VA Home Loan Guide 2026: Eligibility, Rates & Requirements

A 2026 VA home loan guide covering eligibility and service requirements, no down payment and no PMI, the funding fee rates, loan limits, and the COE process.

The VA home loan is the single most valuable benefit most service members will ever earn, and a lot of the people entitled to it never use it. It lets a qualified veteran, active-duty member, or surviving spouse buy a primary home with no down payment, no private mortgage insurance, and a government guaranty that gets you a better interest rate than you would qualify for on your own. It is not a loan from the VA itself. It is a loan from an ordinary bank or mortgage lender that the Department of Veterans Affairs partially backs, which is what removes the down payment and the monthly insurance that everyone else has to carry.

This guide covers who qualifies in 2026, the exact funding fee rates, how loan limits work now that full-entitlement borrowers have none, and the paperwork that actually gets you to closing. The one number that moves the most is the interest rate, and that changes daily, so rather than quote a rate that is stale by the time you read it, estimate your real monthly payment and funding fee in the VA loan calculator as you go. It uses the current 2026 fee schedule.

The Short Version

For most eligible buyers, the VA loan beats a conventional or FHA loan, and it is not close. Here is why, before we get into the detail.

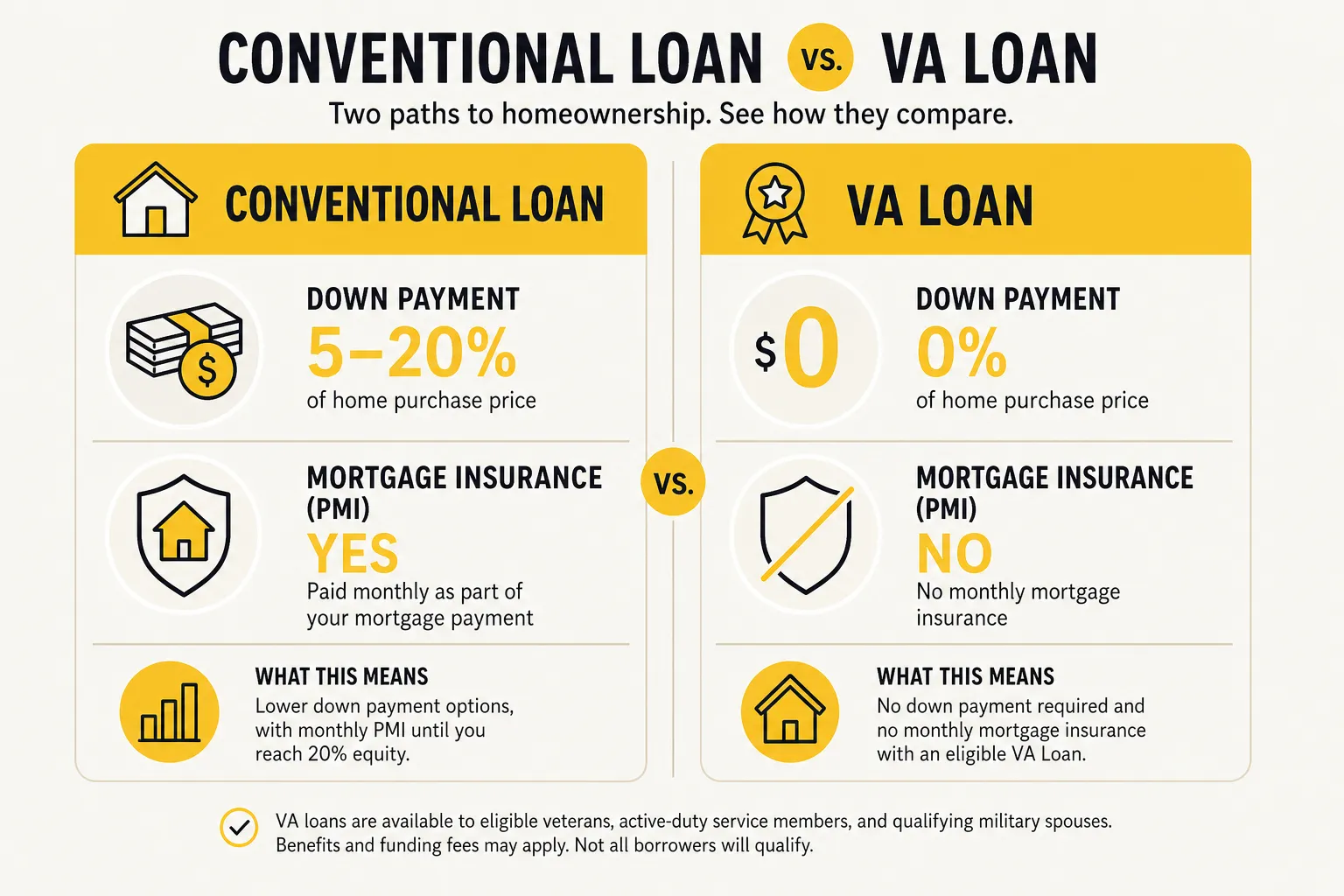

- No down payment. A qualified borrower with full entitlement can finance 100 percent of the purchase price. No other mainstream loan does this without strings.

- No private mortgage insurance. Conventional loans charge PMI when you put down less than 20 percent. FHA loans charge mortgage insurance for the life of the loan in most cases. VA loans charge neither, ever. The VA guaranty takes the place of that insurance.

- A one-time funding fee instead. The trade-off is a single funding fee paid at closing, which you can roll into the loan. Many disabled veterans pay nothing at all.

- Reusable for life. This is not a one-time benefit. You can use it again and again, and you can have more than one VA loan at the same time in some cases.

The catch is that the VA does not hand you a house. You still need a lender willing to make the loan, satisfactory credit, and enough income to cover the payment. The benefit removes the biggest barriers; it does not remove all of them.

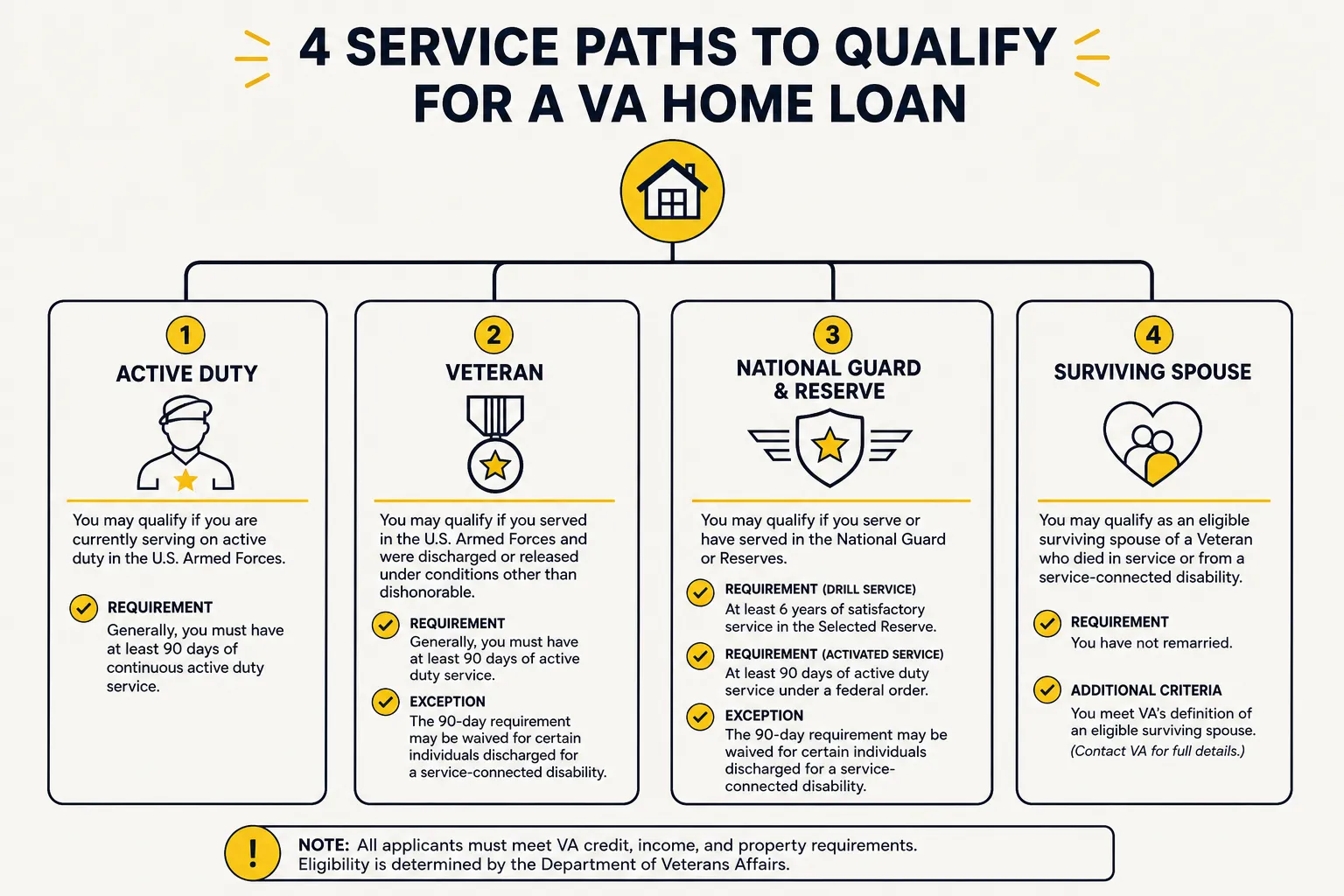

Who Qualifies in 2026

Eligibility comes down to your service history and your current duty status. There are four main paths, and the exact requirement depends on when you served. These are the federal rules in effect for 2026.

Active-duty service members

If you are currently serving on active duty, you generally qualify once you have served at least 90 continuous days. You do not have to wait until you separate or retire. Active-duty members are one of the largest groups using the benefit, often for a home near a duty station.

Veterans

For veterans, the minimum depends on your service era. For anyone who served during the post-Gulf War period (August 2, 1990 to the present), the requirement is at least 24 continuous months of active duty, or the full period of at least 90 days for which you were called or ordered to active duty. Members who served between September 8, 1980 and August 1, 1990 generally face the same 24 continuous months standard. Earlier service eras have their own, often shorter, minimums. A discharge under conditions other than dishonorable is required across the board.

National Guard and Reserve

Guard and Reserve members have their own track. You generally qualify with 6 creditable years in the Selected Reserve or National Guard if you are still serving or were discharged honorably. You can also qualify with at least 90 days of non-training active-duty service. The 6-year path is what lets a drilling reservist who never deployed still earn the benefit.

Surviving spouses

A surviving spouse may be eligible if they receive VA Dependency and Indemnity Compensation, or if they are the spouse of a service member who is missing in action or a prisoner of war. This path exists so that a military family does not lose the home benefit when they lose the member. If you receive VA disability compensation or DIC, that status also tends to make you exempt from the funding fee, which is covered below.

The cleanest way to confirm which path applies to you is to request your Certificate of Eligibility, which we walk through near the end of this guide. If you are unsure whether your service counts, the COE process answers it definitively.

What Makes the VA Loan Different

The benefit is built on one mechanism: the VA guarantees a portion of the loan to the lender. That single feature is what produces every advantage borrowers care about.

No down payment

Because the government backs roughly a quarter of the loan, the lender is protected against loss even with nothing down. So a borrower with full entitlement can finance the entire purchase price. On a $350,000 home, that is $70,000 you do not have to produce that a 20-percent conventional buyer would. The money you would have spent on a down payment can stay in savings or go toward closing costs and moving.

No private mortgage insurance

This is the quiet giant of the VA loan. On a conventional loan with less than 20 percent down, you pay PMI every month, often $100 to $300 or more, until you build enough equity. FHA loans carry mortgage insurance that, in most cases, never goes away for the life of the loan. The VA loan has none of this. The funding fee replaces it, and the funding fee is paid once, not every month for years. Over a 30-year loan this difference alone can be worth tens of thousands of dollars.

Competitive interest rates and easier qualifying

Because the loan is government-backed, lenders take on less risk, and that usually shows up as a lower interest rate than a comparable conventional loan and more forgiving credit standards. The VA itself does not set a minimum credit score, though individual lenders do. You still need to demonstrate stable income and a reasonable debt load. The VA uses a residual income test, which looks at the cash you have left after major monthly obligations, rather than relying on a debt-to-income ratio alone.

A reusable, lifelong benefit

Your entitlement restores after you sell a home and pay off the VA loan, so you can use the benefit again on your next home. With enough entitlement you can even carry two VA loans at once, which matters for service members who buy at one duty station and then PCS to another. This is a benefit you earned, not a one-shot coupon.

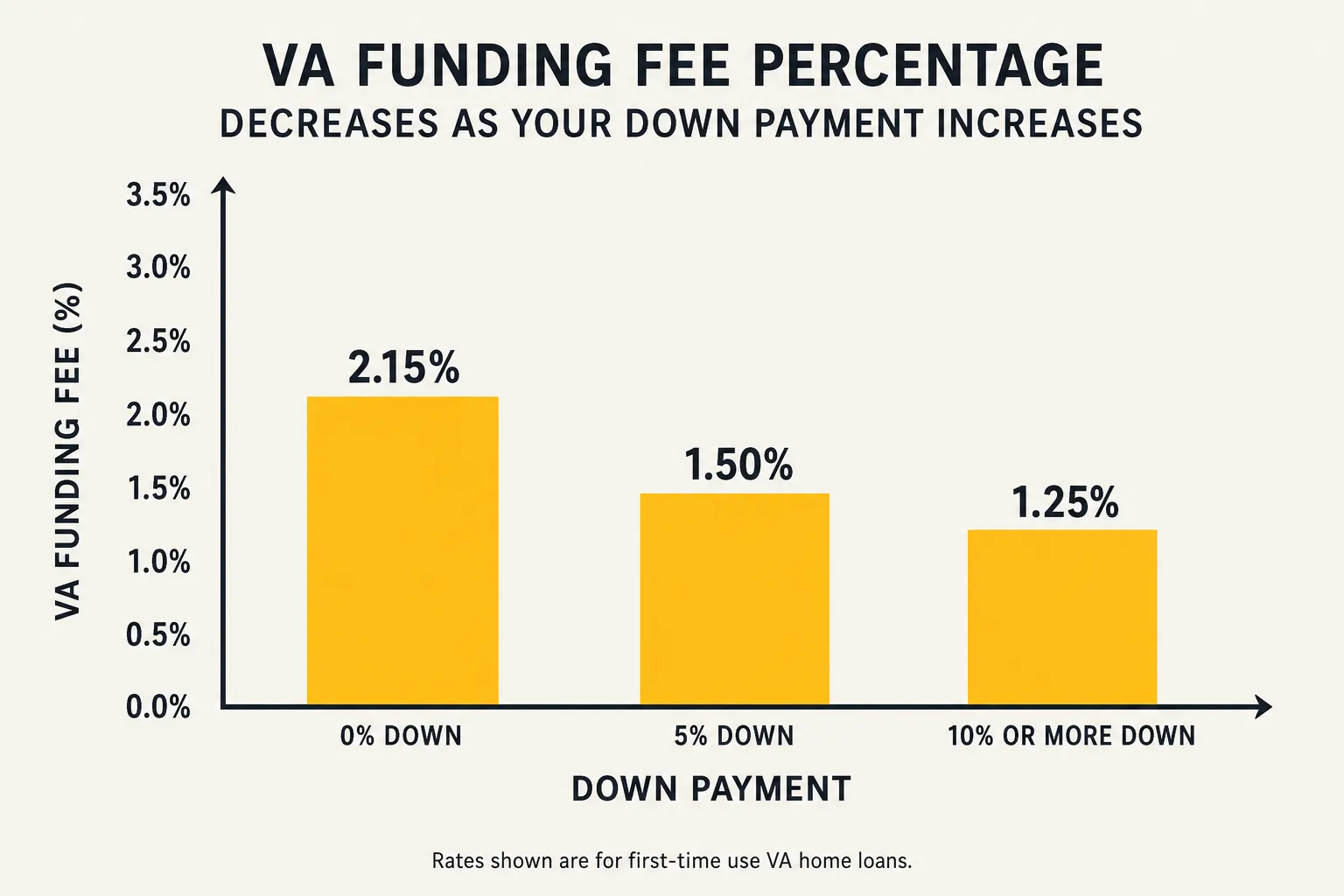

The VA Funding Fee in 2026

The funding fee is the one cost that is unique to VA loans, and it is the trade-off for skipping the down payment and the monthly insurance. It is a one-time charge that goes directly to the VA, not the lender, and it funds the program so it costs taxpayers nothing. You can pay it at closing or roll it into the loan amount.

The rate depends on three things: whether this is your first time using a VA loan, how much you put down, and the loan type. These are the official 2026 rates for purchase and construction loans.

| Down payment | First use | Subsequent use |

|---|---|---|

| Less than 5% | 2.15% | 3.3% |

| 5% to less than 10% | 1.5% | 1.5% |

| 10% or more | 1.25% | 1.25% |

Two things jump out. First, a down payment cuts the fee sharply, and once you reach 5 percent down, first-time and repeat users pay the same rate. Second, the most expensive scenario is a repeat user putting nothing down, at 3.3 percent. On a $350,000 zero-down subsequent-use loan that is $11,550 added to the balance. That is exactly the kind of number worth running before you decide whether to make a small down payment, which you can do in the VA loan calculator.

Refinances follow their own schedule. A cash-out refinance is 2.15 percent on first use and 3.3 percent after. The Interest Rate Reduction Refinance Loan, or IRRRL, the streamlined refinance used to lower your rate, carries a flat 0.5 percent fee.

Who is exempt from the funding fee

A large share of borrowers pay no funding fee at all. You are exempt if you are receiving VA compensation for a service-connected disability, or are eligible for it but receiving active-duty or retirement pay instead. Surviving spouses receiving Dependency and Indemnity Compensation are exempt, as are Purple Heart recipients on active duty who provide evidence on or before closing, and members with a proposed or memorandum disability rating before the loan closes. If you fall into any of these groups, set the funding fee to zero when you estimate your costs. New for 2026, the funding fee is also tax-deductible for those who do pay it, which softens the cost further. For the full breakdown of how the fee works, refunds, and the new deduction, see the VA funding fee 2026 guide.

VA Loan Limits and Entitlement

This is the area that changed most in recent years and where old advice leads people astray.

Full entitlement means no loan limit

If you have full entitlement, there is no VA loan limit. The VA will back your loan regardless of the purchase price, as long as you can afford the payment and the appraisal supports the price. The old county loan limits no longer cap what a full-entitlement borrower can buy with zero down. The practical ceiling is the appraised value or the purchase price, whichever is lower, plus whatever a lender is willing to approve based on your income.

You have full entitlement if you have never used your VA loan benefit, or if you used it before but have since sold the home and repaid the loan in full, restoring your entitlement.

Reduced entitlement and the county limits

If you currently have an active VA loan, or you previously defaulted on one, your entitlement is reduced. In that situation the county loan limits come back into play to calculate how much the VA can guarantee on a second, simultaneous loan, which may mean you need a down payment to cover the gap. The VA ties these limits to the Federal Housing Finance Agency conforming loan limit. For 2026 the baseline one-unit conforming limit is $832,750 in most of the country, and $1,249,125 in designated high-cost areas such as Alaska, Hawaii, Guam, and the U.S. Virgin Islands. These figures matter mainly to reduced-entitlement borrowers and to anyone carrying two VA loans at once.

The takeaway: if this is your first VA loan, ignore the loan-limit conversation entirely. It does not apply to you. It only constrains repeat borrowers using partial entitlement.

Getting Your Certificate of Eligibility

Before a lender will close a VA loan, they need proof you qualify. That proof is the Certificate of Eligibility, or COE. It confirms your service history and entitlement to the lender. It is the first real step, and it is usually fast.

There are three common ways to get one:

- Through your lender. Most VA-approved lenders can pull your COE electronically in minutes through the VA's online system. This is the easiest route and the one most buyers use without even realizing it happened.

- Online yourself. You can request it directly through your VA.gov account if you want it in hand before you shop.

- By mail. You can submit VA Form 26-1880 and supporting documents if the electronic system cannot verify your service, which sometimes happens for Guard and Reserve records.

You will want your discharge or separation paperwork available. For veterans that is your DD-214; active-duty members need a statement of service signed by a commander or personnel officer; Guard and Reserve members may need points statements or NGB Form 22. The COE itself does not approve you for a loan or a specific amount. It only establishes that you are entitled to the benefit. The loan approval, the rate, and the amount all come from the lender after they review your credit, income, and the property.

How the Process Works, Step by Step

The VA loan adds a couple of steps to a normal home purchase but is otherwise familiar.

- Confirm eligibility and get your COE. Establish that you qualify before you fall in love with a house.

- Get pre-approved by a VA-approved lender. Not every lender does VA loans well; pick one with real volume. Pre-approval tells you your real budget and strengthens your offer.

- Shop and make an offer. Make sure your purchase contract allows for a VA appraisal and includes the VA escape clause, which lets you back out without penalty if the appraisal comes in below the contract price.

- VA appraisal and inspection. The VA orders an appraisal that establishes value and checks that the home meets minimum property requirements for safety and livability. This protects you from buying a home with serious defects. A VA appraisal is not the same as a home inspection, and you should still get a private inspection.

- Underwriting and closing. The lender verifies everything, you review your closing costs including the funding fee, and you sign. Then you get the keys.

The single most useful thing you can do at the start is estimate your full monthly payment, including taxes and insurance, plus the funding fee, in the VA loan calculator, so you walk into pre-approval already knowing your numbers.

Common Mistakes to Avoid

A handful of errors trip up VA borrowers repeatedly:

- Assuming you do not qualify. Plenty of Guard and Reserve members and short-term veterans assume the benefit is only for 20-year retirees. The 6-year reserve path and the 90-day active-duty path catch far more people than most realize.

- Making a down payment without doing the math. A down payment lowers your funding fee and your monthly payment, but the whole point of the benefit is that you do not need one. Decide deliberately, not out of habit. Run both scenarios in the calculator.

- Forgetting you might be exempt from the funding fee. If you receive or are eligible for disability compensation, you may owe no fee at all. Do not let a lender quote you a fee you do not owe; check your VA disability status.

- Not shopping lenders. The VA backs the loan, but the lender sets the rate and fees, and those vary. Get quotes from more than one VA-experienced lender.

- Treating the COE as loan approval. The COE only proves entitlement. You still have to qualify on credit and income like any other borrower.

Frequently Asked Questions

What is a VA home loan?

A VA home loan is a mortgage made by a private lender and partially guaranteed by the Department of Veterans Affairs. That guaranty is what lets eligible veterans, active-duty service members, and certain surviving spouses buy a primary home with no down payment and no private mortgage insurance, usually at a better interest rate than a conventional loan. The VA does not lend the money itself; it backs the loan so the lender takes on less risk.

Do you need a down payment for a VA loan?

No. A borrower with full entitlement can finance 100 percent of the purchase price with zero down, as long as the appraisal supports the price and the lender approves the loan. This is the headline benefit of the program. You can choose to put money down to lower your funding fee and monthly payment, but you are never required to.

How much is the VA funding fee in 2026?

For a purchase loan with less than 5 percent down, it is 2.15 percent on first use and 3.3 percent on subsequent use. With 5 percent or more down it drops to 1.5 percent, and with 10 percent or more it falls to 1.25 percent, regardless of whether it is your first use. Cash-out refinances are 2.15 percent first use and 3.3 percent after, and the IRRRL streamline refinance is a flat 0.5 percent. Many disabled veterans and surviving spouses are fully exempt.

Is there a VA loan limit in 2026?

Not for borrowers with full entitlement. The VA will guarantee your loan at any amount your lender approves and the appraisal supports, with no cap. Loan limits only apply to borrowers with reduced entitlement, such as those carrying a second simultaneous VA loan, and those are tied to the 2026 conforming limit of $832,750 in most counties.

Can you use a VA loan more than once?

Yes. The VA loan is a reusable, lifelong benefit. Once you sell a home and pay off the VA loan, your entitlement restores and you can use it again on your next home. In some cases you can hold two VA loans at the same time, which is common for service members who buy at one duty station and then move to another.

Does a VA loan require mortgage insurance?

No. VA loans never require private mortgage insurance, even with zero down. This is one of the biggest savings the program offers, since conventional borrowers pay PMI below 20 percent down and FHA borrowers pay mortgage insurance for most of the loan's life. The one-time funding fee takes the place of that recurring insurance.

Bottom Line

The VA home loan is the rare benefit that is both extremely valuable and underused. If you qualify, no other mainstream mortgage lets you buy with nothing down, skip private mortgage insurance entirely, and get a competitive rate, all backed by entitlement you can reuse for the rest of your life. The funding fee is the only real cost unique to the program, and a large share of disabled veterans and surviving spouses owe none of it. For 2026 the move is straightforward: confirm your eligibility, request your Certificate of Eligibility, decide deliberately whether a down payment makes sense for you, and estimate your real payment and funding fee in the VA loan calculator before you ever talk to a lender. For the deeper detail on the one cost involved, read the VA funding fee 2026 guide.