Military Pension Calculator Walkthrough: High-3 Step by Step

Military pension calculator walkthrough of the High-3 formula: the high-36 average, the 2.5% per-year multiplier, COLA, and a worked example.

Before you trust any military pension calculator with your retirement number, it helps to know the formula it is running. If you came into the service between September 8, 1980 and December 31, 2017 and you did not opt into the Blended Retirement System, your pension runs on the High-3 formula. It is one of the more generous retirement plans still paying out, and the math behind it is not complicated once someone walks you through it slowly. The trouble is that most explanations either hand you a one-line formula with no context or bury it in regulation language. This guide does the opposite: it takes the High-3 calculation apart piece by piece, shows you a full worked example, and points out the spots where people most often miscalculate their own number.

The goal here is to leave you able to estimate your retired pay on a napkin and understand every term in the equation. When you want the precise figure with your actual pay-table numbers plugged in, run it through the retirement calculator - this military pension calculator does the arithmetic and the rounding for you, the same way a military retirement calculator should. But knowing how the machine works first means you can sanity-check any number a calculator, a retirement counselor, or a buddy at the unit gives you.

What "High-3" Actually Means

The name is a shorthand for the heart of the formula: your retirement is based on the average of your highest 36 months of basic pay. That is where "High-3" comes from - three years, expressed as 36 months. For almost everyone who serves a full career, those 36 months are the last three years before retirement, because basic pay generally rises over time through promotions and longevity raises.

A few things matter a great deal here and trip people up constantly.

It is basic pay only. Your High-3 average is built strictly from the basic pay line on your Leave and Earnings Statement. It does not include your Basic Allowance for Housing, your Basic Allowance for Subsistence, special or incentive pays, bonuses, or any allowance. Those are real money in your paycheck today, but they vanish the day you retire and they never enter the retirement formula. This is why a retired paycheck is so much smaller than the gross pay people are used to seeing - the allowances were never part of the pension to begin with.

It is the highest 36 months, not necessarily the final 36. For a normal career these are the same thing. But if you were reduced in grade, or you spent your last stretch at a paygrade and longevity step that paid less than an earlier period, the system uses whichever 36-month window was highest. The calculator looks for the best window, not just the last one.

Who Is Covered by High-3 (and Who Is Not)

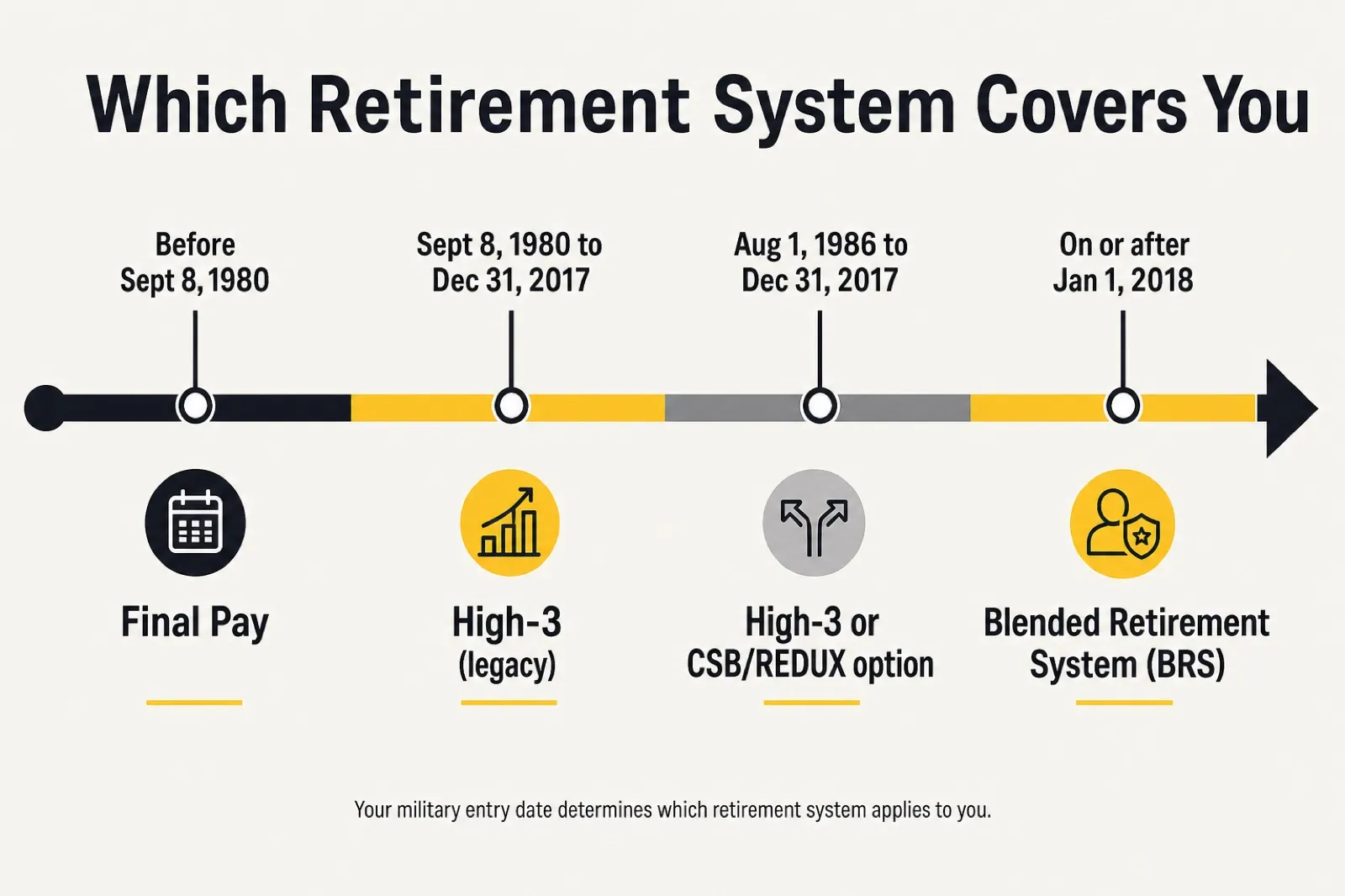

Before you calculate anything, confirm you are actually under High-3. There are several legacy military retirement systems, and they use different formulas. The dividing lines are based on your entry date - specifically your Date of Initial Entry into Military Service (DIEMS), sometimes called your DIEUS.

Here is the breakdown by entry date:

| Entry into service | Retirement system | Multiplier per year |

|---|---|---|

| Before Sept. 8, 1980 | Final Pay | 2.5% |

| Sept. 8, 1980 - July 31, 1986 | High-3 | 2.5% |

| Aug. 1, 1986 - Dec. 31, 2017 | High-3, or CSB/REDUX by election | 2.5% (REDUX reduces it) |

| On or after Jan. 1, 2018 | Blended Retirement System (BRS) | 2.0% |

A couple of clarifications on that table:

- Final Pay members (pre-1980 entry) base their pension on their final monthly basic pay rather than a three-year average. That cohort is almost entirely retired already.

- CSB/REDUX was an option, not an automatic plan, for those who entered between August 1, 1986 and December 31, 2017. Members in that window who took a $30,000 Career Status Bonus at 15 years of service switched to the REDUX formula, which uses a reduced multiplier before age 62 and a smaller cost-of-living adjustment. If you never took that bonus, you are on plain High-3.

- BRS is mandatory for anyone who first entered on or after January 1, 2018. It uses a lower 2.0% multiplier in exchange for government TSP matching. If you were already serving on December 31, 2017, you were grandfathered into the legacy system and could only move to BRS if you had fewer than 12 years of service and chose to opt in during the 2018 opt-in window. That window is long closed.

If any of that is fuzzy for your situation, the cleanest source of truth is your DIEMS on your service record. For the side-by-side dollar consequences of legacy retirement versus the newer system, our BRS vs. High-3 guide walks through the trade-off in detail.

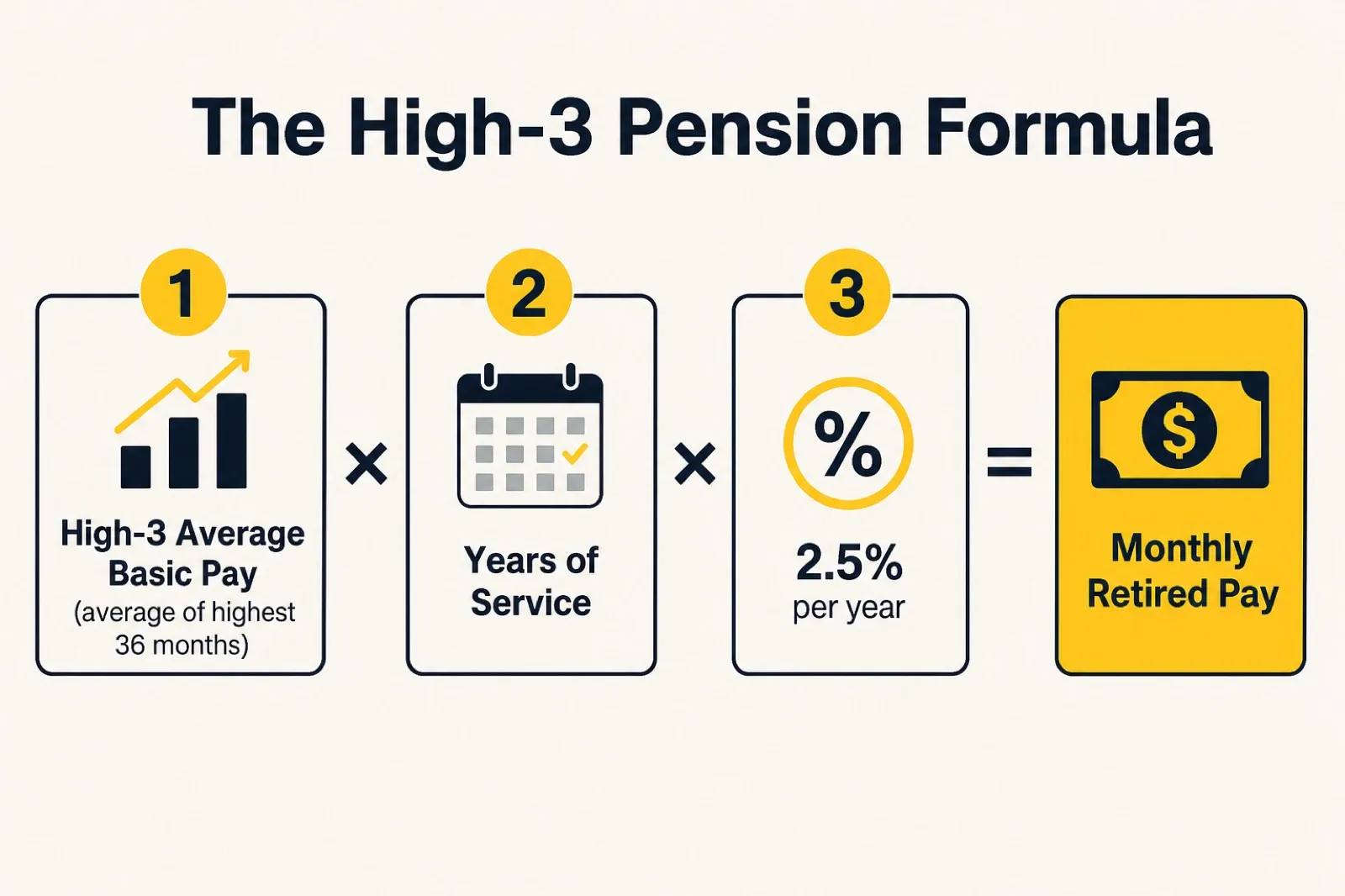

The High-3 Formula

Here is the whole thing in one line:

Monthly retired pay = High-3 average basic pay x (years of service x 2.5%)

That second factor - years of service times 2.5% - is your retirement multiplier. Every full year you serve adds 2.5 percentage points to it. Twenty years gets you to 50%. Thirty years gets you to 75%.

The 2.5% per year multiplier

This is the engine of the whole calculation. Under High-3, the multiplier is exactly 2.5% for each year of creditable service:

- 20 years -> 50%

- 24 years -> 60%

- 26 years -> 65%

- 30 years -> 75%

Partial years count too. Service credit is figured to the month, so each full month is worth one-twelfth of 2.5%, which is about 0.20833% per month. A career of 22 years and 6 months produces a multiplier of 22.5 x 2.5%, or 56.25%. You do not have to land on a clean year boundary to retire, and the formula does not round your service down to the nearest year - it credits the months you actually served.

Is there a cap on the multiplier?

For a regular 20-year active-duty retirement, there is no statutory ceiling that you are likely to hit through length of service alone. The 75% figure people quote is simply what 30 years produces (30 x 2.5%); serve longer and the multiplier keeps climbing past 75%. The 75% cap that does exist applies in the disability retirement context, where the multiplier used is the higher of your service multiplier or your assigned disability percentage, and that disability-based figure is capped at 75%. If a disability rating is part of your picture, that interacts with VA compensation in ways the disability calculator is built to handle - it is a separate analysis from a standard length-of-service retirement.

A Worked Example, Line by Line

Numbers make this concrete. Let us retire a hypothetical E-7 with 22 years of active service. The dollar figures below are illustrative - the exact basic pay numbers come from the current military pay tables, which is exactly what the retirement calculator and any good High-3 calculator pull in for you - but the method is the real method.

Step 1 - Find the highest 36 months of basic pay.

Our E-7 spent her final three years at the E-7 paygrade. Basic pay rises with longevity, so even within those three years the monthly figure stepped up. Suppose her basic pay over the highest 36 months looked roughly like this:

| Period | Monthly basic pay | Months |

|---|---|---|

| Earliest 12 months | $5,300 | 12 |

| Middle 12 months | $5,450 | 12 |

| Final 12 months | $5,600 | 12 |

Step 2 - Average those 36 months.

Add every month of basic pay and divide by 36. With the figures above:

(12 x $5,300) + (12 x $5,450) + (12 x $5,600) = $63,600 + $65,400 + $67,200 = $196,200

$196,200 / 36 = $5,450 High-3 average.

A shortcut: when the steps are evenly spaced like this, the average is just the middle year, $5,450. Real pay histories are messier, which is why a calculator sums the actual months rather than eyeballing it.

Step 3 - Build the multiplier.

22 years of service x 2.5% per year = 55%.

Step 4 - Multiply.

$5,450 x 55% = $2,997.50 per month, or about $35,970 a year before taxes, the Survivor Benefit Plan premium, or any other deductions.

That is the gross pension on day one. Now the part that makes High-3 worth so much over a lifetime.

What four more years is worth

Length of service is the lever you control, and 2.5% per year compounds into real money. Stick with the same $5,450 High-3 average and watch the multiplier do the work:

| Years served | Multiplier | Monthly pension | Annual pension |

|---|---|---|---|

| 20 | 50% | $2,725 | $32,700 |

| 22 | 55% | $2,997.50 | $35,970 |

| 24 | 60% | $3,270 | $39,240 |

| 26 | 65% | $3,542.50 | $42,510 |

Two caveats keep this honest. First, staying longer usually raises your High-3 average too, because basic pay keeps climbing with longevity and promotions - so the real-world gap between a 20-year and a 26-year retirement is wider than the table alone shows. Second, every figure here grows with COLA for the rest of your life, so multiply the annual difference by 30 or 40 years of payments to see the true value of staying in. That is the comparison worth running carefully before you make a stay-or-go decision.

When You Can Start Collecting

A standard active-duty High-3 retirement requires 20 years of creditable service, and you draw the pension immediately upon retirement regardless of your age. That is the headline difference between a military pension and a civilian 401(k) or even the federal civilian pension - a service member who enlisted at 18 and serves 20 years can begin collecting a COLA-protected check at 38. There is no waiting until age 59-and-a-half or 62. The pension starts the month after you retire.

Reserve and National Guard retirements work differently. They use a points-based system to credit service and, in most cases, do not begin paying until age 60 (earlier in some cases for qualifying active-duty mobilizations). The High-3 average and the 2.5%-per-point-equivalent math still underpin the calculation, but the timing and the way years are credited are not the same as the active-duty 20-year cliff described here. If you are a drilling reservist, treat the active-duty example above as the concept rather than your exact mechanics, and confirm the points conversion for your component.

Cost-of-Living Adjustments Keep It Honest

A pension that never grew would lose value to inflation every year. Military retired pay does not have that problem. It is adjusted annually by a cost-of-living adjustment - a COLA - tied to the Consumer Price Index.

The mechanics: the adjustment is effective December 1 each year (it shows up in the January 1 payment), and it is set by the percentage change in the average third-quarter CPI from one year to the next, as measured by the Department of Labor. Full High-3 retirees get the full CPI increase. This is one of the structural advantages of plain High-3 over the old REDUX option, where retirees took a COLA one percentage point below full CPI until age 62, then a one-time catch-up.

Over a 30- or 40-year retirement, that annual compounding matters more than most people expect. A pension that starts near $3,000 a month and rises with inflation is a very different asset from a fixed annuity at the same starting figure. When you are weighing whether to stay to 20, the COLA-protected, government-backed nature of this income stream is a big part of what you are actually earning.

Mistakes People Make Estimating Their Own High-3

A handful of errors come up again and again. Avoiding them gets you most of the way to an accurate number.

Counting allowances in the average

The single most common mistake. People take their full gross pay - basic pay plus BAH plus BAS plus any specialty pay - and run the formula on that. The result is wildly too high. Only basic pay counts. Pull the basic pay line off your LES and ignore everything else.

Assuming "High-3" means the last three years

Usually true, but not a law of nature. If your highest-paid 36 months were not your final 36 - because of a demotion, a break in service, or an unusual assignment history - the system uses the genuinely highest window. For a clean upward career this distinction never bites, but it is worth knowing it exists.

Forgetting that partial years count

Some people assume you must serve in whole-year increments or that months get rounded off. They do not. Service is credited by the month, so retiring at 21 years and 8 months gives you a real multiplier of roughly 54.17%, not a flat 50% or 52.5%.

Confusing High-3 with BRS

If you entered on or after January 1, 2018, you are on BRS and your multiplier is 2.0%, not 2.5%. Running BRS service through the High-3 formula overstates the pension by a quarter. The flip side is that BRS members also have years of government TSP matching that High-3 members never received, so the comparison is not as lopsided as the multiplier alone suggests. Our TSP guide for service members covers how those matching dollars stack up.

How This Fits the Rest of Your Retirement Picture

The High-3 pension is the foundation, but it is rarely the whole story. Most career retirees are looking at a combination of income streams, and each one is calculated differently:

- The pension itself, calculated as above and protected by COLA for life.

- Thrift Savings Plan balance. Even legacy High-3 members can contribute to the TSP; they simply did not get the automatic and matching contributions that BRS introduced. Whatever you put in, plus growth, is yours on top of the pension.

- VA disability compensation, if applicable, which is separate from retired pay and calculated on its own rating schedule. The interaction between a service pension and VA compensation (including concurrent receipt rules) is its own subject - start with the disability calculator.

- Survivor Benefit Plan, an elected annuity for a spouse or child that is paid for by a premium deducted from your retired pay.

The point is that your retired pay line is one input into a larger plan, not the entire plan. Get the High-3 number right first, because it anchors everything else.

Frequently Asked Questions

How is High-3 retirement calculated?

Take the average of your highest 36 months of basic pay - your High-3 average - and multiply it by your retirement multiplier, which is your years of service times 2.5%. That product is your gross monthly retired pay. Only basic pay counts toward the average; allowances and special pays are excluded.

What is the High-3 retirement formula?

The formula is one line: monthly retired pay = High-3 average basic pay x (years of service x 2.5%). Twenty years produces a 50% multiplier, and each additional year adds 2.5 percentage points, with partial years credited to the month.

What is the average military pension after 20 years?

A 20-year retirement locks in a 50% multiplier, so the pension is half of your High-3 average basic pay. Using the $5,450 average from the worked example above, that comes to about $2,725 a month, or roughly $32,700 a year before deductions. Your actual figure depends on your paygrade and the current pay tables, and COLA raises it every year you draw it.

How much is military retirement pay?

It is your High-3 average basic pay multiplied by your service multiplier. For a 20-year career that is 50% of the average, climbing to 75% at 30 years and beyond. Run your real paygrade and years through the retirement calculator to see your exact military pension amount.

BRS vs High-3?

High-3 uses a 2.5% per-year multiplier and no government TSP matching, while the Blended Retirement System (BRS) uses a lower 2.0% multiplier but adds automatic and matching TSP contributions. Anyone who first entered service on or after January 1, 2018 is on BRS; most who entered earlier stayed on High-3. Our BRS vs. High-3 guide walks through the dollar trade-off.

What happens when you retire from the military after 20 years?

Retiring from the military after 20 years of active service entitles you to an immediate, COLA-protected pension regardless of your age - a service member who enlisted at 18 can begin collecting at 38. You also keep any Thrift Savings Plan balance, may elect the Survivor Benefit Plan, and can claim VA disability compensation separately if you have a rating.

Run Your Real Numbers in the Military Pension Calculator

You now have everything you need to estimate a High-3 pension by hand: confirm you are under High-3 by your entry date, build the average of your highest 36 months of basic pay, multiply your years of service by 2.5% to get the multiplier, and multiply the two together. Add COLA on top for every year you draw the pension.

When you want the exact military pension amount rather than a napkin estimate, the retirement calculator does it with the current military retirement pay chart values, handles partial-year service to the month, and lets you test different retirement dates side by side. Try it with a 20-year exit and a 24-year exit and watch how much those four extra years - and the four extra increments of 2.5% - change the lifetime value. That comparison is one of the most useful things you can do before you decide when to hang it up.