VA Home Loan Requirements: COE, Credit & DTI Explained

VA home loan requirements for 2026 - the Certificate of Eligibility, service history, credit and DTI guidelines, funding fee, and what full entitlement means for your down payment.

The VA home loan is one of the strongest benefits a service member earns, and the rules around it confuse people more than they should. There is no down payment requirement, no private mortgage insurance, and no government-set credit score cutoff. What there is instead is a short list of requirements that fall into two buckets: the ones the Department of Veterans Affairs sets to prove you are entitled to the benefit, and the ones your lender sets to prove you can repay the loan. Mixing those two up is the single biggest source of confusion, so this guide keeps them separate.

The VA home loan requirements that matter in 2026 are your service history, your Certificate of Eligibility, satisfactory credit, a manageable debt-to-income ratio, and enough residual income to cover daily living costs. Below is exactly what each one means, the current numbers behind them, and where the VA's rule ends and your lender's discretion begins. The actual dollar figures swing with the home price, your entitlement, and the funding fee, so as you read, run your own purchase through the VA loan calculator to see what the requirements add up to for your situation.

The Two Layers of VA Loan Requirements

Every VA purchase has to clear two separate sets of rules, and they are owned by different parties.

The VA owns eligibility. It decides, based on your service, whether you have earned the benefit at all and how much of it (your entitlement). It guarantees a portion of the loan to the lender, which is what lets the lender offer no down payment and no mortgage insurance. The VA also sets baseline underwriting standards in its Lenders Handbook, including the residual income tables and the 41 percent debt-to-income benchmark.

The lender owns approval. Because the VA only guarantees part of the loan and the lender funds all of it, the lender carries real risk and is allowed to add its own requirements on top of the VA's. These extra rules are called overlays. The most common overlay is a minimum credit score. The VA itself sets no credit score floor, but almost every lender does.

So when you hear conflicting things about VA loan requirements, it is usually because one source is describing the VA's rule and another is describing a typical lender's overlay. Both are real. You have to satisfy both.

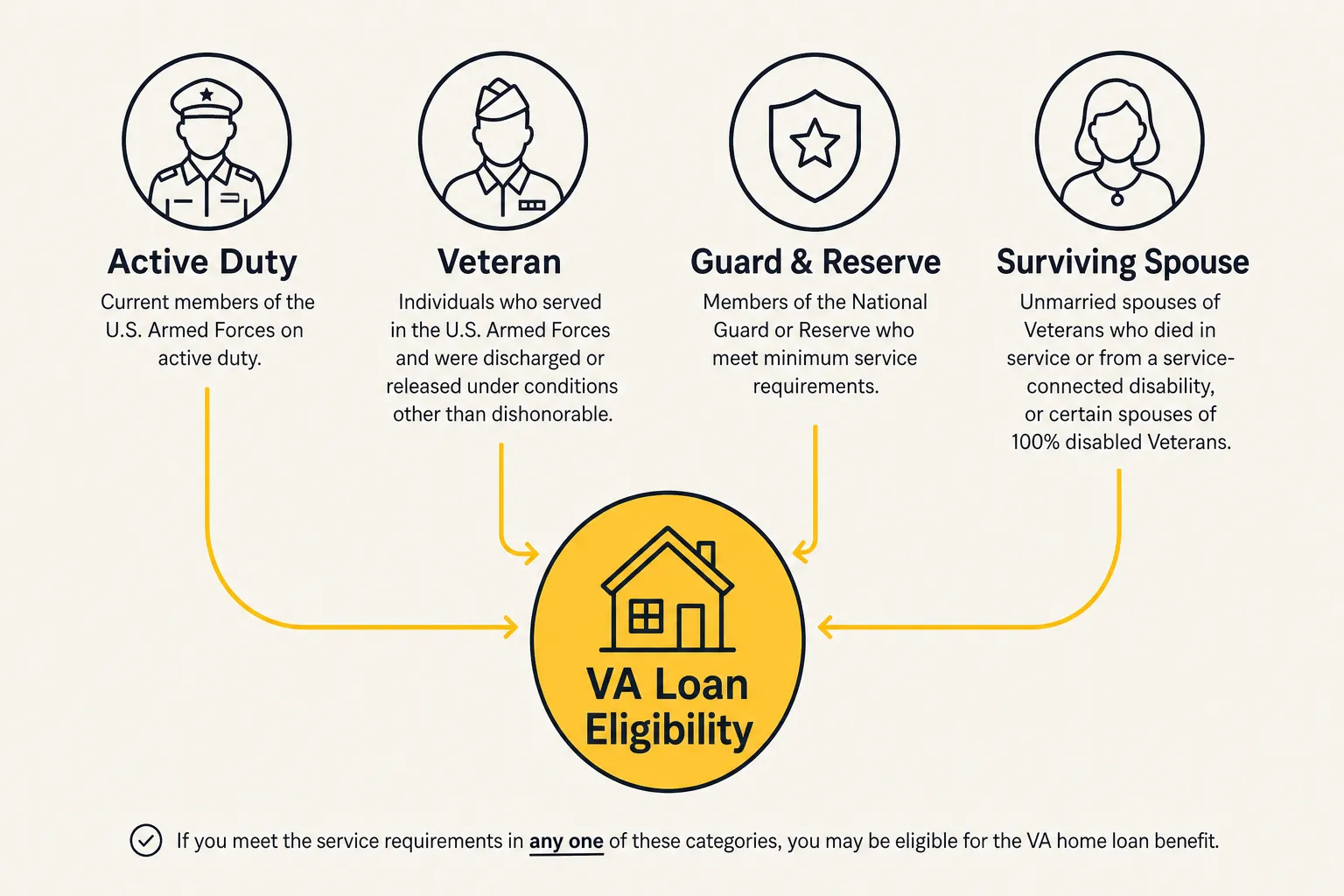

Service Eligibility Requirements

The first question is whether your service qualifies you at all. The minimum depends on when you served and in what capacity. These thresholds come straight from the VA's eligibility rules.

Active-duty service members

If you are currently serving on active duty, you become eligible after 90 continuous days of service. You do not have to wait for a discharge to use the benefit while still in uniform.

Veterans, by era of service

For separated veterans, the minimum length of service depends on your service era:

- Gulf War era (August 2, 1990 to present): at least 24 continuous months, or the full period you were called to active duty (at least 90 days), or a qualifying early discharge.

- September 8, 1980 to August 1, 1990: at least 24 continuous months, or the full period you were called to active duty (at least 181 days), or a qualifying early discharge.

- May 8, 1975 to September 7, 1980: 181 continuous days.

- Vietnam era (August 5, 1964 to May 7, 1975): at least 90 total days.

- Earlier wartime eras (WWII, Korea): at least 90 total days.

The 24-month rule for post-1980 service has exceptions. If you were discharged early for a service-connected disability, a hardship, a reduction in force, or certain other qualifying reasons, you can still be eligible with less time served.

National Guard and Reserve members

Guard and Reserve members qualify one of two ways. Either you served at least 90 days of active-duty service (not active duty for training), or you completed at least 6 creditable years in the Selected Reserve or Guard and were honorably discharged, placed on the retired list, or transferred to an active status reserve unit. The Guard and Reserve path is real and often overlooked, but the six-year service record has to be documented.

Surviving spouses

A surviving spouse can inherit the benefit. The two main paths are being the un-remarried spouse of a service member who died in the line of duty or from a service-connected disability and who is receiving VA Dependency and Indemnity Compensation, or being the spouse of a service member who is missing in action or a prisoner of war. Surviving spouses use VA Form 26-1817 to establish eligibility rather than the standard request, and many of them are also exempt from the funding fee.

Character of discharge

Your discharge generally has to be under conditions other than dishonorable. An honorable or general (under honorable conditions) discharge usually qualifies. An other-than-honorable, bad conduct, or dishonorable discharge can disqualify you, but it is not automatically the end of the road. The VA runs a Character of Discharge review that can find your service qualifying despite the discharge type, and discharge upgrades exist. Check your DD-214 for the character of service before assuming you do not qualify.

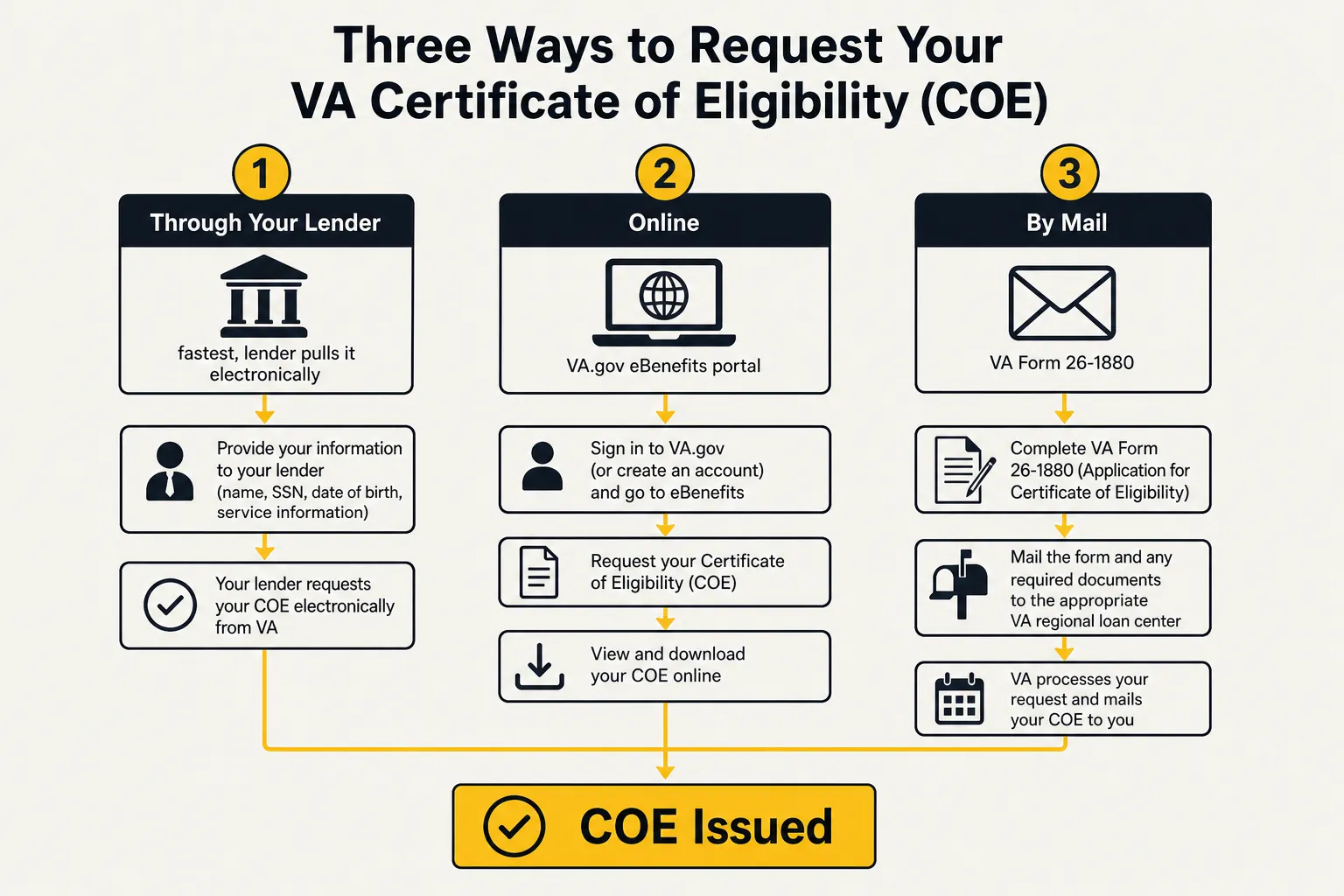

The Certificate of Eligibility (COE)

Once your service qualifies you, the document that proves it to a lender is the Certificate of Eligibility. The Certificate of Eligibility is not the loan and it is not pre-approval. It is a single VA-issued statement that confirms you are entitled to the benefit and shows how much entitlement you have available.

What the COE actually shows

The COE tells the lender two things: that you meet the service requirement, and what your entitlement status is. That second part matters because it determines whether you can buy with zero down and no county loan limit, which the next section covers in detail. If you have used a VA loan before and have not restored that entitlement, the COE reflects the reduced amount remaining.

Three ways to get your COE

There is no single "apply" button, but there are three reliable paths:

- Through your lender. This is the fastest route for most people. Lenders have direct access to the VA's Web LGY portal and can often pull your COE in minutes during the pre-approval conversation. If you are already talking to a lender, let them do it.

- Online yourself. You can request it through VA.gov by signing in to the Health and Benefits portal and using the housing assistance section. (The old eBenefits portal has been retired and its services moved to VA.gov, so VA.gov is now the place to do this.) The Health and Benefits mobile app surfaces the COE too.

- By mail. Submit VA Form 26-1880 (or Form 26-1817 for surviving spouses) if the automated systems cannot verify your service.

Documents you may need

If the portal cannot pull your record automatically, have your paperwork ready. Veterans need a copy of their discharge or separation papers (DD-214) showing character of service. Active-duty members need a current statement of service signed by the commander, adjutant, or personnel officer, showing your name, Social Security number, date of birth, entry date, and any lost time. Guard and Reserve members may need a points statement and proof of honorable service.

Entitlement, Loan Limits, and the Zero-Down Benefit

Entitlement is the part of VA loan requirements that gets misunderstood the most, partly because the rules changed and a lot of outdated advice is still floating around.

Full entitlement means no loan limit

As of January 1, 2020, the Blue Water Navy Vietnam Veterans Act of 2019 eliminated VA county loan limits for borrowers with full entitlement. If you have your full entitlement, there is no cap on how much you can borrow with zero down. The VA will guarantee 25 percent of the loan amount regardless of the home price, and the limit on what you can borrow comes from what your lender will approve based on your income and credit, not from a VA ceiling.

You have full entitlement if you have never used your VA home loan benefit, or you have paid a previous VA loan in full and sold the property, or you had a foreclosure on a prior VA loan but have since repaid the VA in full.

Partial entitlement still has limits

If you currently have an active VA loan, or you used the benefit and have not restored it, you have partial (remaining) entitlement. In that case the old county loan limits still apply to the calculation, and you may need a down payment if the new loan is large. This is the one scenario where the published conforming loan limits still matter to a VA borrower.

What this means for your down payment

For a borrower with full entitlement, the headline benefit is real: zero down payment, on any loan amount the lender approves. That is the feature that makes the VA loan worth the effort. Run a purchase price through the VA loan calculator to see how the no-money-down structure changes your closing cash compared with a conventional loan that demands 5, 10, or 20 percent up front.

Credit and Income Requirements

This is where the lender's overlays live. The VA sets a framework, and the lender fills in the specific thresholds.

Credit score: the VA sets none, lenders do

The VA has no minimum credit score requirement. That is a real feature of the program, not a marketing line. What the VA requires is "satisfactory credit," which its underwriters judge by looking at your payment history, any derogatory marks, and whether past problems have been resolved.

Lenders, though, almost always set a minimum score as an overlay. In 2026 the most common floor sits around 620, with some lenders going lower and some setting it higher. So while the VA will guarantee a loan for a borrower with a thin or bruised credit file, you have to find a lender whose overlay you clear. If one lender turns you down on score alone, another with a lower overlay may approve you on the same file.

A bankruptcy or foreclosure does not permanently block you. The VA generally looks for a seasoning period (commonly two years after a Chapter 7 bankruptcy and often two years after a foreclosure) with re-established good credit since.

Debt-to-income ratio: the 41 percent benchmark

The VA's underwriting guideline puts the target debt-to-income ratio at 41 percent. That figure is your total monthly debt payments, including the new mortgage, divided by your gross monthly income.

Here is the part most summaries get wrong: 41 percent is a benchmark, not a hard cutoff. A DTI above 41 percent does not automatically kill the application. When the ratio runs higher, the underwriter takes a closer look and can still approve the loan if other factors are strong. The VA specifically allows higher DTIs when your residual income exceeds the required amount by at least 20 percent, and tax-free income (like VA disability compensation) can be grossed up because it stretches further than taxable pay. If an underwriter approves a loan above the 41 percent mark, they have to document in writing why the borrower is still a sound risk.

Residual income: the requirement that makes VA loans safer

Residual income is the VA's signature underwriting test and the reason VA loans have historically had low foreclosure rates despite zero down. After you subtract your mortgage payment, all other monthly debts, estimated taxes, insurance, utilities, and maintenance from your take-home pay, what is left over has to meet a minimum.

That minimum varies by region of the country (Northeast, Midwest, South, West), by family size, and by loan amount. A larger family in a higher-cost region needs more left over each month. Residual income is often the deciding factor for borrowers with a higher DTI: if you clear the residual income table comfortably, the loan can be approved even with debt ratios that would sink a conventional application. Because the tables are specific to your family size and region, the cleanest way to see whether you pass is to model your full monthly picture rather than eyeball it.

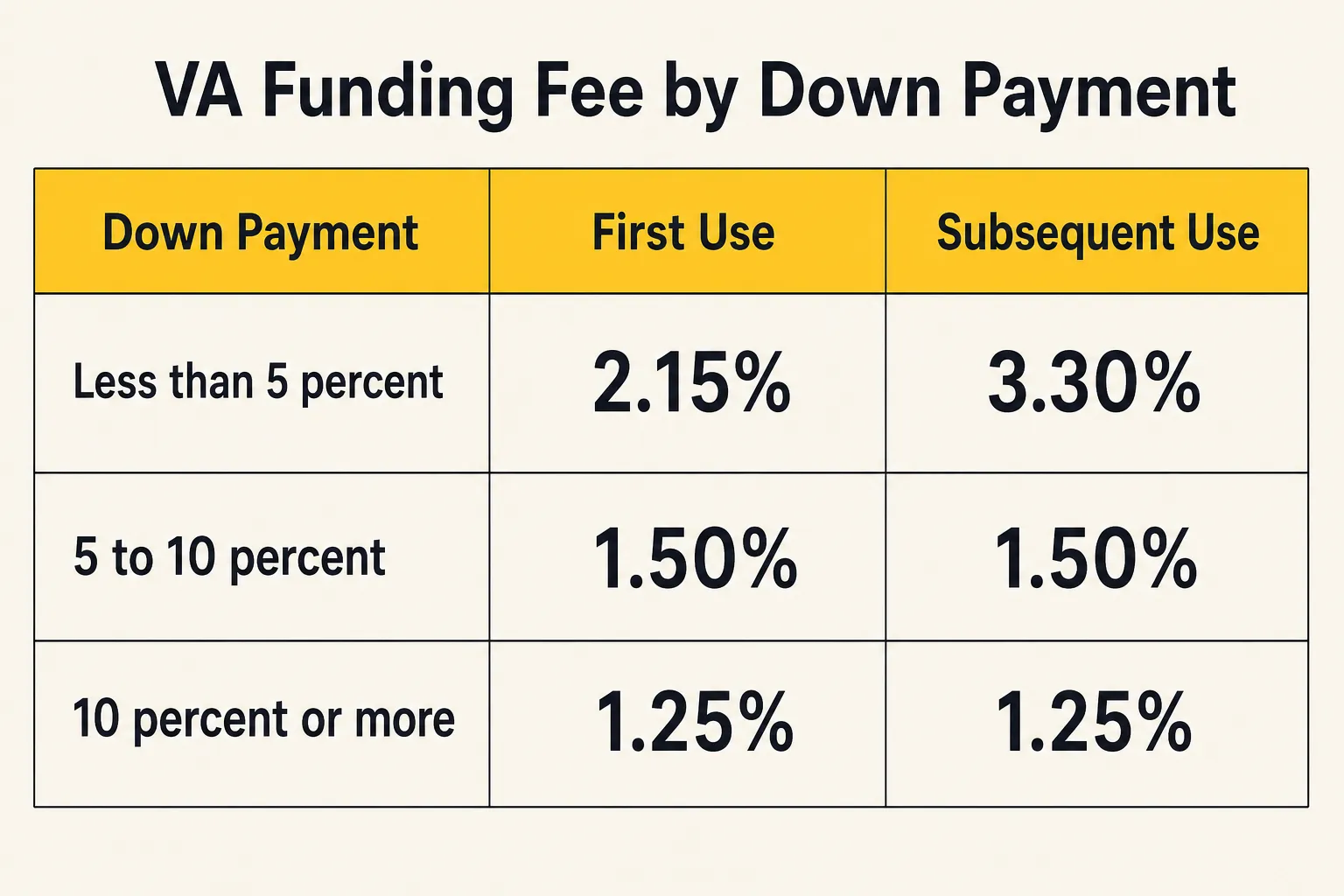

The VA Funding Fee

The VA funding fee is not a credit or income requirement, but it is a cost requirement you have to plan for, and it surprises a lot of first-time buyers. It is a one-time fee paid to the VA that keeps the loan program running at no cost to taxpayers, and it replaces the mortgage insurance you would pay on other low-down-payment loans.

Current funding fee rates

For purchase and construction loans, the rates effective since April 7, 2023 (and still current in 2026) depend on your down payment and whether this is your first use of the benefit:

| Down payment | First use | Subsequent use |

|---|---|---|

| Less than 5% | 2.15% | 3.3% |

| 5% to less than 10% | 1.5% | 1.5% |

| 10% or more | 1.25% | 1.25% |

A few things stand out in that table. First, even a modest down payment cuts the fee sharply: putting 5 percent down drops a first-time buyer from 2.15 percent to 1.5 percent, and a repeat user from 3.3 percent all the way to 1.5 percent. Second, the penalty for subsequent use only applies when you put less than 5 percent down. For other loan types, an Interest Rate Reduction Refinance Loan (IRRRL, the VA streamline refinance) carries a flat 0.5 percent fee, and a cash-out refinance follows the 2.15 percent first-use and 3.3 percent subsequent-use pattern.

Who is exempt from the funding fee

You owe no funding fee at all if you fall into an exempt category. The main ones are:

- You receive VA compensation for a service-connected disability.

- You are eligible for VA compensation but receive retirement or active-duty pay instead.

- You are a surviving spouse receiving Dependency and Indemnity Compensation.

- You have a proposed or memorandum disability rating before the loan closes, from a pre-discharge claim.

- You are an active-duty service member who provides evidence of a Purple Heart on or before the closing date.

The disability exemption is the big one. If you have any service-connected disability rating that pays compensation, your funding fee is waived entirely, which on a typical loan saves thousands of dollars. If you have a VA disability claim in progress, it is worth understanding how a rating would affect this fee before you close. You can estimate where a combined rating might land using the VA disability calculator.

Paying the fee

The funding fee can be rolled into the loan amount and financed over the life of the mortgage, or paid in cash at closing. Most borrowers roll it in to keep closing cash low, though that does mean paying interest on it. For a detailed breakdown of how the fee is calculated and financed, see the VA funding fee guide for 2026.

Property and Appraisal Requirements

The home itself has to meet requirements too, and this catches buyers off guard because it is stricter than a conventional appraisal.

A VA loan can only be used for a primary residence, a home you intend to live in, not a pure investment property or a vacation home. Beyond the standard appraisal that establishes value, the VA appraiser also checks the property against the VA's Minimum Property Requirements. These confirm the home is safe, structurally sound, and sanitary: working utilities, a sound roof, safe mechanical systems, adequate heating, no exposed wiring, clean water, and no health or safety hazards.

This protects the buyer, but it can complicate purchases of fixer-uppers or distressed properties. A home that fails the Minimum Property Requirements has to be repaired before the loan can close, and sellers of as-is properties sometimes balk at that. It is worth knowing going in so a failed inspection does not blindside your timeline.

Putting the Requirements Together

Stack the layers and the path is clearer than the rulebook makes it look:

- Confirm your service qualifies using the era-based minimums above.

- Get your Certificate of Eligibility, fastest through a lender.

- Check your entitlement status, since full entitlement means no loan limit and zero down.

- Meet the lender's credit overlay, commonly around a 620 score, even though the VA sets none.

- Clear the income tests, the 41 percent DTI benchmark and the residual income table.

- Budget for the funding fee, unless a disability rating or other exemption waives it.

- Pass the property appraisal against the Minimum Property Requirements.

Each step is a yes-or-no gate, and the calculator turns the financial gates into real numbers. Plug your purchase price, down payment, and funding fee status into the VA loan calculator to see your monthly payment and closing cash before you ever talk to a lender.

Frequently Asked Questions

What are the basic requirements for a VA home loan?

You need qualifying military service (generally 90 continuous days on active duty, 24 months for most post-1980 veterans, or 6 creditable years in the Guard or Reserve), a Certificate of Eligibility proving it, satisfactory credit, a debt-to-income ratio at or near the VA's 41 percent benchmark, and enough residual income for your region and family size. The home must also be your primary residence and pass the VA appraisal.

Is there a minimum credit score for a VA loan?

The VA itself sets no minimum credit score. It requires "satisfactory credit" judged on your overall history. Lenders, however, almost always add a minimum-score overlay, most commonly around 620 in 2026. Because lenders set their own floors, a borrower turned down by one lender on score may be approved by another with a lower overlay.

What is the VA loan debt-to-income limit?

The VA's underwriting benchmark is a 41 percent debt-to-income ratio. It is a guideline, not a hard cap. Loans above 41 percent can still be approved when residual income exceeds the required amount by at least 20 percent or other compensating factors are strong, and the underwriter documents the reasoning.

How do I get a Certificate of Eligibility?

The fastest way is to have your lender pull it through the VA's Web LGY portal, often during pre-approval. You can also request it yourself online by signing in to VA.gov (the old eBenefits portal has been retired and its functions moved there), or by mailing VA Form 26-1880 (Form 26-1817 for surviving spouses). Have your DD-214 or a signed statement of service ready in case automatic verification fails.

Do I have to pay a VA funding fee?

Most borrowers do, but not all. The fee ranges from 1.25 to 3.3 percent of the loan for purchases, depending on your down payment and whether it is your first use. You are exempt if you receive VA disability compensation, are a surviving spouse receiving DIC, or meet another exemption such as a qualifying Purple Heart. The fee can be financed into the loan or paid at closing.

Is there a loan limit on a VA loan?

Not if you have full entitlement. Since January 1, 2020, VA county loan limits were eliminated for full-entitlement borrowers, so you can buy with zero down at any price your lender approves. County limits still apply only if you have partial entitlement, meaning you have an active VA loan or used the benefit without restoring it.

Can I use a VA loan more than once?

Yes. The benefit is reusable for life. If you sell a home and pay off the VA loan in full, your full entitlement is restored and you can buy again with zero down. You can even hold more than one VA loan at a time using remaining entitlement, though the second purchase may then involve a loan limit and possibly a down payment.

Bottom Line

VA home loan requirements look intimidating until you separate the VA's rules from the lender's. The VA decides whether your service earned the benefit, issues the Certificate of Eligibility, and sets the residual income and 41 percent DTI framework. The lender decides whether to approve you and adds its own overlays, most importantly a credit score floor the VA does not impose. Clear both layers and the payoff is unmatched among mortgage programs: zero down, no mortgage insurance, no loan limit on full entitlement, and a funding fee that disappears entirely if you carry a disability rating. Confirm your eligibility, pull your COE, and run your actual numbers through the VA loan calculator so the requirements stop being abstract and start being a real monthly payment you can plan around.