VA Funding Fee in 2026: Rates, Who Is Exempt, and How to Lower It

VA funding fee 2026: the exact purchase, cash-out, and IRRRL rates, who is exempt, how a down payment cuts the fee, refunds, and the new tax break.

The VA funding fee is the one trade-off that comes with the strongest benefit a service member earns: a home loan that lets you buy with no down payment and no monthly mortgage insurance. It is a one-time charge that goes straight to the Department of Veterans Affairs, not to your lender, and it keeps the loan program running without taxpayer money. On a typical home it can run into the thousands of dollars, so it is worth understanding before you sign anything.

This guide lays out the 2026 funding fee rates exactly as the VA publishes them, walks through who pays nothing at all, and covers the levers that actually move the number on your closing statement. If you want the dollar figure for your specific price, down payment, and use, run it through the VA loan calculator with funding fee rather than estimating off a chart. The percentages below are what feed that math.

What the VA Funding Fee Actually Is

The funding fee is a one-time payment tied to the loan, not a recurring cost. A conventional buyer who puts down less than 20 percent usually pays private mortgage insurance every month for years. An FHA buyer pays both an upfront premium and a monthly one. A VA borrower pays neither. Instead you pay the funding fee once, and that is the whole cost of the guaranty.

Because it replaces ongoing insurance, the fee is best understood as the price of the zero-down feature rather than a penalty. Over the life of a loan, a single funding fee almost always costs less than years of conventional or FHA mortgage insurance would have. That does not make it small in dollar terms, which is why the rest of this guide focuses on whether you owe it at all, and how to keep it as low as possible if you do.

2026 VA Funding Fee Rates

The VA sets the rate by three things: what kind of loan it is, whether this is your first time using the VA loan benefit, and how much you put down. Nothing else changes the percentage. Your credit score, your lender, and your interest rate have no effect on the funding fee.

Purchase and construction loans

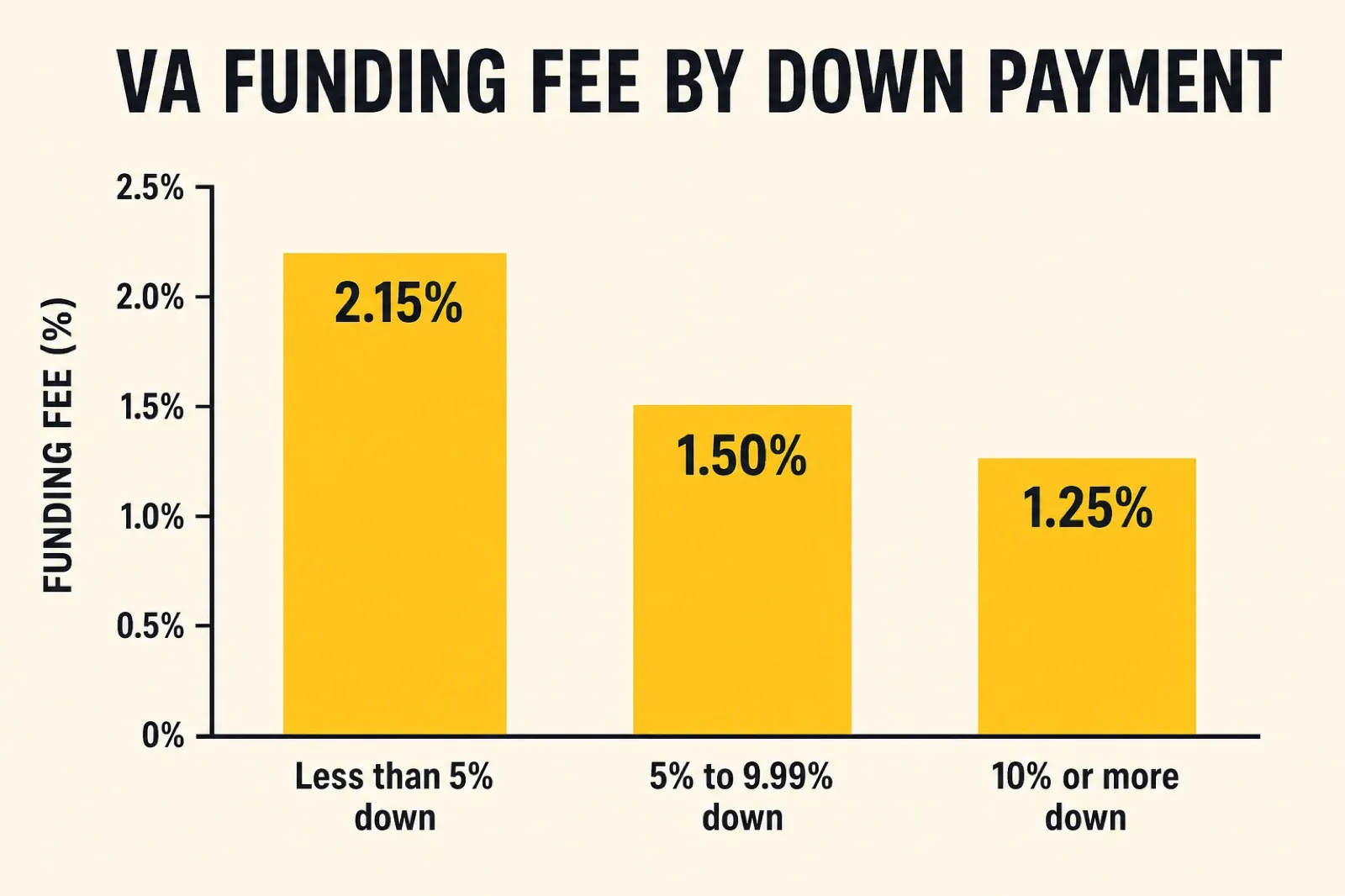

This is the table that applies to most homebuyers using the benefit to purchase a home or build one. The fee is a percentage of the loan amount, not the purchase price, so a down payment shrinks the base the percentage is applied to and lowers the percentage itself.

| Down payment | First use | Subsequent use |

|---|---|---|

| Less than 5% | 2.15% | 3.3% |

| 5% to 9.99% | 1.5% | 1.5% |

| 10% or more | 1.25% | 1.25% |

Two things in that table catch people off guard. First, the penalty for reusing the benefit only shows up in the zero-to-five-percent tier, where the rate jumps from 2.15 percent to 3.3 percent. Once you reach a 5 percent down payment, first use and repeat use cost the same. Second, you do not need anything close to 20 percent down to cut the fee. The full discount lands at 10 percent.

Cash-out refinance

If you refinance to pull equity out of the home, the funding fee works like a purchase but ignores down payment entirely. There is no down-payment tier here.

- First use of the benefit: 2.15 percent

- After first use: 3.3 percent

Interest Rate Reduction Refinance Loan (IRRRL)

The IRRRL, often called a VA streamline refinance, lowers your rate on an existing VA loan with minimal paperwork. Its funding fee is the lowest in the system at a flat 0.5 percent, regardless of how many times you have used the benefit or what equity you hold. That low fee is a big part of why an IRRRL can pay for itself quickly when rates drop.

To see how a streamline compares to your current loan, the refinance side of the VA loan calculator will fold the 0.5 percent fee into the breakeven math for you.

Who Is Exempt From the Funding Fee

A large share of VA borrowers owe no funding fee at all. A VA funding fee exemption is not something you negotiate or apply for at the lender level - it flows from your VA status, and your lender confirms it through the VA system before closing. You are exempt if any one of the following is true.

- You receive VA disability compensation for a service-connected disability. Even a 10 percent rating that pays compensation makes you exempt.

- You are eligible to receive that compensation but are getting retirement pay or active-duty pay instead, so you waived it. Eligibility is what matters, not whether you actually collect the check.

- You are a surviving spouse receiving Dependency and Indemnity Compensation because your service member died in service or from a service-connected cause.

- You are an active-duty service member who received a Purple Heart, with evidence of it dated on or before the loan closing date.

- You have a proposed or memorandum rating, issued before closing on a pre-discharge claim, that establishes your eligibility for compensation.

The recurring theme is timing. The status that makes you exempt has to exist, on paper, before you close. A rating that arrives the week after closing does not retroactively waive the fee at the table. There is a separate refund path for that situation, covered below, but it is a different process with its own rules.

If you are not sure where your disability claim stands or what your current rating pays, the disability compensation calculator can show your monthly amount, and any compensable rating is also your ticket to a waived funding fee. The fee itself is defined in the Funding Fee glossary entry if you want the short version. And if you hold more than one rating, our walk-through of how VA combined disability ratings work explains why your overall percentage is not just the sum of the parts.

A note for surviving spouses

Surviving spouses who qualify for a VA loan through DIC are exempt from the funding fee in the same way a disabled veteran is. They also keep the core no-down-payment, no-mortgage-insurance structure of the loan. The exemption is one of the more valuable and least understood pieces of the survivor benefit, so it is worth confirming with the VA Regional Loan Center if a lender is unsure how to code it.

How a Down Payment Lowers the Fee

For borrowers who do owe the fee, the down payment is the cleanest lever you control. Look again at the purchase table. The fee falls from 2.15 percent to 1.5 percent at 5 percent down, and to 1.25 percent at 10 percent down. The savings compound because a larger down payment also shrinks the loan amount the percentage is charged against.

Take a $400,000 home as an example. With zero down on a first use, the fee is 2.15 percent of $400,000, which is $8,600. Put 5 percent down, or $20,000, and the loan drops to $380,000 while the rate drops to 1.5 percent. That fee is $5,700, a savings of $2,900 on the fee alone. At 10 percent down the fee is 1.25 percent of $360,000, or $4,500.

None of that means a down payment is always the right move. The whole point of the VA loan is that you do not need one, and cash kept liquid for an emergency fund or for closing costs may serve you better than a smaller funding fee. Use the VA funding fee calculator to slide the down payment up and down so you can see the fee change against your own numbers instead of guessing.

Paying the Fee: Roll It In or Pay at Closing

You have two ways to handle the fee. You can pay it in full at closing, out of pocket, or you can finance it by rolling it into the loan and paying it off over the life of the mortgage. Most borrowers finance it, because the appeal of the VA loan is bringing little or no cash to the table.

Financing the fee is convenient but not free. When you roll a $8,600 fee into the loan, you borrow that amount and pay interest on it for as long as you hold the mortgage. Over 30 years that interest can add up to more than the fee itself. If you have the cash and no better use for it, paying the fee upfront avoids financing it at your mortgage rate. If cash is tight, rolling it in is exactly what the option exists for. Neither choice is wrong, it is a question of where your dollars do the most good.

One practical detail: the financed funding fee is allowed to push your loan amount above the home's value by the amount of the fee, so financing it does not blow up your loan-to-value calculation the way an ordinary overage would. Your lender handles this automatically.

How to Get a VA Funding Fee Refund After Closing

Timing trips up a lot of veterans whose disability claims are still pending when they buy. Here is the rule that matters. If you pay the funding fee at closing and are later awarded VA disability compensation with an effective date that falls before your loan closing date, you are owed a refund of the fee.

The effective date is the hinge. It is the date your compensation is considered to have started, which is often earlier than the date the award letter arrives. If that effective date predates your closing, you were technically exempt all along and the VA refunds the fee. If your rating's effective date lands after closing, you are not eligible for a refund, even if the letter shows up soon after.

To pursue a refund, contact your loan servicer or call the VA Regional Loan Center at 877-827-3702. For refunds issued on or after July 1, 2019, the VA pays the refund directly to the veteran rather than applying it to the loan balance, so the money comes back to you.

The New 2026 Tax Deduction

Starting with the 2026 tax year, the VA funding fee is tax deductible again for many borrowers. The deduction for mortgage insurance premiums, which had lapsed after 2021, was restored, and the VA funding fee is treated as an upfront mortgage insurance premium for this purpose. That means eligible veterans, service members, and surviving spouses who pay the fee may be able to write it off.

A few conditions apply, and they matter. You generally have to itemize deductions on Schedule A rather than take the standard deduction, which only helps if your itemized total beats the standard deduction. Income limits can reduce or phase out the deduction at higher earnings. And a financed fee, spread across the loan, is treated differently for taxes than a fee paid in cash at closing, so the bookkeeping is not identical.

This is genuinely new for 2026 and the rules are nuanced, so treat it as a reason to talk to a tax professional rather than a guaranteed refund. The deduction is a nice offset, but it does not change the calculus of whether to pay or finance the fee, and it never beats being outright exempt.

How the Fee Fits With Entitlement and Loan Limits

The funding fee is separate from your VA loan entitlement, but the two interact in ways that surprise repeat buyers. Entitlement is the amount of the loan the VA guarantees to your lender. If you have full entitlement, there is no VA-imposed loan limit and no down payment required, and your funding fee follows the purchase table above based purely on use and any down payment you choose to make.

If you have reduced entitlement, usually because you still have an active VA loan on another property, the picture changes. You may need a down payment to satisfy the lender's loan-to-value requirements on the new home. That required down payment is not a penalty, and it has a side benefit: if it pushes you to 5 percent or 10 percent down, it also drops your funding fee rate. So the same cash that restores your buying power can also trim the fee, which softens the blow of carrying two VA loans at once.

Restoring entitlement after selling a home or paying off a prior VA loan is a paperwork step worth completing before you shop, because it can move you back to full entitlement and remove a required down payment entirely. None of this changes the funding fee percentages, but it changes which row of the table you land on, and that is the part that costs or saves you money.

A Worked Example: Buy Now or Refinance Later

Say you are an E-6 buying a $350,000 home on your first use, with no disability rating yet and no cash for a down payment. Your funding fee is 2.15 percent of $350,000, or $7,525, and you finance it into the loan. A year later, rates have fallen and you want to lower your payment.

Because you now have an existing VA loan, the cheapest path is an IRRRL. Its funding fee is just 0.5 percent, so on a roughly $345,000 balance the fee is about $1,725 - a fraction of what a fresh purchase or cash-out would charge. This is the quiet advantage of the VA program: the expensive fee is the one-time entry, and staying inside the system to refinance is deliberately cheap. The streamline side of the VA loan calculator will show whether the lower rate clears that $1,725 fee fast enough to be worth it.

Now flip one detail. Suppose during that first year your pending disability claim is granted with an effective date before your purchase closing. You were exempt all along, so the original $7,525 fee is refundable, and the VA pays it back to you directly. That single timing fact can be worth more than the refinance.

Common Mistakes to Avoid

A few errors show up again and again, and all of them are avoidable.

Assuming a high rating gets you a discount

The funding fee is binary. Either you are exempt and pay zero, or you are not and pay the full rate. A 100 percent disability rating does not get you a "bigger discount" than a compensable 10 percent rating - both produce a $0 fee. There is no partial exemption.

Closing before a pending claim resolves

If you are close to a disability decision and your effective date will land before closing, the refund path protects you. But the cleaner outcome is to have the rating in hand before closing so the fee is never charged. If your timeline is flexible and a decision is days away, it can be worth a short delay.

Forgetting the fee exists when comparing offers

Because the funding fee is rolled into so many quotes automatically, some buyers never see it as a line item and are surprised at closing. Ask your lender to show the funding fee separately on your loan estimate, and run a VA home loan closing cost calculator alongside it, so you know exactly what you are paying and can confirm whether you should be exempt.

Treating the fee as a reason to skip the VA loan

Even with the fee, the VA loan usually wins against conventional and FHA options for eligible borrowers, because it has no down-payment requirement and no monthly mortgage insurance. The one-time fee is almost always cheaper than years of monthly insurance. If you are weighing housing costs more broadly, the BAH calculator can tell you how much allowance you have to put toward a mortgage in the first place.

Quick Reference

- Purchase, first use, less than 5 percent down: 2.15 percent

- Purchase, subsequent use, less than 5 percent down: 3.3 percent

- Purchase, any use, 5 to 9.99 percent down: 1.5 percent

- Purchase, any use, 10 percent or more down: 1.25 percent

- Cash-out refinance: 2.15 percent first use, 3.3 percent after

- IRRRL streamline refinance: 0.5 percent flat

- Exempt borrowers pay nothing, regardless of the table above

Frequently Asked Questions

Can the VA funding fee be rolled into the loan?

Yes. You can finance the funding fee by adding it to your loan balance and paying it off over the life of the mortgage, which is what most borrowers do. The financed fee is allowed to push your loan amount above the home's value by the amount of the fee, so it does not break your loan-to-value math. The trade-off is that you pay mortgage-rate interest on it for as long as you hold the loan.

Is the VA funding fee tax deductible?

Starting with the 2026 tax year, the funding fee is treated as an upfront mortgage insurance premium and may be deductible. You generally have to itemize on Schedule A, income limits can phase out the deduction, and a financed fee is handled differently than one paid in cash at closing. Talk to a tax professional, since the rules are new and depend on your situation.

VA funding fee vs PMI: what is the difference?

PMI is private mortgage insurance that a conventional borrower pays every month, often for years, when they put down less than 20 percent. The VA funding fee replaces that ongoing cost with a single one-time charge and no monthly insurance at all. Over the life of a loan, the one-time funding fee almost always costs less than years of monthly PMI.

Who is exempt from the VA funding fee?

You are exempt if you receive VA disability compensation for a service-connected condition, are eligible for that compensation but waived it for retirement or active-duty pay, are a surviving spouse receiving Dependency and Indemnity Compensation, are an active-duty Purple Heart recipient with evidence dated on or before closing, or hold a qualifying proposed or memorandum rating issued before closing. The status has to exist on paper before you close.

Does the max VA loan amount include the funding fee?

The funding fee can be financed on top of the home's value, so a financed fee does not count against your loan-to-value calculation. With full entitlement there is no VA-imposed loan limit, and the financed fee simply rides on top of the loan amount. Your lender adds it automatically without it counting as an ordinary overage.

How do you get a VA funding fee refund?

If you pay the fee at closing and are later awarded VA disability compensation with an effective date before your loan closing date, you are owed a refund. Contact your loan servicer or call the VA Regional Loan Center at 877-827-3702 to start the process. For refunds issued on or after July 1, 2019, the VA pays the money directly to the veteran rather than applying it to the loan balance.

The funding fee is real money, but it is one of the most controllable costs in the entire VA loan. Confirm your exemption status first, since that question alone can erase the fee entirely. If you do owe it, decide whether a down payment or paying the fee upfront fits your cash situation, and look into the 2026 tax deduction at filing time. To put your own numbers against all of this, the VA loan calculator will show the exact fee and how it changes the moment you adjust your down payment or use status.