VA Combined Rating Calculator: How VA Disability Math Works

VA combined rating calculator guide: how the VA combines multiple disability ratings, why 50 plus 30 is not 80, the bilateral factor, and dependent pay.

If you have more than one service-connected condition, the single most confusing part of your VA disability award is usually the math, which is exactly why so many veterans reach for a VA combined rating calculator instead of trusting their own arithmetic. You read your decision letter, you see a 50 percent rating for one issue and a 30 percent rating for another, and you naturally expect an 80 percent combined rating. Then the letter says 70 percent, or sometimes 60, and nothing about it looks like arithmetic you have seen before. You are not misreading it. The VA does not add your ratings together, and the reason it does not is worth understanding, because it directly affects the check that lands in your account every month.

This guide walks through exactly how the VA arrives at a single combined rating from several individual ones, why the order of your conditions matters, how rounding can move you up or down a full bracket, and how dependents change the dollar amount once the rating is set. The percentages and rules here come straight from VA regulation, but the actual dollar figures change every December with the annual cost-of-living adjustment, so the cleanest way to see your own number is to run your conditions through the VA disability calculator, which works as a VA combined rating calculator and does the table lookups for you.

Why VA Ratings Are Not Added Together

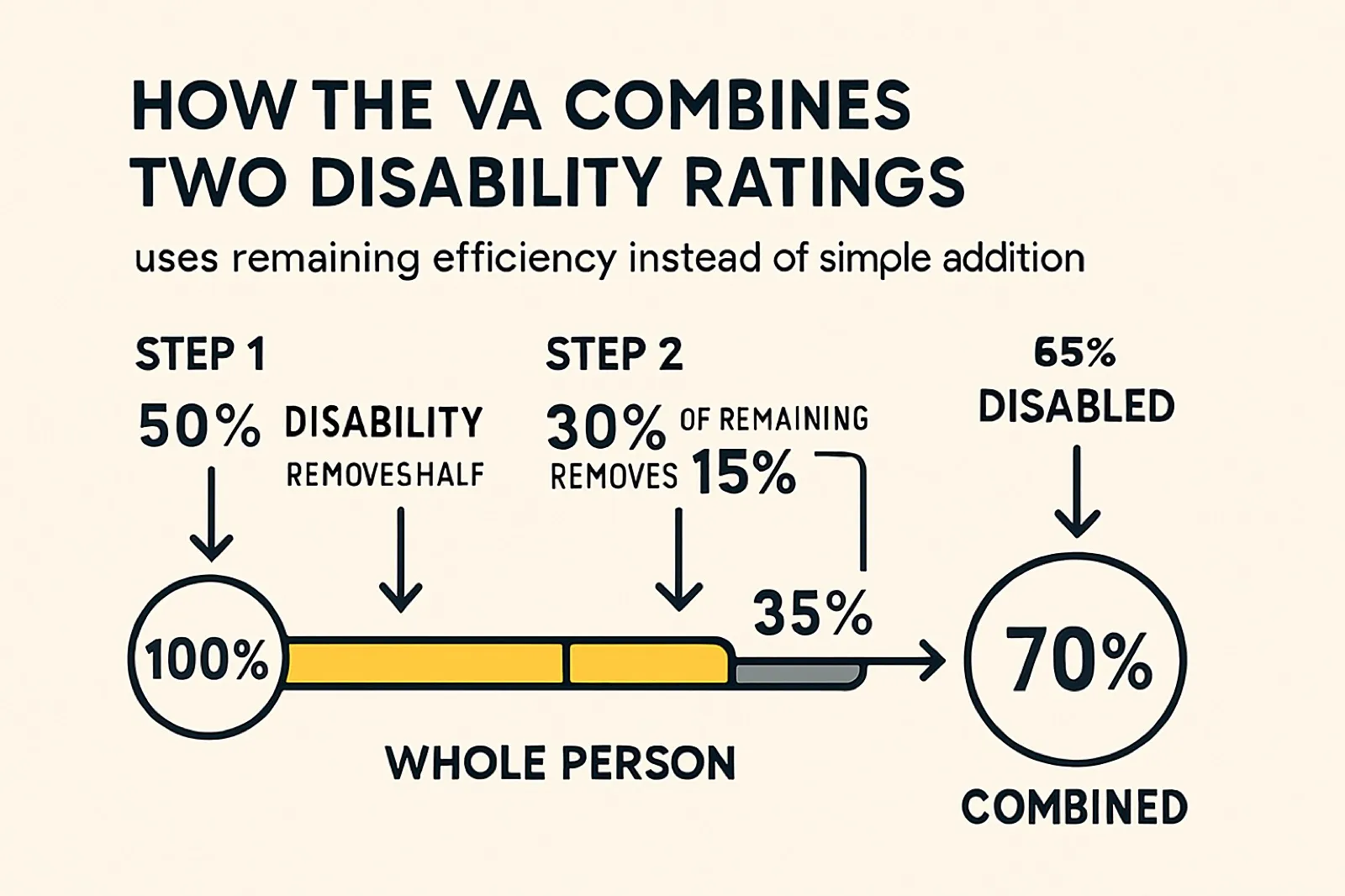

The core idea is something the VA calls the whole person concept. A person starts at 100 percent efficiency, meaning fully able-bodied. Each disability does not subtract a flat percentage from a running total. Instead, it takes a bite out of whatever efficiency is left after the disabilities ahead of it have already taken theirs. This is why you can never exceed 100 percent no matter how many conditions you have, and it is why two ratings that look like they should sum to 80 often land lower.

Walk through it slowly with a 50 percent and a 30 percent rating. Start at 100 percent efficiency. The 50 percent disability is applied first and removes half, leaving you 50 percent efficient. Now the 30 percent disability is applied, but it is not applied to the original whole person. It is applied to the 50 percent that remains, so it removes 30 percent of 50, which is 15. Subtract that 15 from the 50 you had left and you are at 35 percent efficiency, meaning 65 percent disabled. The VA rounds that to the nearest 10, giving a combined 70 percent rating, not the 80 you might have guessed.

That single example contains the whole logic. Each additional condition matters less to your combined number than the one before it, because there is less remaining efficiency for it to act on. A veteran with a 10 percent condition stacked on top of an already high rating may see the combined figure barely move at all. This is not the VA shortchanging you. It is the mathematical consequence of measuring against a person who is, on paper, already partly disabled.

The official combined ratings table

You do not actually have to do this multiplication by hand. The VA publishes a combined ratings table in its regulations, specifically 38 CFR 4.25, and that VA combined rating table is the authority of record. The math above is simply what the table encodes, and it is the same logic any VA math calculator or VA disability rating calculator runs under the hood. To use it, you find your higher rating down the left column and your lower rating across the top row, and the cell where they meet is the combined value before rounding. For the 50 and 30 example, the intersection reads 65, which is exactly what the efficiency calculation produced.

When you have more than two conditions, you do not look them all up at once. You combine two at a time, always working from the highest rating down to the lowest, and you carry the unrounded result forward into the next lookup. Rounding happens only once, at the very end.

How a VA Combined Rating Calculator Handles Three or More Ratings

The order is not optional, and getting it wrong is one of the most common mistakes veterans make when they try to check the VA's work. The rule is always highest to lowest. Sort your individual ratings in descending order, combine the two largest, then combine that running total with the next largest, and keep going until every condition is folded in.

Here is the worked example the VA itself uses, with conditions rated 60 percent, 40 percent, and 20 percent. Start with the two highest, 60 and 40. The table puts their intersection at 76. You do not round yet. You take that 76 back to the left column and combine it with the remaining 20 percent condition. The table puts that intersection at 81. Now, and only now, you round to the nearest 10. Eighty-one rounds down to a final combined rating of 80 percent.

The rounding rule is worth stating plainly because it can feel arbitrary in the moment. A combined value ending in 1 through 4 rounds down, and a value ending in 5 through 9 rounds up. An unrounded 84 becomes 80, while an unrounded 85 becomes 90. That single point can be the difference between two compensation brackets that are hundreds of dollars apart each month, which is why veterans sitting near a boundary pay such close attention to whether one more secondary condition might tip them over the line.

Why the order changes nothing about the final number, but everything about checking it

A reasonable question is whether sorting highest to lowest actually changes the result, since multiplication is commutative. The final combined value is in fact the same regardless of order, because you are multiplying the same set of remaining-efficiency fractions together. The reason the VA mandates the highest-to-lowest sequence is consistency and the integrity of the rounding step, since the table only stores whole numbers and rounding intermediate values would introduce drift. So if you are reproducing your own rating to confirm it, follow the order exactly, do not round until the end, and you will match the VA. If your hand math disagrees with your decision letter, the usual culprit is an intermediate rounding you should not have done, or a condition you forgot to include.

If you would rather not touch the table at all, the VA disability calculator applies the same 38 CFR 4.25 logic, sorts your conditions for you, and shows the combined value before and after rounding so you can see exactly where your number came from. That makes it a practical VA disability calculator for multiple disabilities, since it folds in every condition in the correct order automatically.

The Bilateral Factor: An Extra Bump Most Veterans Miss

There is one wrinkle that can quietly raise your combined rating, and a lot of veterans never hear about it until someone points it out. It is called the VA bilateral factor, and it applies when you have disabilities affecting both arms, both legs, or paired muscle groups acting on both sides of the body. The logic is that losing function on both sides of a paired limb set is more disabling than the sum of the two sides considered separately, because it compromises your ability to compensate by leaning on the good side.

When the bilateral factor applies, the VA first combines the ratings for the affected paired extremities, then adds an extra 10 percent of that combined value before folding the result into your other, non-bilateral conditions. A right-knee and a left-knee condition, for instance, would be combined with each other, given the 10 percent bilateral bump, and only then combined with, say, a back condition or tinnitus. Because the bilateral factor is applied before the rest of your conditions, the order of operations gets more involved, and this is precisely the kind of case where running the numbers through a calculator beats doing it on paper. The takeaway for now is simply to know the factor exists, since it can be the reason your combined rating is a notch higher than a naive table lookup would suggest.

From Rating to Dollars: How Dependents Change Your Check

Once your combined rating is locked in, it points to a monthly compensation amount, and this is where your family situation enters the picture. The VA pays more to veterans who support dependents, but only above a certain rating threshold, and the bump is structured very specifically.

The first thing to understand is the floor. If your combined rating is 10 percent or 20 percent, dependents do not increase your payment at all. A veteran rated 20 percent receives the same monthly amount whether single or supporting a spouse and three children. The dependent add-ons only begin at a combined rating of 30 percent and scale up from there. This catches people off guard, so it is worth saying directly: claiming your dependents in the VA system does nothing for your check until you cross into the 30 percent bracket.

Above that threshold, the rate tables split into columns by dependent status, with the basic single-veteran rate in one column and progressively higher amounts as you add a spouse, then a first child, then additional children or dependent parents. The dollar gap between the single rate and the with-family rate grows as your rating climbs, so dependents are worth the most to veterans at the higher ratings.

What the 2026 numbers actually look like

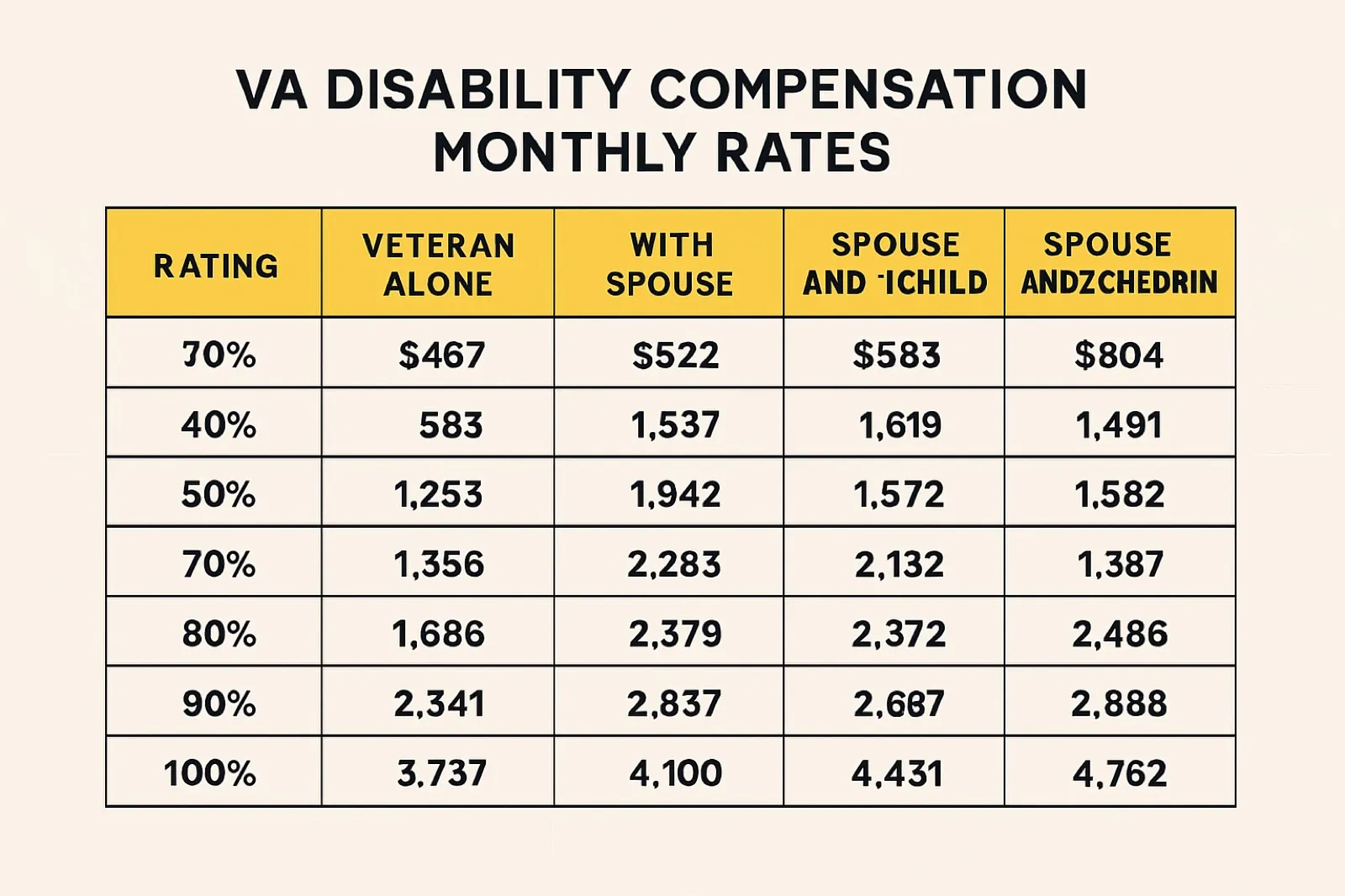

The current figures took effect on December 1, 2025, after the latest cost-of-living adjustment, and they hold through the rest of the rate year. A veteran with no dependents receives $180.42 per month at 10 percent and $356.66 at 20 percent, with no dependent variation at either level. At 30 percent the single rate is $552.47, and a veteran with a spouse and no other dependents receives $617.47, so the spouse alone is worth roughly $65 a month at that rating.

At the top of the scale the spread widens sharply. A single veteran at 100 percent receives $3,938.58 per month, while the same veteran with a spouse and no children receives $4,158.17. Each additional dependent child under 18 adds $109.11 per month at the 100 percent level, and there are further add-ons if your spouse qualifies for Aid and Attendance. These exact dollar amounts shift every December, so treat the figures here as a 2026 snapshot rather than a permanent fixture, and confirm your own situation against the live tables or the calculator.

Children, school, and the cutoff ages

The dependent rules are not just about how many children you have but about their status. A child generally counts as a dependent for VA compensation until age 18, with the allowance continuing to age 23 if the child is enrolled full time in an approved school, and indefinitely for a child who became permanently incapable of self-support before turning 18. Keeping your dependents current in the VA system matters, because the agency pays based on what it has on file. If a child ages out and you do not update the record, the VA can later claw back the overpayment, and if you add a child and forget to file, you simply leave money on the table. Make sure your dependents are accurate in DEERS and reported to the VA, since the two systems serve different purposes and updating one does not automatically update the other.

Putting It All Together with a Full Example

Take a veteran with four service-connected conditions: a back condition at 40 percent, tinnitus at 10 percent, a right knee at 20 percent, and a left knee at 20 percent. The two knee conditions are bilateral, so they get handled first. Combine 20 and 20 to get 36 on the table, then apply the 10 percent bilateral factor, which adds roughly 4 to reach about 40 for the paired knees as a unit.

Now combine everything highest to lowest. The back condition at 40 and the bilateral knee value around 40 combine to roughly 64. Carry that forward and combine with the 10 percent tinnitus, which moves it to about 68. Round to the nearest 10 and you land at a 70 percent combined rating. Notice that a straight addition of 40 plus 20 plus 20 plus 10 would have suggested 90 percent, which is 20 points higher than reality. That gap, multiplied across a career of compensation payments, is exactly why understanding the method matters.

With a 70 percent rating set, the veteran then reads across the rate table to the column matching their dependent status. A single veteran and one supporting a spouse and two children are looking at meaningfully different monthly amounts, even though their rating is identical, and that difference is the entire point of keeping dependents reported and current.

Common Mistakes and How to Avoid Them

The errors that trip people up are predictable once you know the method. The most frequent is adding ratings instead of combining them, which always overstates the result. Close behind is rounding intermediate values, which produces a number that is off by a few points and never matches the decision letter. A third is combining conditions in the wrong order, or forgetting a low condition entirely because it seemed too small to matter. And a surprising number of veterans simply never claim dependents they are entitled to, leaving the spouse and child add-ons unpaid for years.

A few habits prevent all of these. Always sort highest to lowest, combine two at a time, round only at the very end, handle bilateral pairs before anything else, and keep your dependent records accurate. If you would rather skip the bookkeeping, enter your individual ratings and your family situation into the VA disability calculator and let it produce the combined rating and the monthly figure together.

How This Fits with Your Other Benefits

A combined disability rating does more than set a monthly payment. It can unlock or interact with several other benefits, and it is worth seeing the whole board. A high rating affects eligibility for the VA Disability Compensation tax treatment, since these payments are not counted as taxable income, and that tax-free status meaningfully changes how the amount compares to ordinary wages. Veterans pursuing a home purchase should also note that a service-connected disability rating can waive the VA loan funding fee entirely, which our VA loan guide walks through in detail, and which is one of the largest single-dollar benefits a disability rating can carry. And if your service included time in a designated combat zone, the pay you earned there interacts with separate rules covered in the combat pay breakdown.

The thread running through all of it is that your combined rating is the hinge. Get the rating math right, keep your dependents current, and the downstream dollar figures follow predictably. When you want the exact number for your own conditions and family, the VA disability calculator is the fastest way to see it without wrestling the table by hand.

Frequently Asked Questions

How is the VA combined rating calculated? The VA combines ratings two at a time using the combined ratings table in 38 CFR 4.25, always working from highest to lowest. Each rating is applied to the efficiency remaining after the ratings ahead of it, not added on top, and the result is rounded to the nearest 10 only at the very end.

How does VA math work? VA math uses the whole person concept. You start at 100 percent efficiency, and each disability removes a share of whatever efficiency is left rather than a flat slice of the original whole. That is why a 50 percent and a 30 percent rating combine to 65 before rounding instead of 80.

What is the VA bilateral factor? The VA bilateral factor is an extra bump for disabilities affecting both arms, both legs, or paired muscle groups on both sides of the body. The VA first combines the paired extremities, then adds 10 percent of that combined value, and only then folds the result in with your other conditions.

How do you calculate disability percentage for multiple conditions? Sort your ratings highest to lowest, combine the two largest on the 38 CFR 4.25 table, carry the unrounded result forward, and combine it with the next condition. Repeat until every condition is included, then round once to the nearest 10. A VA combined rating calculator does these steps automatically.

What is the VA overall combined rating? The overall combined rating is the single percentage the VA assigns after combining all of your individual service-connected ratings. It is the figure that determines your monthly compensation amount and any dependent add-ons, not a simple sum of your separate ratings.

What are VA disability percentages for conditions? Each service-connected condition is rated on its own in 10 percent increments, from 0 up to 100 percent, based on the severity criteria in the VA rating schedule. Those individual percentages are then combined, never added, to produce your overall rating.

Do dependents increase my payment at 20 percent? No. Dependent add-ons begin at a combined rating of 30 percent. At 10 and 20 percent, the payment is the same regardless of family size.

Where do the dollar amounts come from? From the VA rate tables that took effect December 1, 2025. They adjust every December with the cost-of-living adjustment, so always confirm against the current tables or the calculator.