National Guard & Reserve Drill Pay 2026: How Drill Pay Works

How National Guard and Reserve drill pay works in 2026 - the 1/30 rule, 4 drill periods per weekend, the 3.8% raise, what allowances you do and do not get, and retirement points.

If you serve in the National Guard or the Reserves, the paycheck math is different from active duty in one specific way: you are paid by the drill period, not by the month. A drill weekend is not "a weekend of work" in pay terms. It is four separate paid blocks, and each one is worth exactly one thirtieth of what an active-duty service member at your rank earns in a month. Get that one rule straight and the rest of National Guard drill pay falls into place, including why the number on your bank statement looks the way it does and why it almost never matches anybody's back-of-the-napkin guess.

This guide walks through how drill pay is actually calculated in 2026, what counts as a drill period, the 3.8 percent raise that took effect this January, which allowances you do and do not receive on a drill weekend, how drill pay is taxed, and how every drill you complete also feeds your retirement points. The dollar amounts move with your paygrade and your years of service, so instead of quoting figures that go stale the day the pay tables change, run your own rank through the BAH calculator and the pay tools as you read.

The Core Rule: One Drill Period Equals 1/30 of Monthly Basic Pay

Here is the entire foundation of drill pay in one sentence. For each drill period you complete, you earn one thirtieth of the monthly active-duty base pay for your paygrade and years of service.

That is the rule the Defense Finance and Accounting Service uses to process every drill paycheck. It does not matter that there are 28, 30, or 31 days in the calendar month. The divisor is always 30. One drill period equals one day of active-duty basic pay, computed as the monthly rate divided by 30.

So the question "how much is a drill worth" has a clean answer: take the monthly active-duty basic pay for your rank, divide by 30, and that is one drill period. An active-duty E-5 and a drilling Guard E-5 with the same time in service draw from the exact same basic pay table. The difference is the active-duty member is paid for the whole month and the reservist is paid one thirtieth at a time, only for the periods actually worked.

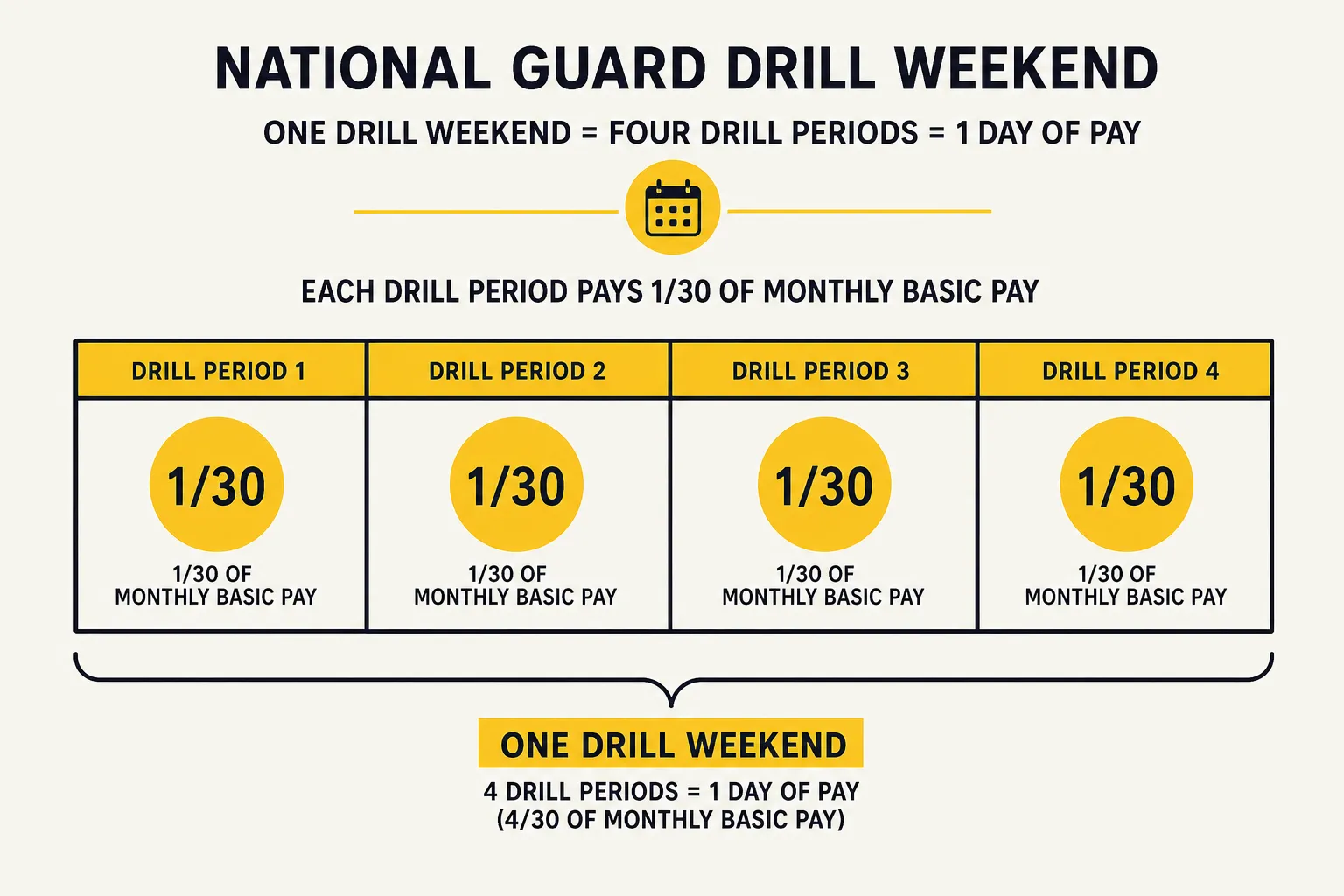

A Drill Weekend Is Four Drill Periods

The phrase "one weekend a month" hides how the pay is counted. A standard drill weekend is not one unit or two. It is four.

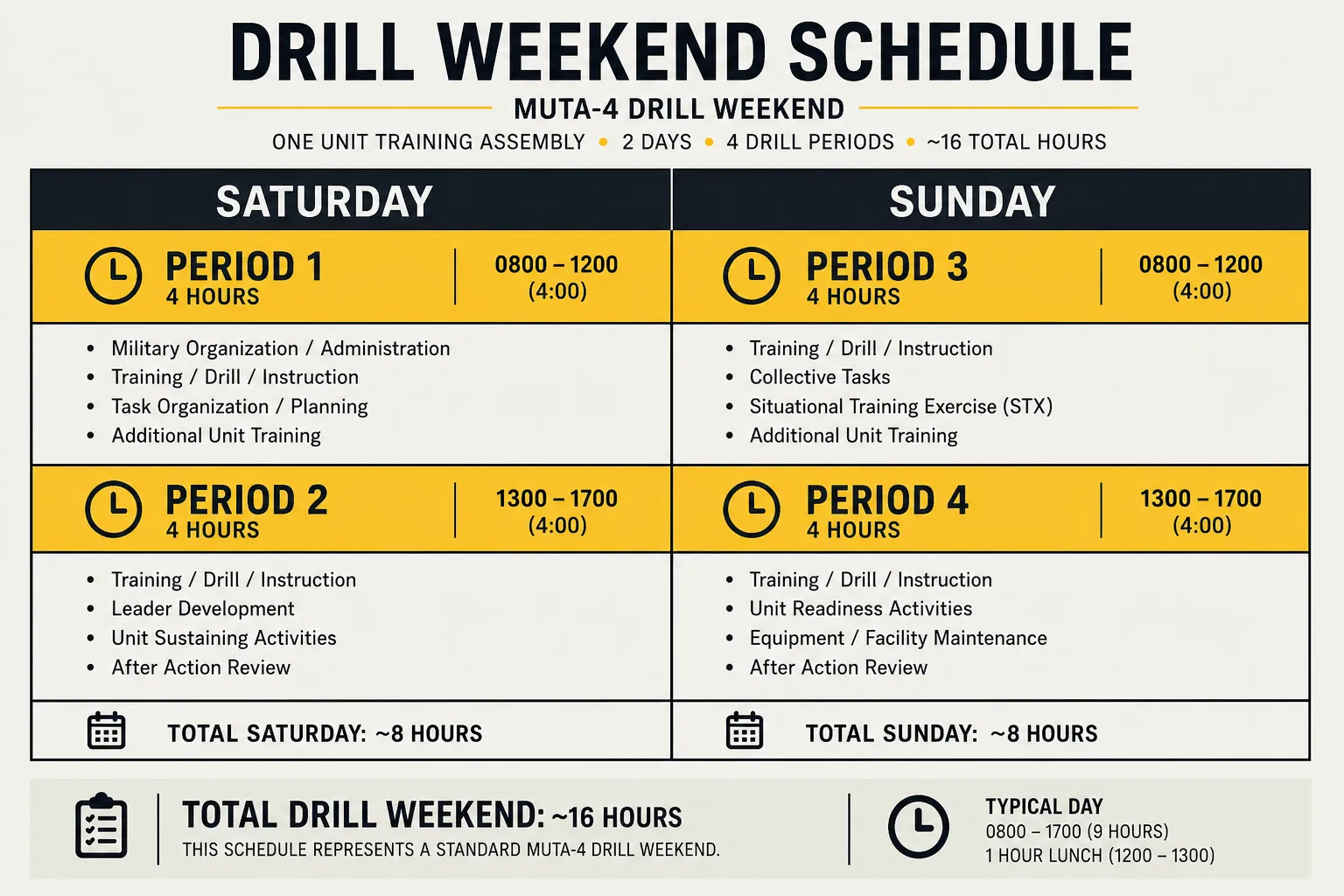

A normal drill weekend runs Saturday and Sunday, with two drill periods scheduled each day. Two days times two periods equals four drill periods, often written as a MUTA-4 (Multiple Unit Training Assembly, four periods). Each drill period is built around roughly four hours of training, which is how a full Saturday and a full Sunday add up to four blocks.

Because each period pays 1/30 of monthly basic pay, a four-period drill weekend pays:

Monthly basic pay divided by 30, times 4 = 4/30 of monthly basic pay

That is the single most useful formula on this page. A standard drill weekend puts roughly four days of active-duty base pay into your account, even though you only showed up for two calendar days. That is not a bonus or an error. It is the design: two drill periods are packed into each day, and each period is paid separately.

Why your weekend pay looks higher than two days of work

This trips up almost everyone the first time. You worked Saturday and Sunday, two days, but you were paid four-thirtieths of a month, which is about four days of active-duty salary. The reason is the period structure, not generosity. The service compresses four training periods into the two calendar days of the weekend, and the 1/30 rule pays each period.

It also means you cannot estimate drill pay by dividing your civilian sense of a weekend into a monthly salary. The honest way to size it up is to find your monthly basic pay rate, multiply by 4, and divide by 30. To anchor that against the rest of your military compensation picture, the BAH calculator shows where housing fits in, which matters more than you might expect once you see the allowance rules below.

The 2026 Pay Raise: 3.8 Percent Across the Board

Drill pay rides on the active-duty basic pay table, so when basic pay goes up, drill pay goes up by the same percentage. For 2026, the raise is 3.8 percent, effective January 1, 2026. The fiscal year 2026 National Defense Authorization Act did not set a specific basic pay adjustment rate, so the increase came through the automatic mechanism in 37 U.S.C. § 1009, which ties the annual raise to the Employment Cost Index (ECI). The Bureau of Labor Statistics calculated an ECI of 3.8 percent for the three-month period ending September 30, 2024, and that figure became the 2026 raise.

Two details matter for Guard and Reserve members specifically:

- The raise is uniform this year. Unlike 2025, when junior enlisted members received a larger targeted bump, the 2026 increase is a flat 3.8 percent across all paygrades. Your drill period is 3.8 percent larger than it was in December 2025, whatever your rank.

- It hit the drill rate automatically. Because drill pay is just 1/30 of the active-duty monthly figure, you did not have to do anything to capture the raise. The January 2026 pay tables already bake it in, and DFAS applies it to every drill period from January 1 forward.

The practical takeaway: do not use a 2025 chart to estimate 2026 drill pay. The base number is 3.8 percent higher now. When you plug a paygrade into a current tool, make sure it is reading the 2026 table.

What Allowances You Get on a Drill Weekend (and What You Do Not)

This is where many new Guard and Reserve members lose money in their planning, because they assume drill pay works like active-duty pay. It does not. On a normal drill weekend you are in an Inactive Duty Training (IDT) status, and IDT pays basic pay only.

No BAH and no BAS on a normal drill weekend

On a standard drill weekend you do not receive Basic Allowance for Housing and you do not receive Basic Allowance for Subsistence. Those allowances are tied to active-duty orders, not to inactive-duty training. Drilling for the weekend is IDT, so the housing and food allowances simply do not trigger.

That is a meaningful gap. On active duty, BAH and BAS can make up a large share of total compensation, often rivaling basic pay itself. A drilling reservist gets none of that on a drill weekend. Your weekend pay is four-thirtieths of basic pay, full stop, with no allowance layered on top.

When allowances do show up

The picture changes the moment you go onto actual duty orders:

- Annual Training (AT) and short active-duty orders under 30 days. When you are activated for fewer than 30 consecutive days, you generally receive a reserve-component housing allowance known as BAH RC/T (Reserve Component/Transit), which is a flat, non-locality rate, plus BAS for the days on orders.

- Active duty of 30 days or more. Once you are on orders for 30 consecutive days or longer, you move to full locality-based BAH for your duty ZIP code, the same as an active-duty member, along with BAS.

So the rule of thumb is simple: drill weekend equals basic pay only; orders unlock allowances, with the size of the housing allowance depending on how long the orders run. If you are trying to forecast income for an upcoming AT period or a mobilization, the locality housing piece is the variable that swings the total most, and the BAH calculator is built to estimate exactly that by ZIP and paygrade.

How Drill Pay Is Taxed and Whether It Counts for TSP

Two more practical questions come up constantly.

Drill pay is taxable

Drill pay is basic pay, and basic pay is taxable income. Federal income tax and FICA (Social Security and Medicare) are withheld from your drill paycheck just as they are from an active-duty salary. The amount that lands in your account is the gross drill figure minus those withholdings, which is why the deposit is smaller than the 4/30 calculation suggests.

There is one major exception that mirrors active duty: if you perform drills or duty inside a designated combat zone, the combat zone tax exclusion can make that pay federally tax-free. For ordinary stateside weekend drills, though, plan on the pay being fully taxable.

State tax treatment varies. A number of states fully or partially exempt military pay, including drill pay, from state income tax, while others tax it normally. Check your state of legal residence rather than assuming.

Drill pay counts toward TSP

Your drill pay is eligible for Thrift Savings Plan contributions. The percentage you elect comes out of your drill (and any active-duty) basic pay. If you are under the Blended Retirement System, the government's automatic 1 percent contribution and any matching apply to the basic pay you earn on drill status too, subject to the same vesting and timing rules that apply on active duty. In short, drilling members build TSP balances the same way active-duty members do, just on smaller per-period amounts. For how the match and vesting work in detail, see the BRS vs High-3 comparison.

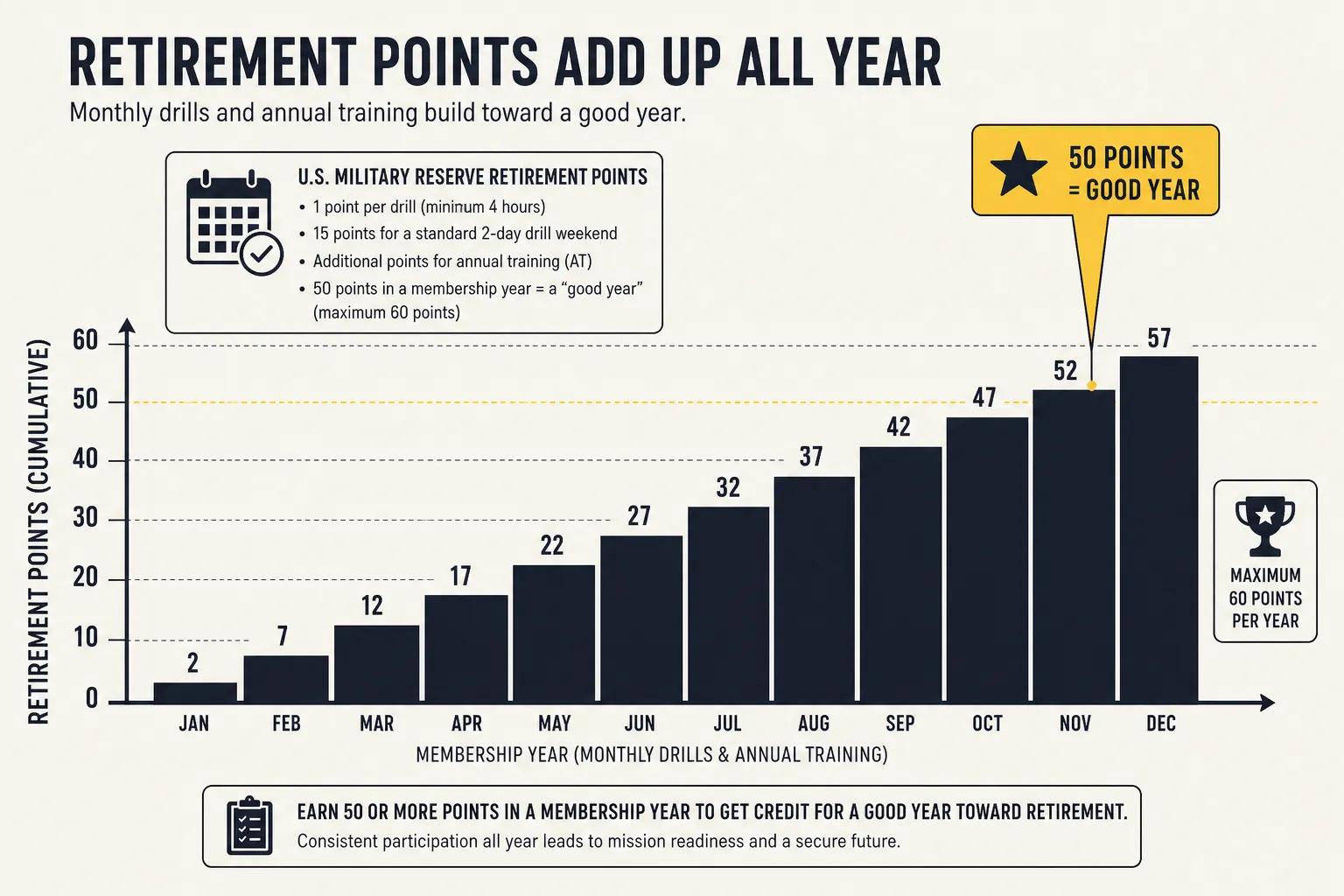

Every Drill Also Earns a Retirement Point

Drill pay and retirement credit travel together, and it is worth understanding both at once because the same drill period does double duty.

One point per drill period

For each drill period you complete, you earn one retirement point, just as you earn 1/30 of basic pay. So a four-period drill weekend that pays 4/30 of monthly basic pay also earns four retirement points. Annual Training and active-duty days each earn one point per day as well, and the service grants 15 membership points per year just for being a participating member.

What makes a "good year"

Guard and Reserve retirement is built on qualifying years, often called good years. A good year is any year in which you accumulate at least 50 retirement points. You need 20 good years to qualify for reserve retired pay, which generally begins at age 60 (earlier in some cases for qualifying active-duty mobilizations).

Here is how the points stack up for a member who drills the standard schedule and does the standard two weeks of Annual Training:

| Source | Points |

|---|---|

| Membership | 15 |

| 12 drill weekends (4 periods each = 48 drills) | 48 |

| Annual Training (about 14 days) | 14 |

| Typical yearly total | 77 |

Even the bare-minimum participant who completes only the 48 required drill periods and nothing else lands at 15 plus 48, or 63 points, comfortably above the 50-point threshold for a good year. The drills that fill your paycheck are the same drills that build the 20-good-year ladder to a pension. For how those points later convert into actual retired pay, the High-3 retirement walkthrough covers the pension formula that the reserve system plugs your point total into.

Putting a Real Number on Your Drill Weekend

To estimate your own drill weekend pay without guessing:

- Find your monthly active-duty basic pay for your paygrade and years of service on the current 2026 table. Drilling members use the exact same basic pay figures as active duty.

- Multiply by 4 for a standard four-period drill weekend.

- Divide by 30. That is your gross weekend drill pay before taxes.

- Subtract withholding (federal income tax, Social Security, Medicare, and any TSP election) to land on what actually hits your account.

A few honest caveats. If your unit schedules a different number of periods (some assemblies are MUTA-2 or run additional periods), scale the multiplier accordingly: it is always the number of drill periods divided by 30. Special and incentive pays, such as flight or hazardous duty pay, are added on top when you qualify and are doing the qualifying duty during the period. And remember that none of this includes BAH or BAS on a normal weekend, because IDT does not pay allowances.

Common Drill Pay Mistakes to Avoid

A handful of errors show up over and over with new Guard and Reserve members:

- Assuming a weekend pays two days of salary. It pays four-thirtieths of a month, roughly four days, because there are four drill periods in the weekend, not two.

- Expecting BAH or BAS on a drill weekend. Those allowances only appear once you are on active-duty orders. A normal weekend is basic pay only.

- Estimating with last year's chart. The 2026 raise added 3.8 percent. Old tables understate every drill period.

- Forgetting drill pay is taxable. The deposit is smaller than the gross 4/30 figure because federal tax and FICA come out first.

- Leaving TSP money on the table. Drill basic pay is TSP-eligible, and under BRS the match applies, so contributing through your drill pay is real long-term money, not loose change.

Frequently Asked Questions

How much is one drill period worth?

One drill period is worth 1/30 of the monthly active-duty basic pay for your paygrade and years of service. Drilling Guard and Reserve members draw from the same basic pay table as active duty, just paid one thirtieth at a time per period worked. To see the rate for your rank, use the current 2026 pay table and divide the monthly figure by 30.

How many drill periods are in a drill weekend?

A standard drill weekend has four drill periods, two on Saturday and two on Sunday, commonly called a MUTA-4. Because each period pays 1/30 of monthly basic pay, a standard weekend pays 4/30 of your monthly basic pay, or roughly four days of active-duty salary.

Do National Guard and Reserve members get BAH on drill weekends?

No. On a normal drill weekend you are in Inactive Duty Training status, which pays basic pay only with no Basic Allowance for Housing and no Basic Allowance for Subsistence. You receive a housing allowance only when you go onto active-duty orders: a flat BAH RC/T (Reserve Component/Transit) rate for orders under 30 days, or full locality BAH for orders of 30 days or more.

Did drill pay go up in 2026?

Yes. Drill pay rose 3.8 percent on January 1, 2026, matching the across-the-board active-duty basic pay raise. The fiscal year 2026 National Defense Authorization Act did not set a specific rate, so the raise came through the automatic adjustment in 37 U.S.C. § 1009, which is tied to the Employment Cost Index. The increase is uniform across all paygrades this year, and DFAS applied it automatically to every drill period starting in January.

Is drill pay taxable?

Yes, drill pay is basic pay and is subject to federal income tax and FICA withholding, so your deposit is smaller than the gross 4/30 figure. The combat zone tax exclusion can make drill or duty pay federally tax-free if performed in a designated combat zone, and several states exempt military pay from state income tax. Check your state of legal residence.

How many retirement points does a drill weekend earn?

A standard four-period drill weekend earns four retirement points, one per drill period, the same periods that generate your pay. Add 15 membership points per year plus a point for each Annual Training day, and most drilling members clear the 50-point threshold for a qualifying good year. Twenty good years qualifies you for reserve retired pay, generally starting at age 60.

Bottom Line

National Guard and Reserve drill pay comes down to one rule applied four times: each drill period pays 1/30 of your monthly active-duty basic pay, and a standard weekend is four periods, so it pays 4/30, about four days of salary for two days at the armory. The 2026 raise lifted that base by 3.8 percent across the board. On a normal weekend you get basic pay only, with no BAH or BAS until you are on active-duty orders, and the pay is taxable and TSP-eligible. Every drill period you complete also banks a retirement point toward the 20 good years that unlock a reserve pension. To size up the part that swings the most once you do go on orders, run your paygrade and duty ZIP through the BAH calculator rather than trusting a rule of thumb.