VA Loan Certificate of Eligibility (COE): How to Get Yours

How to get your VA loan Certificate of Eligibility in 2026 - the three ways to request a COE, exact documents by service type, and what it does and does not do.

The VA Certificate of Eligibility, or COE, is the single document that proves to a lender you have earned the VA home loan benefit. It is not the loan, it is not an approval, and it does not tell you how much house you can buy. It is the green light that lets a VA-backed mortgage even start. Without it your lender cannot close a VA loan, which is why getting it sorted early saves you the most stress later.

The good news is that for most veterans and service members the COE is fast and free. Many people get one in days, and a large share never have to lift a finger because their lender pulls it automatically. This guide walks through what the COE actually does, the three ways to request it, the exact documents you need for your situation, and the common snags that slow people down. When you are ready to see what your monthly payment and funding fee would look like, run your numbers through the VA loan calculator as you read.

What the COE Is and What It Is Not

A Certificate of Eligibility is the VA's official confirmation that you meet the service requirements for a VA-backed home loan. It also shows your entitlement, which is the dollar backing the VA pledges to the lender, and it flags whether you are exempt from the funding fee.

Here is what trips people up. A COE confirms eligibility, not affordability. It says nothing about your credit score, your income, your debt-to-income ratio, or the appraisal of the home. Those are all handled by your lender during underwriting, and they decide the actual loan amount. So you can hold a perfectly valid COE and still be turned down for a loan, and you can have a COE that does not list a loan limit at all and still borrow a large amount, because limits depend on your entitlement rather than the certificate itself.

Two more points worth getting straight up front:

- The COE does not expire on a fixed date. It stays valid as long as your eligibility and the information on it remain accurate. If your circumstances change, for example you return to active duty or your disability status changes, the certificate may need to be updated.

- You do not always need it in hand before you start. Plenty of buyers begin house hunting and get pre-approved while the lender requests the COE in the background. It just has to be in the file before the loan closes.

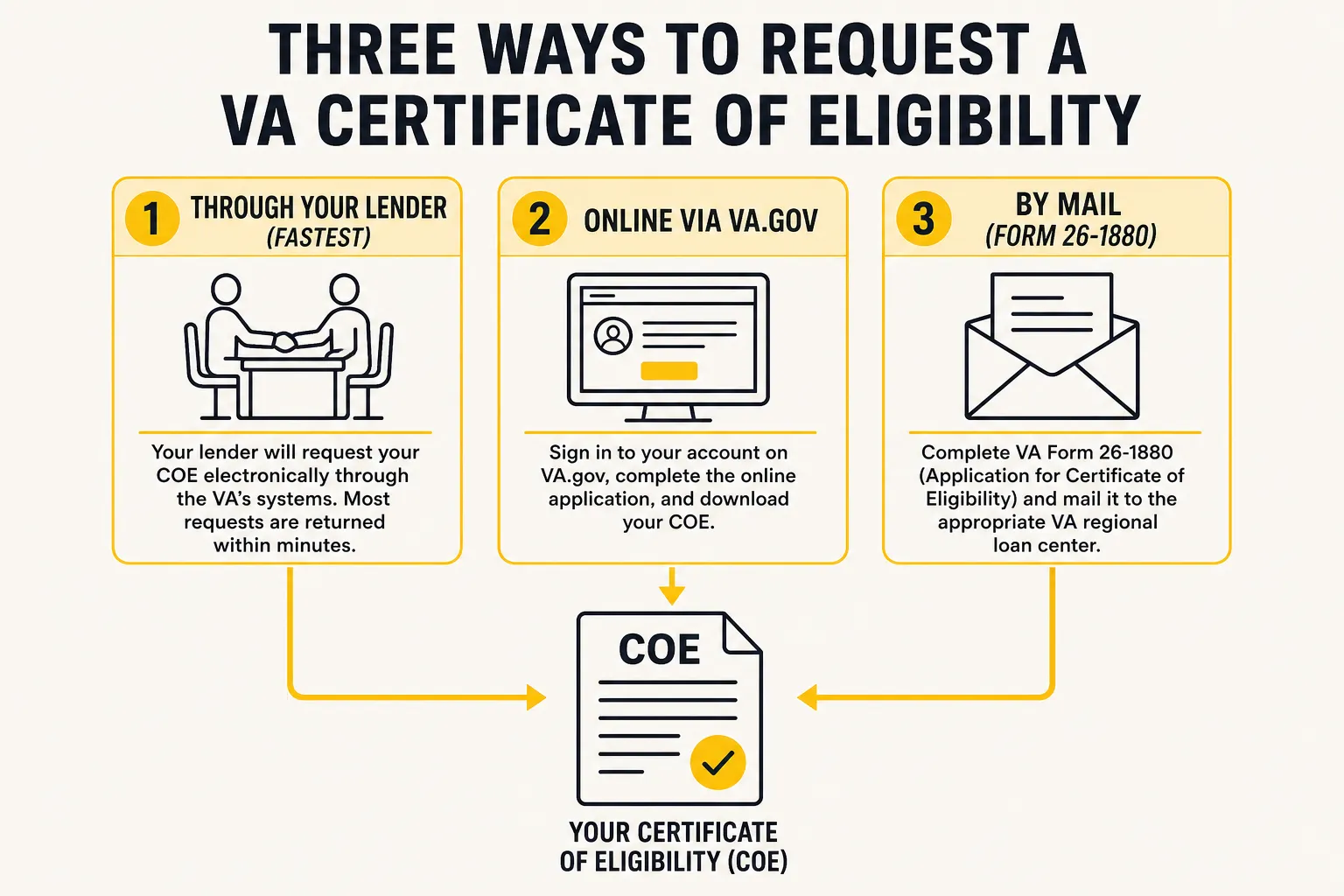

The Three Ways to Request a COE

The VA gives you three official routes. They all reach the same place, but they differ a lot in speed and effort.

1. Through your lender (usually the fastest)

This is the route most borrowers actually use without realizing it. Most VA-approved lenders have direct access to the VA's online system and can pull your COE in minutes while you sit at their desk. If you are already working with a lender to get pre-approved, simply ask them to request it. In many cases they will have it back before you have finished the rest of your paperwork.

The catch is that the automated system only succeeds when your service records are complete and clean in the VA's database. If something does not match, the lender's instant request fails and you fall back to one of the other two routes. That is not a problem with your eligibility, it is just a records gap that needs a document to fill it.

2. Online through VA.gov

You can request a COE yourself by signing in at VA.gov and choosing "Request a COE." This is free and works well for veterans whose discharge is already on file with the VA. The VA states that its goal for contacting COE applicants is an average of about five business days, so this is not always instant, but it is straightforward and you can check the status of your request online afterward.

This route is handy if you want your own copy in hand before you even pick a lender, or if you are comparing several lenders and do not want to wait for each one to pull it separately.

3. By mail

If the online and lender routes both stall, you can fall back to mailing a paper application. You fill out VA Form 26-1880, the Request for a Certificate of Eligibility, and send it to your VA regional loan center. The mailing addresses are printed on the form. This is the slowest route by far, so treat it as the backup when the records system cannot verify you automatically, not as your first move.

Documents You Need by Service Type

The reason an automated COE request sometimes fails comes down to documents. The VA needs proof of your service, and which proof depends on who you are. Gather the right paperwork before you apply and you sidestep the most common delay.

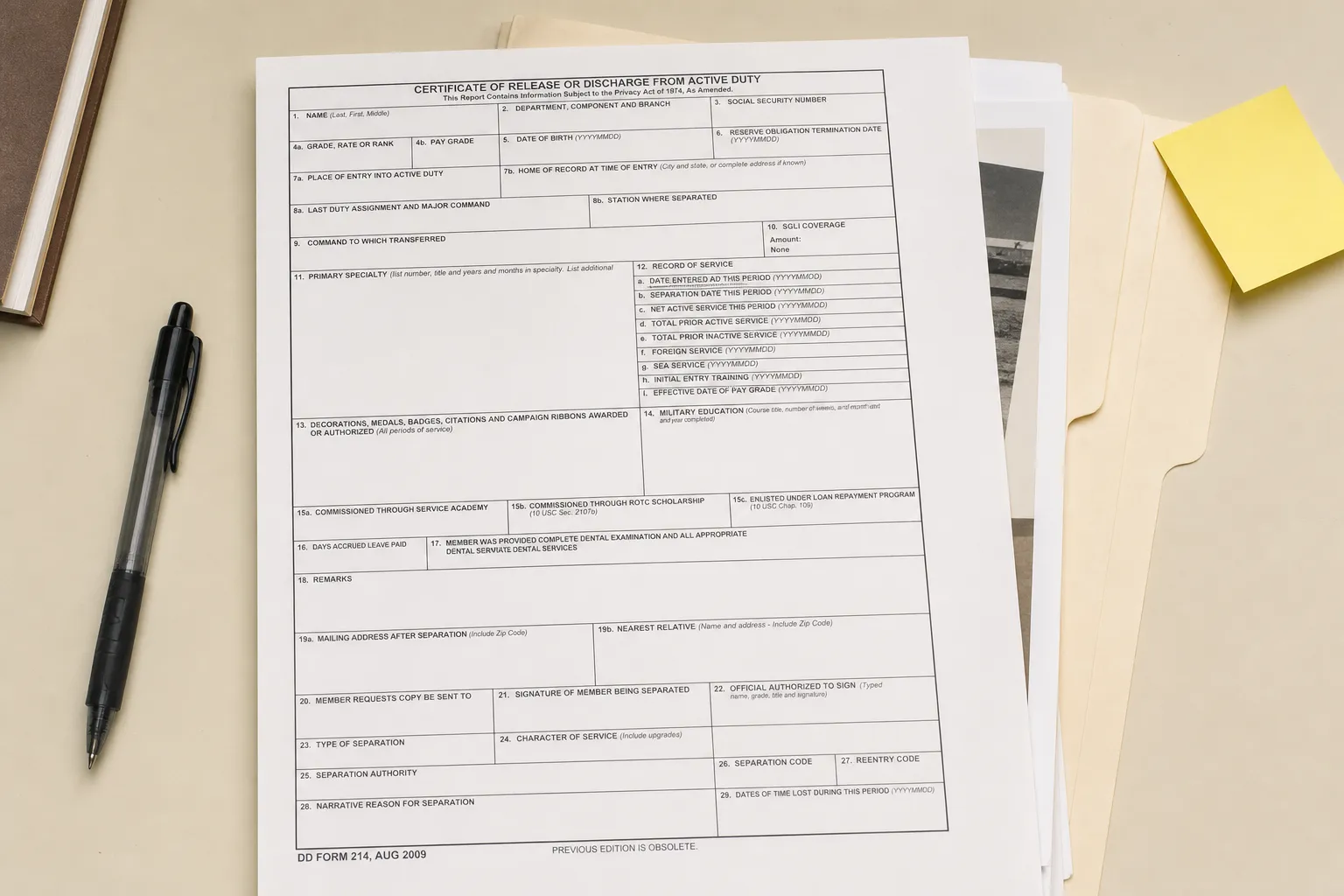

Veterans (separated or retired)

You need a copy of your discharge or separation papers, the DD214. Make sure it is a copy that shows the character of service and the dates, since the VA reads both to confirm you meet the length-of-service rules. A member copy that includes the narrative reason for separation is the safest version to submit.

Active-duty service members

If you are still serving, you will not have a DD214 yet, so the VA uses a statement of service instead. This is a signed letter from your commander, adjutant, or personnel officer that includes your full name, Social Security number, date of birth, the date you entered service, any lost time, and the name of the command providing the information. There is no standard government form for this, so ask your unit's personnel or admin office to draft it on official letterhead.

National Guard and Reserve members

This is the category with the most variations, because the documents differ depending on whether you were ever activated on federal orders.

- If you were activated for at least 90 days, you generally provide your DD214 covering that active-duty period. If you served 90 or more days, with 30 of them consecutive, the VA may also accept a DD214 showing the activation authority, an annual points statement, or a DD Form 220 with the orders that called you up.

- If you have never been activated and are still serving, you provide a statement of service signed by your commander or personnel officer, with the same details an active-duty statement requires plus your years of creditable service.

- If you have separated from the Guard and were never activated, you provide an NGB Form 22 for each period of service plus an NGB Form 23, your retirement points statement, showing honorable service.

- If you have separated from the Reserve and were never activated, you provide your latest annual retirement points statement along with proof of honorable service.

Surviving spouses

A surviving spouse can be eligible for the VA home loan benefit, and the documents depend on whether you receive Dependency and Indemnity Compensation, known as DIC.

- If you receive DIC, you submit VA Form 26-1817, the Request for Determination of Loan Guaranty Eligibility for Surviving Spouses.

- If you do not receive DIC, you submit VA Form 21P-534EZ, your marriage license, and the veteran's death certificate.

The surviving-spouse path also unlocks an important money point: many surviving spouses receiving DIC are exempt from the VA funding fee. If that applies to you, set the exemption flag in the VA loan calculator so your estimate is not inflated by a fee you will not pay.

Do You Even Qualify? The Service Requirements Behind the COE

The COE is just the proof. The underlying eligibility comes from your service length, and the minimums depend on when you served. These are the federal standards the VA applies in 2026.

Wartime service

If you served during a recognized wartime period, the minimum is generally at least 90 total days of active service. The classic wartime windows include World War II, the Korean War, and the Vietnam War.

Peacetime service

Peacetime minimums are longer:

- Service in the post-World War II and post-Korea peacetime gaps generally requires at least 181 continuous days.

- For the stretch from September 8, 1980 through August 1, 1990, and for the Gulf War era from August 2, 1990 to the present, the requirement is generally at least 24 continuous months of active duty, or the full period you were called to active duty.

National Guard and Reserve

Guard and Reserve members qualify with at least 90 days of non-training active-duty service, or with 6 creditable years in the Selected Reserve or National Guard, while still serving or after an honorable discharge. The 90-day federal active-duty path is separate from the six-year drilling path, and meeting either one can establish eligibility.

Because the exact wartime and peacetime windows have hard start and end dates, do not eyeball whether you fall inside one. Your DD214 dates settle it, and the VA verifies them when it issues the COE.

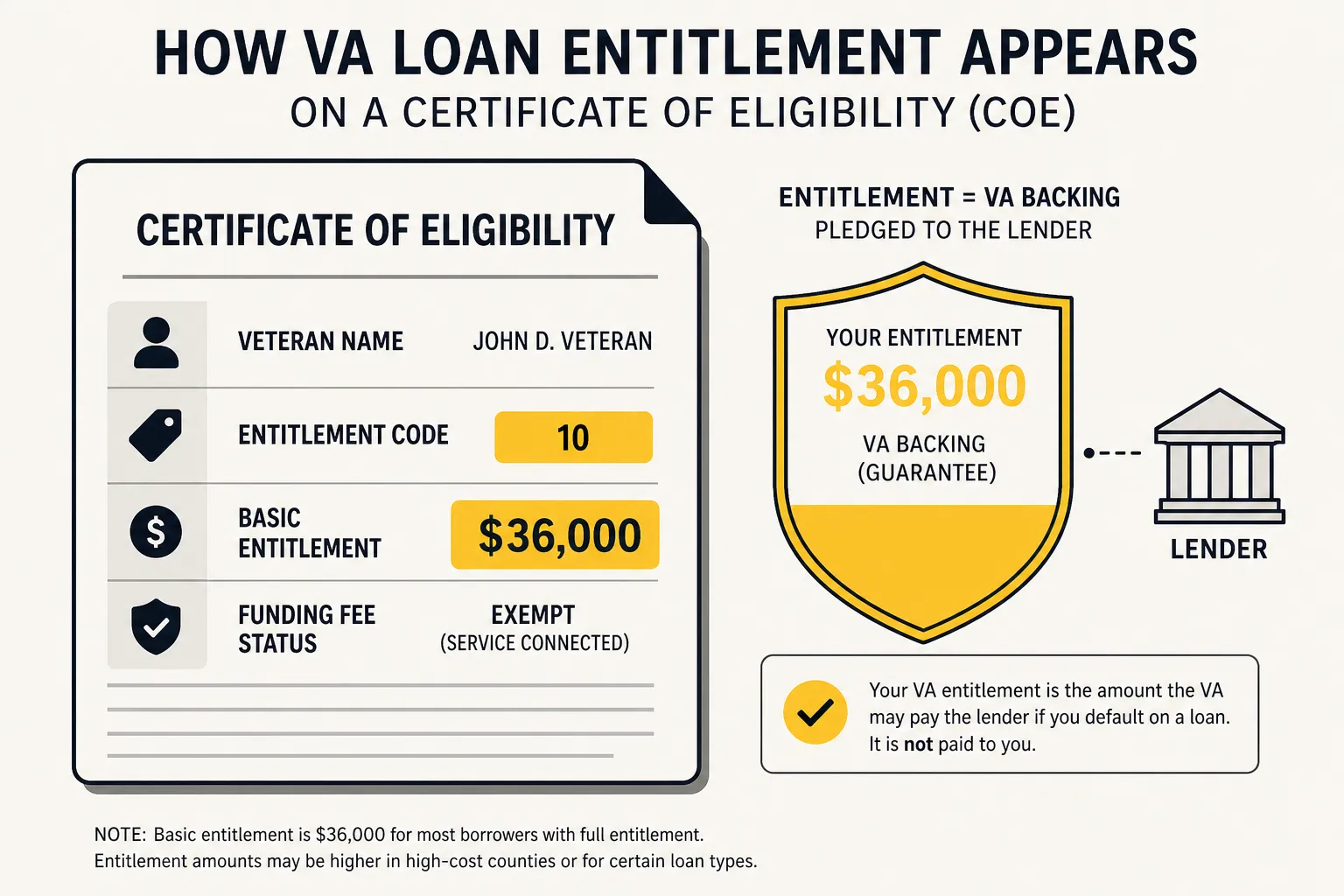

Understanding Entitlement on Your COE

When your COE comes back, it will list your entitlement. This is the part borrowers most often misread, so it is worth a plain-English explanation.

Entitlement is the amount the VA guarantees to your lender if you default. It is the government backing that lets lenders offer no down payment and no monthly mortgage insurance. There are two layers:

- Basic entitlement is the first tier, historically tied to a $144,000 figure that you will still see referenced on documents and in older guides.

- Bonus entitlement, sometimes called second-tier or Tier 2, sits on top and is what makes larger loans possible without a down payment.

Here is the headline that matters in 2026. If you have your full entitlement, meaning you have never used your VA loan benefit or you have fully restored it after selling a prior VA-financed home, there is no county loan limit. The lender's willingness to lend, based on your income and credit, becomes the real ceiling, not a VA cap. That has been the rule since the start of 2020 and it still holds.

Where limits come back into play is partial entitlement. If you already have an active VA loan, or you defaulted on one, you have used part of your entitlement, and county conforming loan limits then constrain how much you can borrow with zero down. In that situation a down payment can bridge the gap. The conforming loan limits themselves rose again for loans closing in 2026, so the math changes year to year.

The practical takeaway: the dollar figure on your COE describes your VA backing, not your maximum loan. To see how the loan size, the funding fee, and your down payment interact for your own numbers, model it in the VA loan calculator rather than trying to back into it from the certificate.

How the COE Fits Into the Whole Loan Process

It helps to see where the COE sits in the timeline so you know what to do and when.

- Confirm eligibility. Check your service dates against the requirements above. If you clearly qualify, you are ready to request the certificate.

- Get pre-approved. Talk to a VA-approved lender. They look at your credit and income and, in most cases, pull your COE automatically during this step.

- Request the COE if needed. If the automatic pull fails, request it online at VA.gov or by mailing VA Form 26-1880 with the right documents for your service type.

- House hunt and make an offer. You do not need the COE in hand to shop or to make an offer, only to close.

- Close. The COE must be in the loan file at closing. By then your lender has it, and the funding fee, if you owe one, is settled at the closing table.

Notice that the COE is an early, low-effort step, not the final hurdle. The heavy lifting in a VA loan is underwriting and the appraisal, which happen after eligibility is confirmed.

Common COE Mistakes and Snags

A handful of issues account for most of the delays people hit:

- An incomplete DD214. Submitting a copy that omits the character of service or the dates forces the VA to come back for more. Use a complete member copy that shows both.

- A name or Social Security number that does not match records. If your records have a typo or an old name, the automated request fails and you need to submit a document to reconcile it.

- Assuming the COE sets your loan limit. It does not. With full entitlement there is no county limit at all. Your lender and your finances set the real ceiling.

- Waiting for the COE before talking to a lender. You can do both at once. Letting the lender pull it is usually the fastest path anyway.

- Forgetting to claim a funding fee exemption. Veterans receiving VA disability compensation, Purple Heart recipients, and many surviving spouses are exempt from the funding fee. If that is you, make sure it is reflected, because it can save thousands. See the full breakdown in the VA funding fee guide.

Frequently Asked Questions

How do I get a VA Certificate of Eligibility?

You have three options. The fastest is to ask a VA-approved lender to pull it for you, which many can do online in minutes while you get pre-approved. You can also request it yourself by signing in at VA.gov and choosing "Request a COE," which the VA aims to handle in about five business days on average. As a backup, you can mail VA Form 26-1880 to your regional loan center. All three are free.

How long does it take to get a COE?

It varies by route. A lender's automated request can return your COE almost instantly when your service records are complete. A direct online request through VA.gov is targeted at an average of about five business days. Mailing a paper application is the slowest path and can take longer, so use it only when the electronic routes cannot verify you automatically.

Do I need a COE before I apply for a VA loan?

No. You can start house hunting and get pre-approved while your lender requests the COE in the background. The certificate only needs to be in your loan file by the time the loan closes, not before you begin.

What documents do I need for a COE?

It depends on your service type. Separated veterans need a complete copy of their DD214. Active-duty members need a statement of service signed by their command. National Guard and Reserve members need a DD214 if activated, or a statement of service or NGB Forms 22 and 23 if not. Surviving spouses need VA Form 26-1817 if they receive DIC, or VA Form 21P-534EZ with a marriage license and death certificate if they do not.

Does a COE guarantee I will get a VA loan?

No. The COE only confirms you meet the service requirements for the benefit. Your lender still has to approve you based on your credit, income, debt, and the home's appraisal. A valid COE is necessary but not sufficient for loan approval.

Does my COE show how much I can borrow?

Not exactly. The COE shows your entitlement, the VA's guaranty backing, not your maximum loan amount. If you have full entitlement there is no county loan limit at all, so your lender and your finances set the ceiling. If you have partial entitlement from a prior VA loan, conforming county limits can come into play and a down payment may be needed.

Can a surviving spouse get a COE?

Yes. A surviving spouse may be eligible for the VA home loan benefit. If you receive Dependency and Indemnity Compensation, you request your COE using VA Form 26-1817. If you do not receive DIC, you submit VA Form 21P-534EZ along with your marriage license and the veteran's death certificate. Many surviving spouses are also exempt from the funding fee.

Bottom Line

The Certificate of Eligibility is the front door to the VA home loan, but it is a low, easy step rather than the final hurdle. It proves your service-based eligibility, shows your entitlement, and flags any funding fee exemption, and that is all it does. It will not approve your loan or set your purchase price. The fastest path for most buyers is to let a VA-approved lender pull it during pre-approval, with the VA.gov request and the mailed VA Form 26-1880 as backups when records need a document to reconcile. Gather the right proof for your service type, claim any exemption you have earned, and once eligibility is settled, run your real numbers through the VA loan calculator to see your monthly payment and funding fee before you ever sit down at the closing table.

For the cost side of the benefit, see how the one-time charge is calculated and who skips it in the VA funding fee guide, and if you receive disability compensation, check how that interacts with the fee in the VA disability combined ratings guide.