fall below 50 points. A year under 50 points is not a good year and does not count toward your 20. Track your point statement every year so a light year does not quietly cost you a good year.

- Confusing 360 and 365. The pension converts points using a 360 divisor, not 365. Using the wrong number understates your equivalent years and your pension.

- Assuming pay starts when you stop drilling. It starts at age 60 in most cases. Plan for the gray-area gap between finishing your 20 years and the first check.

- Overlooking reduced-age credit. If you mobilized after January 28, 2008, you may be entitled to start pay before 60. The credit is not always applied automatically, so verify your qualifying days.

- Using drill-era pay in the formula. The high-36 average is built from the pay tables near when your pay begins, usually around age 60, not your pay while you were drilling. Estimating with old pay understates the pension.

Frequently Asked Questions

How many points equal a year for Reserve retirement?

For the pension calculation, 360 points equal one equivalent year of service. You divide your total lifetime points by 360 to get the years figure, then multiply by your retirement multiplier (2.5% under legacy High-3 or 2.0% under BRS) and your high-36 base pay. Note this is different from the "good year" rule, which requires 50 points in a year for that year to count toward the 20 years needed to vest.

How many good years do I need for a Guard or Reserve pension?

You need 20 qualifying years, each with at least 50 retirement points. Fewer than 20 good years means no pension. A year with fewer than 50 points does not count toward the 20, although the points you did earn in that year still count in the dollar calculation once you vest.

When does Guard and Reserve retirement pay start?

Retired pay generally begins at age 60, not when you stop drilling. The period between completing your 20 years and turning 60 is called the gray area. Qualifying active-duty mobilizations after January 28, 2008 can move the start date earlier - 3 months for every 90 cumulative days of qualifying service - down to a floor of age 50.

How is National Guard retirement pay calculated?

Total your lifetime retirement points, divide by 360 to get equivalent years of service, then multiply by your retirement multiplier and your high-36 average basic pay. For example, 3,600 points is 10 equivalent years; under legacy High-3 that is 10 x 2.5% = 25% of your high-36 base pay. The high-36 average uses the pay tables in effect for the 36 months before your pay begins. Plug your own point total and paygrade into the retirement calculator for an exact figure.

Do active-duty points count toward Reserve retirement?

Yes. Time spent on active duty earns 1 point per day, and those points count toward both your point total for the pension and, if the year reaches 50 points, toward a good year. Prior active-duty service is one of the most valuable contributions to a Reserve point record, which is why a mobilization year can be worth around 365 points.

What is the difference between active-duty and Reserve retirement?

Active-duty retirement uses raw years of service and pays the month you retire, typically in your 40s. Reserve and Guard retirement converts points to equivalent years (points divided by 360), requires 20 good years to vest, and pays at age 60 unless mobilization credit moves it earlier. The multiplier and high-36 base pay work the same way in both systems.

Bottom Line

National Guard and Reserve retirement rewards the long game. You accumulate points across an entire career, protect a good year every single year by clearing 50 points, and bank the 20 good years that vest the pension. The payout then runs on the same formula as active-duty retirement with one swap - points divided by 360 stand in for years of service - and the check usually starts at age 60, earlier if your mobilizations earned reduced-age credit. The exact dollar figure depends on your point total, your retirement system, and the basic pay tables in effect when your pay begins, so confirm your point statement, verify any reduced-age credit, and run your real numbers through the military retirement calculator instead of any rule of thumb. If you are under BRS, see how the two systems compare in the BRS vs High-3 guide and capture the full TSP match while you serve.