VA Loan Rates 2026: Current Rates & How to Lock One In

How VA loan rates work in 2026 - why they run below conventional, what actually moves them, the funding fee tiers, and how to shop, lock, and run the payment math.

If you are searching for VA loan rates in 2026, the first thing to understand is that there is no single "VA rate" anyone can quote you and have it stay true. Mortgage rates move every business day, sometimes more than once, and the number a lender shows you this morning can be different by the afternoon. Anyone who promises you an exact rate without pulling your file and the day's market is selling something. What you can actually learn ahead of time is how VA rates are built, why they tend to sit a little below conventional rates, what makes your personal quote move up or down, and how to lock the rate once you find one you like. That is what this guide covers, and when you are ready to see what a given rate does to a monthly payment, the VA loan calculator does the math for your own price and term.

The Short Version

A VA loan rate is set by the lender, not by the Department of Veterans Affairs. The VA guarantees a portion of the loan, which lowers the lender's risk, and that backing is the reason VA rates usually come in slightly under comparable conventional rates on the same day. Beyond the broad market, your own rate is shaped by your credit, your loan size, the loan term, and whether you buy discount points.

- VA does not publish or control a rate. It guarantees the loan; lenders price the rate.

- VA rates typically run a touch below conventional rates because of that guarantee, though the exact gap changes daily.

- The biggest single advantage is not even the rate. It is that VA loans carry no monthly mortgage insurance, ever, which lowers your true cost of borrowing more than a small rate difference would.

- You should shop several lenders, because the same borrower can get materially different quotes on the same day.

Because the live number changes constantly, this guide stays away from quoting a specific APR as if it were fixed. Plug whatever rate your lender quotes into the VA loan calculator to turn it into a real monthly payment.

Why VA Rates Sit Below Conventional Rates

The Department of Veterans Affairs does not lend money. It runs a loan guaranty program. When you take a VA-backed loan, the VA promises the lender it will cover part of the loss if you default. That guaranty is a form of insurance for the lender, and a lender facing less risk can offer a lower rate for the same borrower.

On any given day, VA rates tend to land modestly below conventional rates for a comparable borrower. The size of that gap is not fixed and is not something you should bank on to the basis point, because it moves with the bond market and with how lenders are pricing their loan products that week. Some days the difference is meaningful, some days it narrows. Treat "usually a little lower" as the honest rule, not a guarantee.

There is a second reason VA financing is cheaper that has nothing to do with the headline rate. Conventional loans charge private mortgage insurance, or PMI, whenever you put down less than 20 percent, and that monthly premium can add a real chunk to your payment. VA loans never carry monthly mortgage insurance regardless of how little you put down. So even on a day when a VA rate and a conventional rate look close, the VA loan is usually the cheaper monthly payment once you account for the insurance the conventional borrower has to pay and you do not. When you compare offers, compare the all-in monthly cost, not just the interest rate. The VA loan calculator and the conventional mortgage calculator let you line the two up side by side.

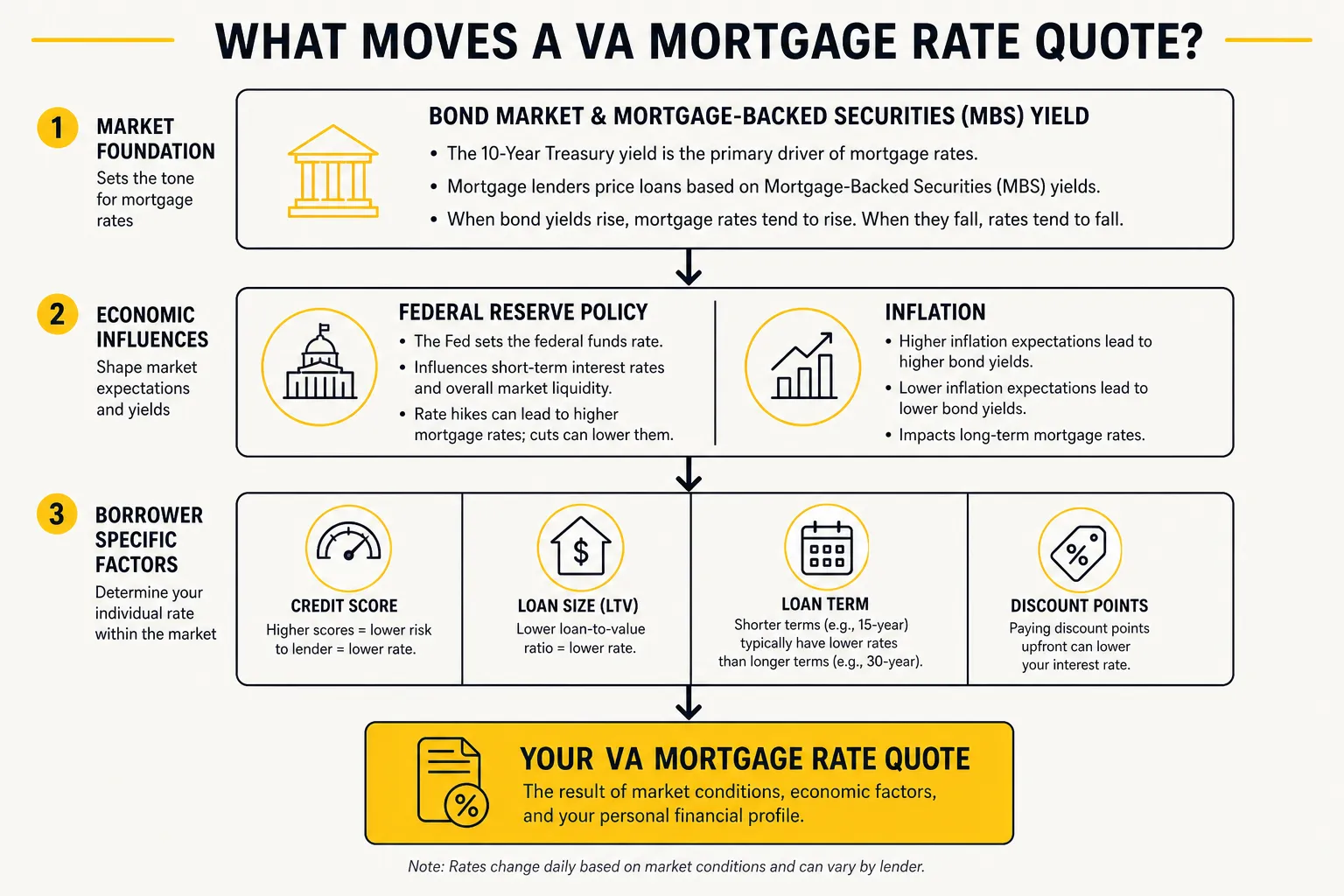

What Actually Moves Your VA Rate

Two layers determine the rate you are quoted. The first is the broad market, which you do not control. The second is your own file, which you partly do.

The market layer

Mortgage rates broadly track the bond market, specifically the yield on mortgage-backed securities, which in turn responds to inflation data, Federal Reserve policy signals, and the general appetite for those bonds. When inflation cools and bond yields fall, mortgage rates tend to drift down. When the economy runs hot or inflation surprises to the upside, rates tend to climb. This is why the rate you saw last month may be gone, and why no guide can hand you a current number that stays accurate. Nobody, including the lender, controls this layer. They are pricing off what the market did that morning.

The personal layer

On top of the market base rate, lenders adjust your specific quote using factors you can influence:

- Credit score. VA itself sets no minimum credit score, but lenders absolutely use yours to price the loan. A stronger score generally earns a lower rate. This is one of the most common surprises for borrowers, who assume the VA's no-minimum rule means score does not matter. It matters to the lender pricing your rate even though it does not matter to your basic eligibility.

- Loan term. A 15-year VA loan usually carries a lower rate than a 30-year, though the shorter term means a higher monthly payment.

- Loan amount and type. Purchase, cash-out refinance, and the streamline refinance (the IRRRL) are priced differently.

- Discount points. You can pay points up front to buy the rate down. One point is one percent of the loan amount paid at closing in exchange for a lower rate. Whether that trade is worth it depends entirely on how long you keep the loan, which is a break-even calculation worth running rather than guessing.

- Occupancy and property. VA loans are for a primary residence you intend to live in, and the property type can nudge the quote.

Because the personal layer varies so much, two veterans applying to the same lender on the same morning can be quoted different rates. That is normal, not a mistake, and it is exactly why shopping multiple lenders pays off.

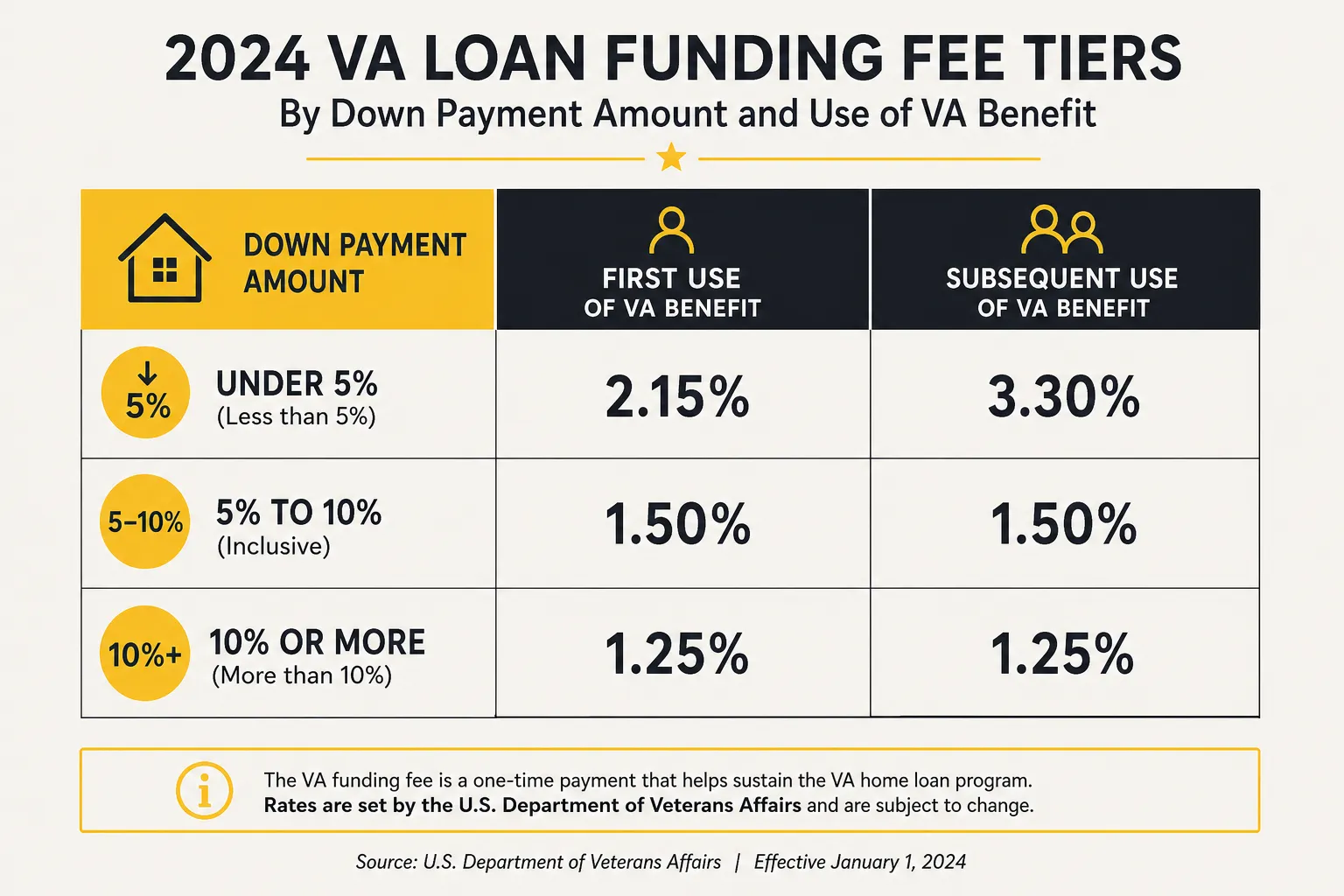

The Funding Fee: Not a Rate, but Part of Your Cost

People often blur the VA funding fee together with the interest rate. They are separate things. The interest rate is the ongoing cost of borrowing. The funding fee is a one-time charge that helps keep the VA loan program running at no cost to taxpayers. It does not change your rate, but it does change how much you finance, so it belongs in any honest look at the cost of a VA loan.

The fee is a percentage of the loan amount, and the percentage depends on two things: how much you put down, and whether this is your first time using the VA loan benefit or a later use. As currently published by the VA for purchase loans:

| Down payment | First use | Subsequent use |

|---|---|---|

| Less than 5% | 2.15% | 3.3% |

| 5% to less than 10% | 1.5% | 1.5% |

| 10% or more | 1.25% | 1.25% |

A few things to take from that table. First, putting down even 5 percent cuts the fee substantially on a first use, from 2.15 percent to 1.5 percent, and it removes the higher subsequent-use penalty entirely. Second, the streamline refinance (IRRRL) carries a much smaller funding fee of 0.5 percent, and a VA cash-out refinance is charged at 2.15 percent for a first use and 3.3 percent for a subsequent use. Always confirm the current figures against the VA's funding fee page before you close, since these are set by the VA and can be revised.

You can pay the funding fee in cash at closing or roll it into the loan, which is what most borrowers do. Rolling it in means you finance the fee and pay interest on it over the life of the loan, so it is not free, but it keeps your cash-to-close lower. When you model a payment in the VA loan calculator, include the funding fee in the financed amount to see its real effect.

Who pays no funding fee at all

A large share of VA borrowers are exempt from the funding fee entirely. You owe no funding fee if any of these apply to you:

- You are receiving VA compensation for a service-connected disability.

- You are eligible for VA compensation but are receiving retirement or active-duty pay instead.

- You are the surviving spouse of a veteran and are receiving Dependency and Indemnity Compensation.

- You received a proposed or memorandum disability rating before your loan closing on a pre-discharge claim.

- You are an active-duty service member who provides evidence of a Purple Heart on or before the closing date.

If you fall into any of these categories, the funding fee drops out of your cost picture completely, which makes the VA loan even cheaper relative to the alternatives. Confirm your exempt status with your lender and your COE early, because it changes the numbers.

How VA Loan Eligibility Affects Your Pricing

Your rate quote and your eligibility are connected but separate. Eligibility is whether you can use the benefit at all. To use a VA loan you need a Certificate of Eligibility, the COE, which verifies your service history to the lender. The minimum service requirement is generally at least 90 continuous days of active duty, though the exact requirement depends on when you served and whether you are active duty, a veteran, National Guard, or Reserve. The COE is what proves your eligibility to the lender; it does not set your rate.

Two pricing-relevant points often get missed:

- No down payment is available nationwide. Since January 1, 2020, there have been no county loan limits for veterans with full entitlement, meaning the VA does not cap how much you can borrow with zero down in any part of the country. Loan limits still apply only to borrowers with partial entitlement who have a prior VA loan they have not yet restored and are borrowing above $144,000. For most buyers using the benefit fresh, the no-limit, no-down-payment rule is the headline.

- Zero down does not mean the cheapest rate or fee. Putting nothing down is allowed, but it lands you in the highest funding fee tier, and some lenders price the rate slightly higher for a 100 percent loan-to-value loan. There is no monthly mortgage insurance either way, but the funding fee math alone is a reason to put down 5 percent if you can comfortably afford it.

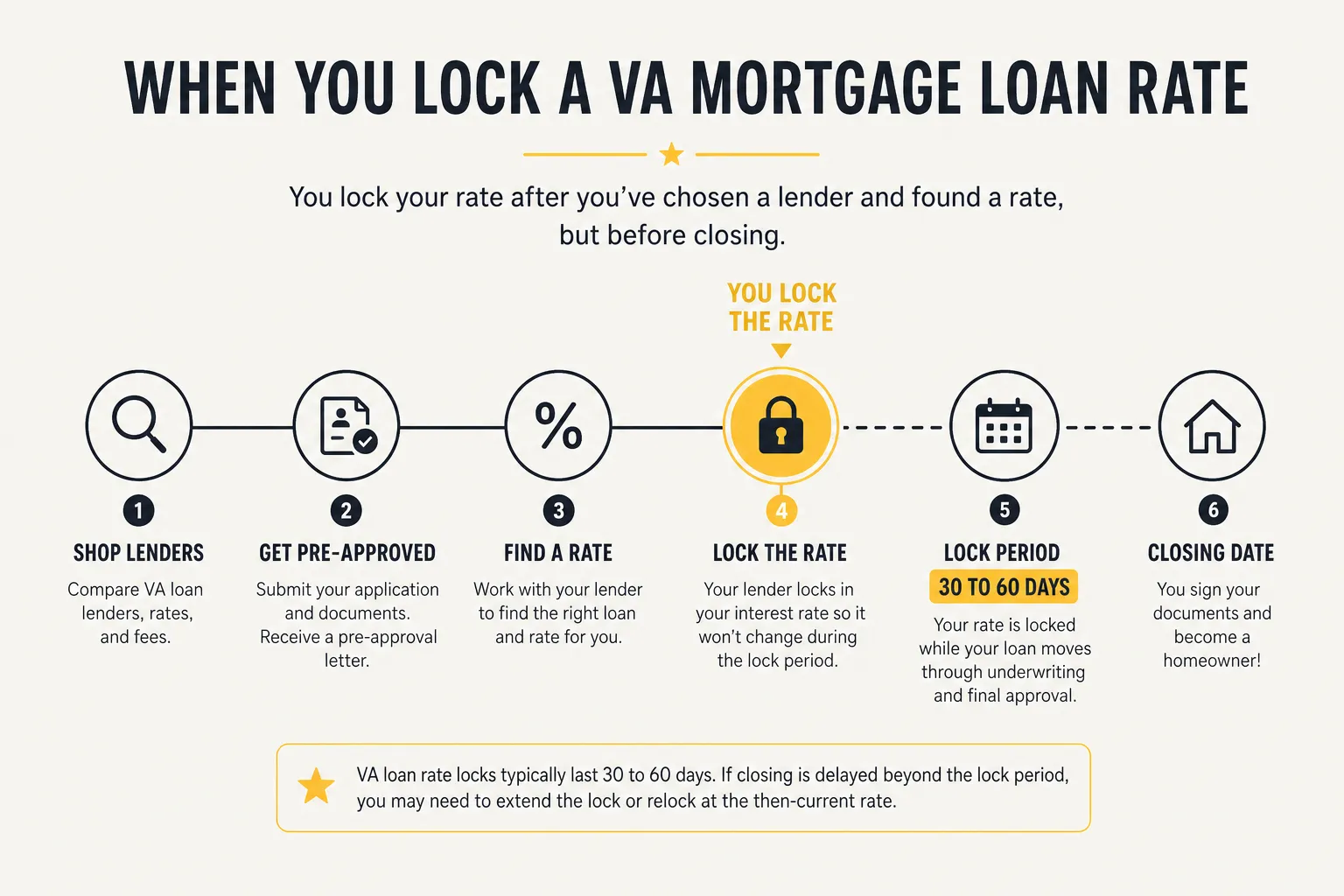

How to Shop and Lock a VA Rate

Once you understand that the rate is a moving, lender-set number, the strategy becomes clear: shop several lenders on the same day, then lock when you find a quote you are comfortable with.

Shop on the same day, compare the same things

Because rates move daily, a quote from Lender A on Monday and Lender B on Thursday are not really comparable. Gather quotes within the same day or two, and compare the full picture: the interest rate, the APR, the points charged, the lender fees, and the estimated monthly payment. A lower rate with high points and fees can cost you more than a slightly higher rate with none. Lenders are required to give you a Loan Estimate, which lays these out in a standard format so you can compare apples to apples.

What a rate lock actually does

A rate lock is the lender's promise to hold a specific rate for a set window, commonly 30 to 60 days, while your loan closes. Once locked, your rate will not move even if the market rises during that window. The flip side is that if the market falls after you lock, you are generally held to the locked rate unless you bought a float-down option.

- Standard 30-day and 45-day locks are typically free at most lenders.

- Longer locks of 60, 75, or 90 days may carry a small cost, often expressed in fractions of a discount point, because the lender is carrying market risk for longer.

- A float-down option lets you capture a lower rate if the market drops after you lock, but it usually costs extra and the terms vary by lender. Ask whether it is available and what it costs before assuming you have it.

Lock or float: how to decide

The honest answer is that nobody can time the bottom of the rate market, and trying to is how borrowers end up chasing a rate that keeps moving away from them. Lock when you have a signed purchase contract and a rate that makes the payment work for your budget. Float, meaning wait to lock, only if you have a clear reason to expect rates to fall and you can stomach the risk that they rise instead. For most buyers, locking a comfortable rate once you are under contract is the lower-stress, more reliable move. Run the locked rate through the VA loan calculator so you know the exact payment you are committing to before you sign.

Common Mistakes That Cost You

A handful of errors come up again and again when veterans shop VA rates:

- Quoting yourself a rate from an ad. The teaser rate on a website is for an ideal borrower on a past day. Your real rate comes from a lender pulling your file. Use advertised rates only as a rough sense of the market, never as your number.

- Shopping only one lender. The same borrower can get noticeably different quotes from different lenders on the same day. Getting at least three Loan Estimates is one of the highest-return hours you can spend.

- Comparing rate without comparing fees and points. A headline rate that looks great can hide high points or junk fees. Compare the APR and the full Loan Estimate, not just the interest rate.

- Ignoring the no-PMI advantage when comparing to conventional. A conventional loan with a similar rate is usually more expensive monthly once PMI is added. Always compare the all-in payment.

- Forgetting the funding fee in the math. If you roll it in, you are financing it and paying interest on it. Include it in the loan amount when you estimate the payment.

- Treating the funding fee as unavoidable. If you have a service-connected disability rating or another exemption, you may owe no funding fee at all. Confirm it early, because it changes the numbers.

Frequently Asked Questions

What are VA loan rates today?

There is no fixed answer, because VA mortgage rates change every business day with the bond market. VA rates are set by individual lenders, not by the Department of Veterans Affairs, and they typically run modestly below comparable conventional rates because the VA guaranty lowers the lender's risk. The only accurate "today" rate is one a lender quotes after reviewing your credit, loan amount, and term. Take that quote and drop it into the VA loan calculator to see your real monthly payment.

Are VA loan rates lower than conventional rates?

Usually, yes, but by a margin that changes daily. On a typical day a VA rate sits a little below a conventional rate for the same borrower, thanks to the VA guaranty. The larger and more reliable advantage, though, is that VA loans carry no monthly mortgage insurance while conventional loans charge PMI on down payments under 20 percent. That difference often makes the VA payment lower even when the rates look similar, so always compare the all-in monthly cost.

Does the VA set the interest rate?

No. The VA guarantees part of the loan but does not set or publish interest rates. Lenders set the rate based on the market and on your personal file. That is why you should shop multiple lenders, since quotes for the same borrower on the same day can differ meaningfully.

How do I lock a VA loan rate?

You lock by telling your lender to hold a specific quoted rate for a set period, usually 30 to 60 days, while your loan closes. Standard 30-day and 45-day locks are typically free; longer locks may cost a fraction of a point. Lock once you have a signed purchase contract and a rate that fits your budget rather than trying to time the market bottom.

Does my credit score affect my VA loan rate?

Yes. The VA itself sets no minimum credit score, but lenders use your score to price your rate, and a higher score generally earns a lower one. So while a lower score will not necessarily disqualify you from a VA loan, it can raise the rate a lender offers.

Is the funding fee part of the interest rate?

No. The funding fee is a separate one-time charge based on your down payment and whether it is a first or subsequent use of the benefit, ranging from 1.25 percent to 3.3 percent on a purchase loan, with lower fees for the streamline refinance. It does not change your interest rate, but it does add to the amount you finance if you roll it in. Many borrowers, including those with a service-connected disability rating, are exempt from it entirely.

Bottom Line

VA loan rates in 2026 cannot be pinned to a single number, and you should be skeptical of anyone who tries. What is reliable is the structure: the VA guarantees the loan, lenders set the rate, that backing usually keeps VA rates a little under conventional, and the absence of monthly mortgage insurance widens the real cost advantage further. Your own rate then turns on your credit, term, loan size, and whether you buy points. The smart play is to shop several lenders on the same day, compare the full Loan Estimate rather than the headline rate, account for the funding fee unless you are exempt, and lock once you are under contract with a rate that fits your budget. Then run that exact rate through the VA loan calculator so the payment you commit to is one you have already seen on paper.

For more on the broader cost picture, see how a VA loan stacks up against a conventional mortgage in the VA loan vs conventional guide, and use the conventional mortgage calculator to compare the all-in monthly numbers side by side.